2.2: Process Costing Vs. Job Order Costing

- Page ID

- 65675

Nature of a process cost system

Many businesses produce large quantities of a single product or similar products. Pepsi-Cola makes soft drinks, Exxon Mobil produces oil, and Kellogg Company produces breakfast cereals on a continuous basis over long periods. For these kinds of products, companies do not have separate jobs. Instead, production is an ongoing process.

A YouTube element has been excluded from this version of the text. You can view it online here: http://pb.libretexts.org/ma/?p=70

Job costing and process costing have important similarities:

- Both job and process cost systems have the same goal: to determine the cost of products.

- Both job and process cost systems have the same cost flows. Accountants record production in separate accounts for materials inventory, labor, and overhead. Then, they transfer the costs to a Work in Process Inventory account.

- Both job and process cost systems use predetermined overhead rates to apply overhead.

Job costing and process costing systems also have their significant differences:

- Types of products produced. Companies that use job costing work on many different jobs with different production requirements during each period. Companies that use process costing produce a single product, either on a continuous basis or for long periods. All the products that the company produces under process costing are the same.

- Cost accumulation procedures. Job costing accumulates costs by individual jobs. Process costing accumulates costs by process or department.

- Work in Process Inventory accounts. Job cost systems have one Work in Process Inventory account for each job. Process cost systems have a Work in Process Inventory account for each department or process.

Aprocess cost system (process costing) accumulates costs incurred to produce a product according to the processes or departments a product goes through on its way to completion. Companies making paint, gasoline, steel, rubber, plastic, and similar products using process costing. In these types of operations, accountants must accumulate costs for each process or department involved in making the product. As an example, view this How’s It Made video.

A YouTube element has been excluded from this version of the text. You can view it online here: http://pb.libretexts.org/ma/?p=70

Can you imagine having to determine the cost of making just ONE lego when we can make 1.7 million legos per hour? Cost accountants have to do this. They will use process costing! Accountants compute the cost per unit by first accumulating costs for the entire period (usually a month) for each process or department. Second, they divide the accumulated costs by the number of units produced (tons, pounds, gallons, or feet) in that process or department.

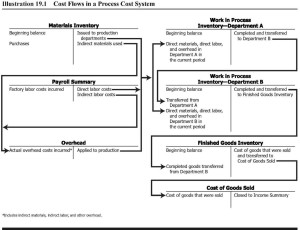

The next picture shows the cost flows in a process cost system that processes the products in a specified sequential order. That is, the production and processing of products begin in Department A. From Department A, products go to Department B. Department B inputs direct materials and further processes the products. Then Department B transfers the products to Finished Goods Inventory.

There are two methods for using process costs: Weighted Average and FIFO (First In First Out). Each method uses equivalent units and cost per equivalent units but calculates them just a little differently.

Contributors and Attributions

- Accounting Principles: A Business Perspective.. Authored by: James Don Edwards, University of Georgia & Roger H. Hermanson, Georgia State University.. Provided by: Endeavour International Corporation. Project: The Global Text Project. License: CC BY: Attribution

- Job Order Costing vs Process Costing. Authored by: Education Unlocked. Located at: https://youtu.be/F6RzLSSKlZM. License: All Rights Reserved. License Terms: Standard YouTube License

- How It's Made Lego. Authored by: How Is Made. Located at: https://youtu.be/zrzKih5rqD0. License: All Rights Reserved. License Terms: Standard YouTube License