6: How Is the Statement of Cash Flows Prepared and Used?

- Page ID

- 51375

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\( \newcommand{\dsum}{\displaystyle\sum\limits} \)

\( \newcommand{\dint}{\displaystyle\int\limits} \)

\( \newcommand{\dlim}{\displaystyle\lim\limits} \)

\( \newcommand{\id}{\mathrm{id}}\) \( \newcommand{\Span}{\mathrm{span}}\)

( \newcommand{\kernel}{\mathrm{null}\,}\) \( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\) \( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\) \( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\id}{\mathrm{id}}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\kernel}{\mathrm{null}\,}\)

\( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\)

\( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\)

\( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\) \( \newcommand{\AA}{\unicode[.8,0]{x212B}}\)

\( \newcommand{\vectorA}[1]{\vec{#1}} % arrow\)

\( \newcommand{\vectorAt}[1]{\vec{\text{#1}}} % arrow\)

\( \newcommand{\vectorB}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vectorC}[1]{\textbf{#1}} \)

\( \newcommand{\vectorD}[1]{\overrightarrow{#1}} \)

\( \newcommand{\vectorDt}[1]{\overrightarrow{\text{#1}}} \)

\( \newcommand{\vectE}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash{\mathbf {#1}}}} \)

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\(\newcommand{\longvect}{\overrightarrow}\)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\(\newcommand{\avec}{\mathbf a}\) \(\newcommand{\bvec}{\mathbf b}\) \(\newcommand{\cvec}{\mathbf c}\) \(\newcommand{\dvec}{\mathbf d}\) \(\newcommand{\dtil}{\widetilde{\mathbf d}}\) \(\newcommand{\evec}{\mathbf e}\) \(\newcommand{\fvec}{\mathbf f}\) \(\newcommand{\nvec}{\mathbf n}\) \(\newcommand{\pvec}{\mathbf p}\) \(\newcommand{\qvec}{\mathbf q}\) \(\newcommand{\svec}{\mathbf s}\) \(\newcommand{\tvec}{\mathbf t}\) \(\newcommand{\uvec}{\mathbf u}\) \(\newcommand{\vvec}{\mathbf v}\) \(\newcommand{\wvec}{\mathbf w}\) \(\newcommand{\xvec}{\mathbf x}\) \(\newcommand{\yvec}{\mathbf y}\) \(\newcommand{\zvec}{\mathbf z}\) \(\newcommand{\rvec}{\mathbf r}\) \(\newcommand{\mvec}{\mathbf m}\) \(\newcommand{\zerovec}{\mathbf 0}\) \(\newcommand{\onevec}{\mathbf 1}\) \(\newcommand{\real}{\mathbb R}\) \(\newcommand{\twovec}[2]{\left[\begin{array}{r}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\ctwovec}[2]{\left[\begin{array}{c}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\threevec}[3]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\cthreevec}[3]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\fourvec}[4]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\cfourvec}[4]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\fivevec}[5]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\cfivevec}[5]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\mattwo}[4]{\left[\begin{array}{rr}#1 \amp #2 \\ #3 \amp #4 \\ \end{array}\right]}\) \(\newcommand{\laspan}[1]{\text{Span}\{#1\}}\) \(\newcommand{\bcal}{\cal B}\) \(\newcommand{\ccal}{\cal C}\) \(\newcommand{\scal}{\cal S}\) \(\newcommand{\wcal}{\cal W}\) \(\newcommand{\ecal}{\cal E}\) \(\newcommand{\coords}[2]{\left\{#1\right\}_{#2}}\) \(\newcommand{\gray}[1]{\color{gray}{#1}}\) \(\newcommand{\lgray}[1]{\color{lightgray}{#1}}\) \(\newcommand{\rank}{\operatorname{rank}}\) \(\newcommand{\row}{\text{Row}}\) \(\newcommand{\col}{\text{Col}}\) \(\renewcommand{\row}{\text{Row}}\) \(\newcommand{\nul}{\text{Nul}}\) \(\newcommand{\var}{\text{Var}}\) \(\newcommand{\corr}{\text{corr}}\) \(\newcommand{\len}[1]{\left|#1\right|}\) \(\newcommand{\bbar}{\overline{\bvec}}\) \(\newcommand{\bhat}{\widehat{\bvec}}\) \(\newcommand{\bperp}{\bvec^\perp}\) \(\newcommand{\xhat}{\widehat{\xvec}}\) \(\newcommand{\vhat}{\widehat{\vvec}}\) \(\newcommand{\uhat}{\widehat{\uvec}}\) \(\newcommand{\what}{\widehat{\wvec}}\) \(\newcommand{\Sighat}{\widehat{\Sigma}}\) \(\newcommand{\lt}{<}\) \(\newcommand{\gt}{>}\) \(\newcommand{\amp}{&}\) \(\definecolor{fillinmathshade}{gray}{0.9}\)John Huston, CEO and founder of Home Store, Inc., has reviewed the company’s income statement and balance sheet for the most recent fiscal year ended December 31, 2020. Home Store has grown rapidly this past year, with sales and net income showing significant gains compared to 2019. Although John is satisfied with the increase in profitability, he notices a significant decline in cash. John decides to pursue this with Linda Nash (CFO) and Steve Bauer (treasurer) in their weekly meeting:

John:

I just received the income statement and balance sheet for 2020. Profits look great, but our cash position seems to have deteriorated. We had $130,000 in cash to start the year and ended with only $32,000. I noticed cash was declining throughout the year when I reviewed our monthly financial statements, but I’m concerned about how far our cash balance has dropped.

Steve:

You’re right, John. We encountered cash flow problems several times throughout the year in spite of increased sales and profits. On several occasions, I had to delay payments to creditors because of cash flow issues.

John:

Seems to me we shouldn’t have this problem. Where is our cash going?

Linda:

Good question. Let me round up our cash flow information for the year. I’ll have something for you by next week.

John:

Great! I’d like to start next week’s meeting by discussing how much cash we generated in 2020 from our daily operations. I realize net income is shown on an accrual basis, but I’d like to know how much net income was received in the form of cash.

Linda:

No problem. I’ll have it for you next week.

Home Store, Inc., has cash flow problems that are common to many fast growing companies. Although the income statement and balance sheet provide important information concerning financial performance and financial condition, neither statement provides information regarding cash activity for a period of time. The focus of this chapter is on preparing a statement that provides cash flow information. This statement is appropriately called the statement of cash flows.

6.1 Purpose of the Statement of Cash Flows

Learning Objectives

- Define the purpose of the statement of cash flows.

Question: Most organizations prepare four financial statements for external reporting purposes: income statement, balance sheet, statement of owners’ equity, and statement of cash flows. Financial accounting courses cover the first three statements in detail and often provide an overview of the statement of cash flows. This chapter will focus on preparing the statement of cash flows and on using the resulting cash flow information for analytical purposes. What information is provided in the statement of cash flows?

Answer: The statement of cash flows provides cash receipt and cash payment information and reconciles the change in cash for a period of time. Cash receipts and cash payments are summarized and categorized as operating, investing, or financing activities. Simply put, the statement of cash flows indicates where cash came from and where cash went for a period of time.

Assume you keep track of your individual cash transactions for an entire year in a check register (e.g., checks written and paycheck deposits) and suppose you have hundreds of transactions for the year. Rather than showing every single transaction in a formal report, the statement of cash flows summarizes these transactions. For example, all cash receipts from paychecks are added together and shown as one line item, all cash payments for rent are added together and shown as one line item, all cash payments for food are added together and shown as one line item, and so on. The goal is to start with the beginning of the year cash balance, add all cash receipts for the year, subtract all cash payments for the year, and find the resulting end-of-year cash balance. Although the formal statement of cash flows is not quite this simple, the concept is the same.

Question: Why did the Financial Accounting Standards Board (FASB) create the statement of cash flows in 1987?

Answer: The statement of cash flows was created due to a lack of cash flow information on the income statement, balance sheet, and statement of owners’ equity. The income statement shows revenues and expenses using the accrual basis of accounting, but it does not indicate how much cash was received for revenues or paid for expenses. The balance sheet shows assets, liabilities, and owners’ equity at a point in time, but it does not show how much cash was received or paid for these items. The only cash information provided on these statements is the change in cash from the end of last period to the end of the current period derived from the cash line item on the balance sheet (often called cash and cash equivalents).

Owners, creditors, and managers wanted more cash flow information. They often asked such questions as: Why did cash go down? How much cash was received related to net income? How much cash was paid for the purchase of equipment? How much cash was received from issuing bonds? As a result of the demand for more cash flow information, the FASB formally created the statement of cash flows in 1987 (Statement of Financial Accounting Standard No. 95, which can be found at http://www.fasb.org). Most companies are now required to prepare the statement of cash flows along with the other three statements. We begin the process of explaining how to prepare this statement in the next section.

Business in Action 6.1

Cash Flows at Southwest Airlines

Southwest Airlines was in the enviable position of generating $2.3 billion in net income for the year ended December 31, 2019. However, cash on the balance sheet only increased $700 million for the same period. Why did total cash go up by such a small amount compared to the net income? The statement of cash flows provides the information necessary to answer this question. Southwest generated nearly $4 billion from operating activities including net income. Southwest spent $303 million on property and equipment (planes, parts, etc.) and $3 billion to pay off long-term debt and buy back treasury stock.

Source: Southwest Airlines, “2019 Annual Report,” http://www.southwest.com.

Key Takeaway

- The statement of cash flows provides cash receipt and cash payment information and reconciles the change in cash for a period of time. The primary purpose of the statement is to show what caused the change in cash from the beginning of the period to the end of the period.

Check Yourself

- Describe the purpose of the statement of cash flows.

- Why did the FASB create the statement of cash flows?

Solution

- The purpose of the statement of cash flows is to provide a summary of cash receipt and cash payment information for a period of time and to reconcile the difference between beginning and ending cash balances shown on the balance sheet. The statement of cash flows clarifies how cash was generated and how cash was used for a period of time.

- The FASB created the statement of cash flows because owners, creditors, managers, and other stakeholders wanted more information regarding cash receipts and cash expenditures. Although the balance sheet shows cash balances at the end of each period, no further information is provided on the balance sheet, income statement, or statement of owners’ equity regarding cash flow activities. The statement of cash flows takes care of this problem.

6.2 Three Types of Cash Flow Activities

Learning Objectives

- Describe the three categories of cash flows.

Question: What are the three types of cash flows presented on the statement of cash flows?

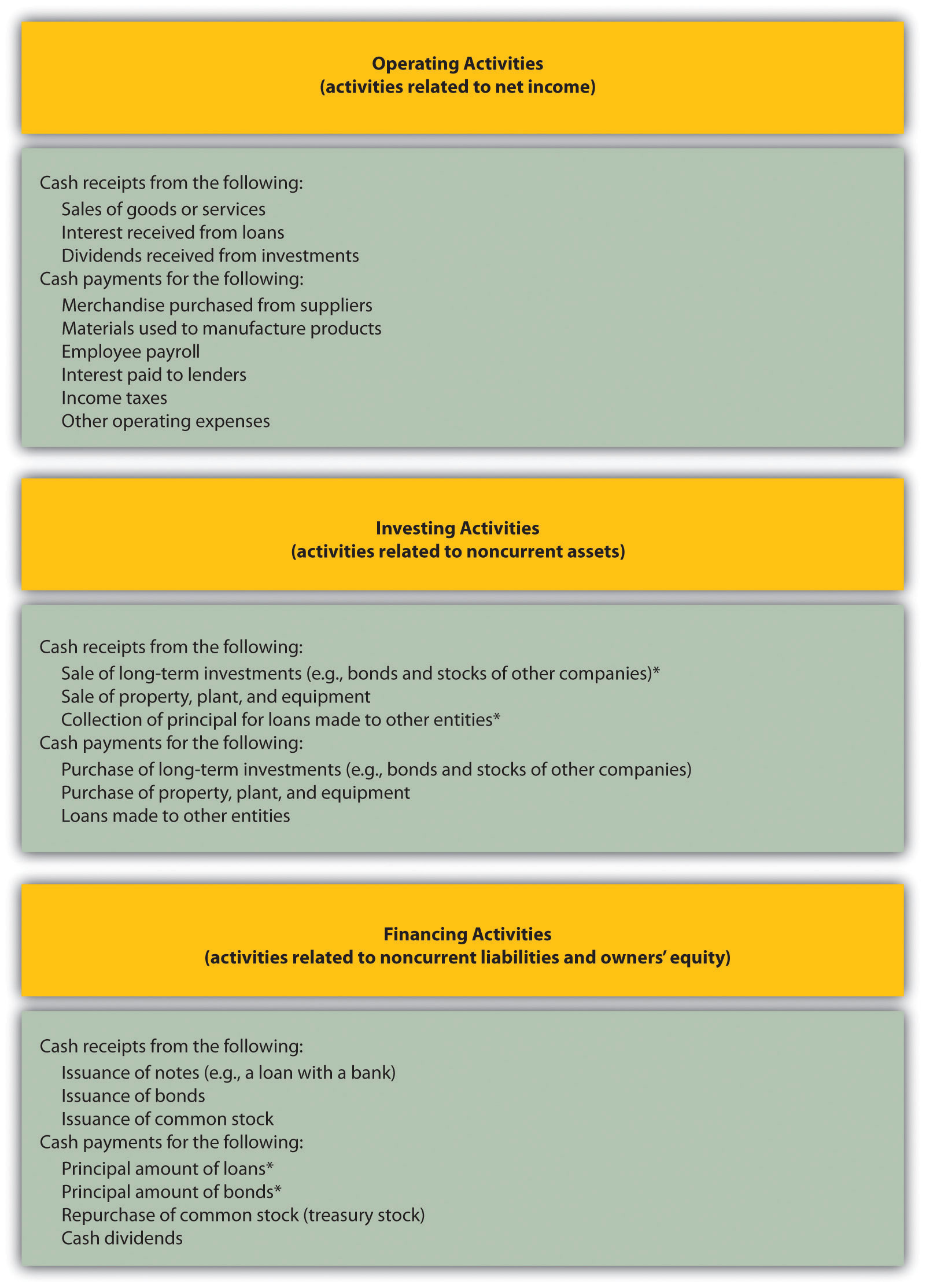

Answer: Cash flows are classified as operating, investing, or financing activities on the statement of cash flows, depending on the nature of the transaction. Each of these three classifications is defined as follows.

- Operating activities include cash activities related to net income. For example, cash generated from the sale of goods (revenue) and cash paid for merchandise (expense) are operating activities because revenues and expenses are included in net income.

- Investing activities include cash activities related to noncurrent assets. Noncurrent assets include (1) long-term investments; (2) property, plant, and equipment; and (3) the principal amount of loans made to other entities. For example, cash generated from the sale of land and cash paid for an investment in another company are included in this category. (Note that interest received from loans is included in operating activities.)

- Financing activities include cash activities related to noncurrent liabilities and owners’ equity. Noncurrent liabilities and owners’ equity items include (1) the principal amount of long-term debt, (2) stock sales and repurchases, and (3) dividend payments. (Note that interest paid on long-term debt is included in operating activities.)

Figure 6.1 “Examples of Cash Flows from Operating, Investing, and Financing Activities” shows examples of cash flow activities that generate cash or require cash outflows within a period.

Figure 6.1 Examples of Cash Flow Activity by Category

*Receipts of cash for dividends from investments and for interest on loans made to other entities are included in operating activities since both items relate to net income. Likewise, payments of cash for interest on loans with a bank or on bonds issued are also included in operating activities because these items also relate to net income.

Question: Which section of the statement of cash flows is regarded by most financial experts to be most important?

Answer: The operating activities section of the statement of cash flows is generally regarded as the most important section since it provides cash flow information related to the daily operations of the business. This section answers the question, “how much cash did we generate from the daily activities of our core business?” Owners, creditors, and managers are most interested in cash flow generated from daily activities rather than from a one-time issuance of stock or a one-time sale of land. The operating activities section allows stakeholders to assess the ongoing viability of the company. We discuss how to use cash flow information to evaluate organizations later in the chapter.

Business in Action 6.2

Cash Activity at Home Depot and Lowe’s

The Home Depot. Inc., and Lowe’s Companies, Inc., are large home improvement retail companies with stores throughout North America. A review of the statements of cash flows for both companies reveals the following cash activity. Positive amounts are cash inflows, and negative amounts are cash outflows.

| Home Depot | Lowes | |

| Operating | 13,723 | 4,296 |

| Investing | (2,653) | (1,369) |

| Financing | (10,834) | (2,734) |

| Net Change in Cash | 236 | 193 |

Amounts are in millions.

This information shows both companies generated significant amounts of cash from daily operating activities; $13.7 billion for The Home Depot and $4.3 billion for Lowe’s. It is interesting to note both companies spent significant amounts of cash to acquire property and equipment and long-term investments as reflected in the negative investing activities amounts. For both companies, a significant amount of cash outflows from financing activities were for the repurchase of common stock. Apparently, both companies chose to return cash to owners by repurchasing stock. So while the amounts for Home Depot are significantly higher than for Lowes the pattern is remarkably similar and the resulting change in cash is very close to the same.

Source: The Home Depot Inc., “2019 Annual Report,” http://www.homedepot.com; Lowe’s Companies Inc., “2019 Annual Report,” http://www.lowes.com.

Key Takeaways

- The three categories of cash flows are operating activities, investing activities, and financing activities. Operating activities include cash activities related to net income. Investing activities include cash activities related to noncurrent assets. Financing activities include cash activities related to noncurrent liabilities and owners’ equity.

Check Yourself

Identify whether each of the following items would appear in the operating, investing, or financing activities section of the statement of cash flows. Explain your answer for each item.

- Cash payments for purchases of merchandise

- Cash receipts from sale of common stock

- Cash payments for equipment

- Cash receipts from sales of goods

- Cash dividends paid to shareholders

- Cash payments to employees

- Cash payments to lenders for interest on loans

- Cash receipts from collection of principal for loans made to other entities

- Cash receipts from issuance of bonds

- Cash receipts from collection of interest on loans made to other entities

Solution

- It would appear as operating activity because merchandise activity impacts net income as an expense (merchandise costs ultimately flow through cost of goods sold on the income statement).

- It would appear as financing activity because sale of common stock impacts owners’ equity.

- It would appear as investing activity because purchase of equipment impacts noncurrent assets.

- It would appear as operating activity because sales activity impacts net income as revenue.

- It would appear as financing activity because dividend payments impact owners’ equity.

- It would appear as operating activity because employee payroll activity impacts net income as an expense.

- It would appear as operating activity because interest payments impact net income as an expense.

- It would appear as investing activity because principal collections impact noncurrent assets.

- It would appear as financing activity because bond issuance activity impacts noncurrent liabilities.

- It would appear as operating activity because interest received impacts net income as revenue.

6.3 Four Key Steps to Preparing the Statement of Cash Flows

Learning Objectives

- Describe the four steps used to prepare the statement of cash flows.

Question: Recall from your financial accounting course that the accrual basis of accounting recognizes revenue when earned and expenses when incurred, regardless of when cash is exchanged. Conversely, the cash basis of accounting recognizes revenue when cash is received and expenses when cash is paid, regardless of when goods or services are exchanged. The income statement, balance sheet, and statement of owners’ equity are all created using the accrual basis of accounting. However, the statement of cash flows is based on cash flows only, and thus adjustments must be made to convert accrual basis information to a cash basis. What information is necessary to make these adjustments?

Answer: Several pieces of information are required to make these adjustments in preparing the statement of cash flows:

- Balance sheets for the end of last year and end of the current year are needed to calculate the amount of change in each balance sheet account. These changes in balance sheet accounts are needed to prepare certain parts of the statement of cash flows.

- Income statement information for the current year is needed as the starting point for converting net income from an accrual basis to a cash basis, which is shown in the operating activities section of the statement of cash flows.

- Other information is needed to complete the statement of cash flows, such as cash dividends paid and the original cost of long-term investments sold.

Question: With this information in hand, four steps are required to prepare the statement of cash flows. What are these four steps?

Answer: The four steps required to prepare the statement of cash flows are described as follows:

Step 1. Prepare the operating activities section by converting net income from an accrual basis to a cash basis.

This step can be done using one of two methods—the direct method or the indirect method. Because more than 98 percent of companies surveyed use the indirect method we will use the indirect method throughout this chapter.

The indirect method begins with net income from the income statement and makes several adjustments related to changes in current assets, current liabilities, and other items to arrive at cash provided by operating activities (or used by operating activities if the result is a cash outflow). Cash provided by operating activities represents net income on a cash basis. It tells the reader how much cash was received from the daily operations of the business.

Step 2. Prepare the investing activities section by presenting cash activity for noncurrent assets.

This step focuses on the effect changes in noncurrent assets have on cash. Noncurrent asset balances found on the balance sheet, coupled with other information (e.g., cash proceeds from sale of equipment) are used to perform this step.

Step 3. Prepare the financing activities section by presenting cash activity for noncurrent liabilities and owners’ equity.

This step focuses on the effect changes in noncurrent liabilities and owners’ equity have on cash. Noncurrent liabilities and owners’ equity balances found on the balance sheet, coupled with other information (e.g., cash dividends paid) are used to perform this step.

Step 4. Reconcile the change in cash.

Each section of the statement of cash flows described in steps 1, 2, and 3, will show the total cash provided by (increase) or used by (decrease) the activity. Step 4 simply confirms that the net of these changes equates to the change in cash on the balance sheet.

For example, assume the balance sheet shows cash totaled $100 at the end of last year and $140 at the end of the current year. Thus cash increased $40 over the course of the current year. Step 4 reconciles this change with the changes shown in the three sections of the statement of cash flows. Suppose operating activities provided cash of $170, investing activities used cash of $160, and financing activities provided cash of $30. These 3 amounts netted together reconcile to the $40 increase in cash shown on the balance sheet (= $170 − $160 + $30).

Key Takeaways

-

The four steps required to prepare the statement of cash flows are described as follows:

Step 1. Prepare the operating activities section by converting net income from an accrual basis to a cash basis.

Step 2. Prepare the investing activities section by presenting cash activities for noncurrent assets.

Step 3. Prepare the financing activities section by presenting cash activities for noncurrent liabilities and owners’ equity.

Step 4. Reconcile the change in cash from the beginning of the period to the end of the period.

Check Yourself

Describe the four steps necessary to prepare the statement of cash flows.

Solution

The four steps required to prepare the statement of cash flows are as follows:

Step 1. Prepare the operating activities section by converting net income from an accrual basis to a cash basis.

This step starts with net income on an accrual basis (from the income statement) and makes adjustments related to changes in current assets, current liabilities, and other items to find net income on a cash basis. The resulting cash basis net income is called cash provided by operating activities.

Step 2. Prepare the investing activities section by presenting cash activity for noncurrent assets.

This step focuses on the effect changes in noncurrent assets have on cash.

Step 3. Prepare the financing activities section by presenting cash activity for noncurrent liabilities and owners’ equity.

This step focuses on the effect changes in noncurrent liabilities and owners’ equity have on cash.

Step 4. Reconcile the change in cash.

Each section of the statement of cash flows described in steps 1, 2, and 3 will show the total cash provided by or used by each activity. Step 4 confirms that the net of these changes equates to the change in cash derived from the balance sheet.

6.4 Using the Indirect Method to Prepare the Statement of Cash Flows

Learning Objectives

- Prepare a statement of cash flows using the indirect method.

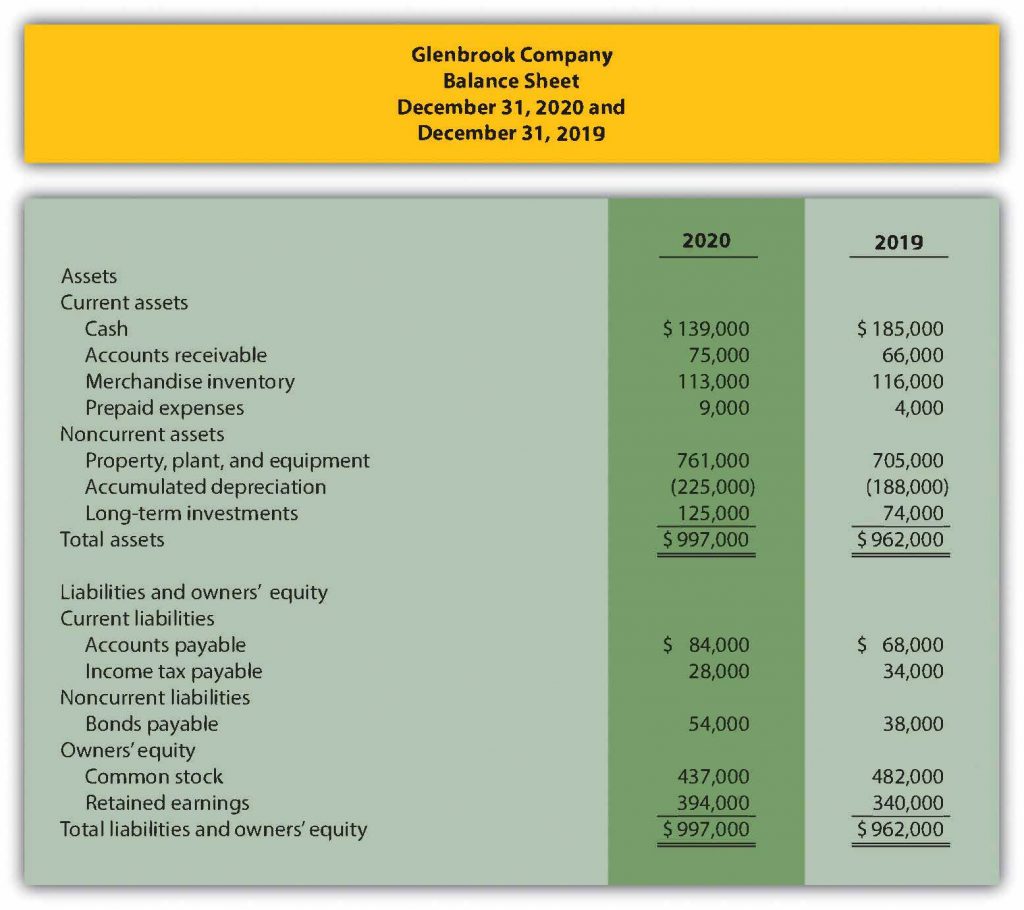

Question: Now that you are familiar with the four key steps, let’s take a look at the statement of cash flows for Home Store, Inc. Where do we start in preparing Home Store, Inc.’s statement of cash flows?

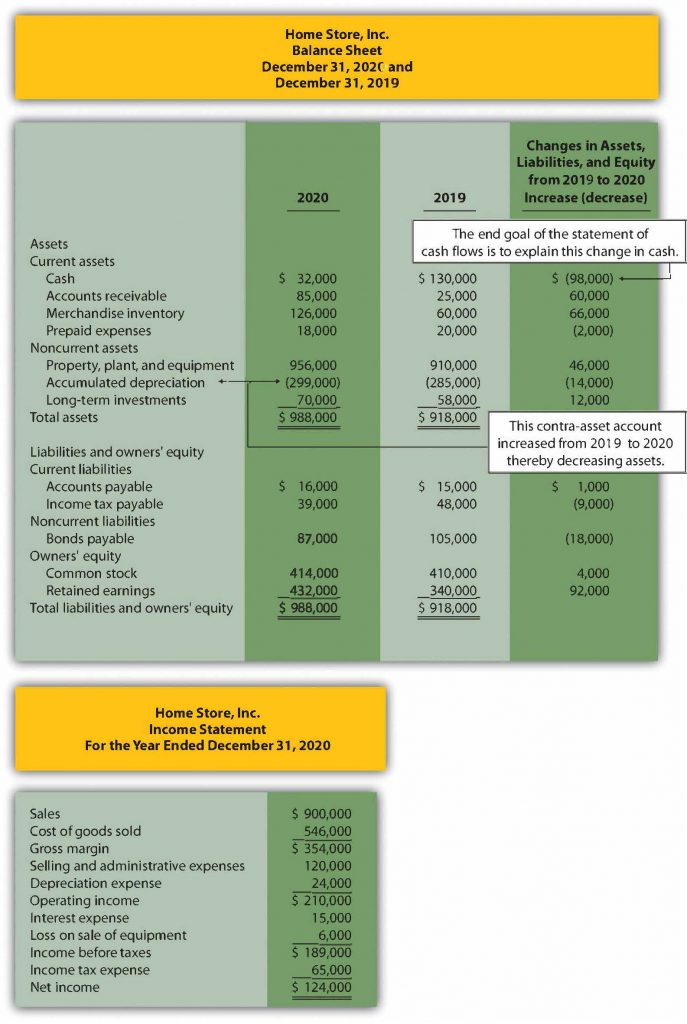

Answer: As stated earlier, the information needed to prepare the statement of cash flows includes the balance sheet, income statement, and other selected data. This information is presented in Figure 6.2 “Balance Sheet and Income Statement for Home Store, Inc.”. Other pertinent data for 2020 are as follows:

- Sold equipment with a book value of $11,000 (= $21,000 cost − $10,000 accumulated depreciation) for $5,000 cash

- Purchased equipment for $67,000 cash

- Long-term investments were purchased for $12,000 cash. There were no sales of long-term investments

- Bonds were paid with a principal amount of $18,000

- Issued common stock for $4,000 cash

- Declared and paid $32,000 in cash dividends

With these data and the information provided in Figure 6.2 “Balance Sheet and Income Statement for Home Store, Inc.”, we can start preparing the statement of cash flows. It is important to note that all positive amounts shown in the statement of cash flows denote an increase in cash, and all negative amounts denote a decrease in cash.

Figure 6.2 Balance Sheet and Income Statement for Home Store, Inc.

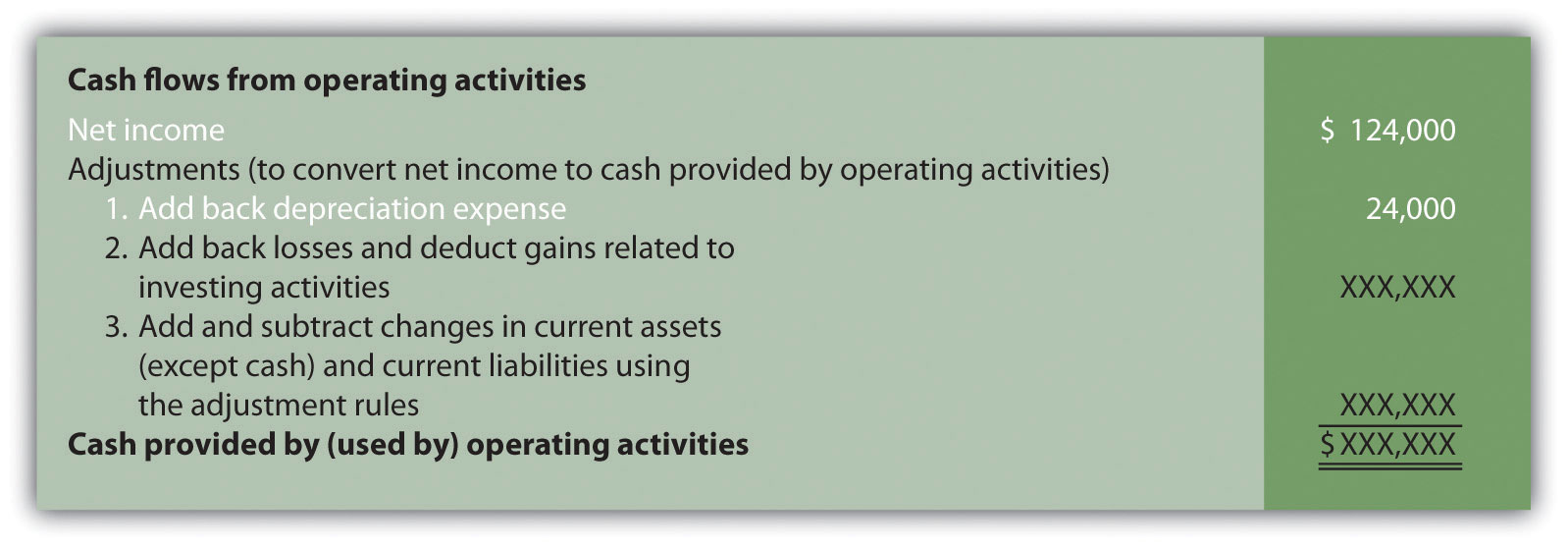

Step 1: Prepare the Operating Activities Section

Question: We will be using the indirect method to prepare the operating activities section. The starting point using the indirect method is net income. Home Store, Inc., had net income of $124,000 in 2020. This amount comes from the income statement, which was prepared using the accrual basis of accounting. How do we convert this amount to a cash basis?

Answer: Several adjustments are necessary to convert this amount to a cash basis and to provide an amount related only to daily operating activities of the business. If the resulting adjusted amount is a cash inflow, it is called cash provided by operating activities; if it is a cash outflow, it is called cash used by operating activities.

Three general types of adjustments are necessary to convert net income to cash provided by operating activities. These three types of adjustments are shown in Figure 6.3 “Operating Activities Format and Adjustments”, which also displays the format used for the operating activities section of the statement of cash flows. Examine this figure carefully.

Figure 6.3 Operating Activities Format and Adjustments

Adjustment One: Adding Back Noncash Expenses

Question: What is the first type of adjustment necessary to convert net income to a cash basis?

Answer: The first adjustment to net income involves adding back expenses that do not affect cash (often called noncash expenses). For example, the accrual basis of accounting deducts depreciation expense in calculating net income, even though depreciation expense does not involve cash. (Recall the financial accounting entry to record depreciation expense: debit depreciation expense and credit accumulated depreciation. Notice cash is not involved.) Thus to convert net income to a cash basis, depreciation expense is added back to net income. In effect, we are reversing depreciation expense because it is not an expense using the cash basis of accounting. The end result is as though depreciation expense was never deducted as an expense.

Next, we show how the first adjustment to net income appears in the operating activities section of the statement of cash flows for Home Store, Inc. (net income and depreciation expense come from the income statement shown in Figure 6.2 “Balance Sheet and Income Statement for Home Store, Inc.”):

The income statement for Home Store, Inc., shows $24,000 in depreciation expense for the year. As shown previously, this amount is added back to the net income of $124,000.

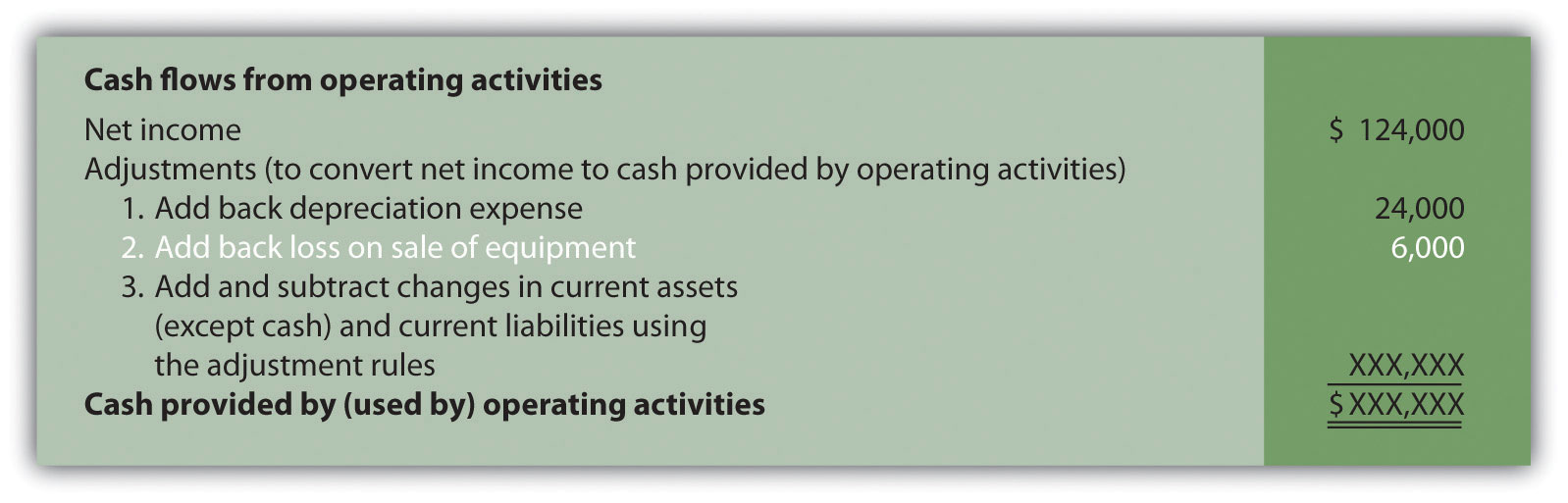

Adjustment Two: Adding Back Losses and Deducting Gains Related to Investing Activities

Question: What is the second type of adjustment necessary to convert net income to a cash basis?

Answer: The second adjustment to net income involves adding back losses and deducting gains related to investing activities. For example, Home Store, Inc., realized a $6,000 loss on the sale of equipment. This loss is shown on the income statement as a deduction in calculating net income (see Figure 6.2 “Balance Sheet and Income Statement for Home Store, Inc.”). However, this loss is not related to the daily operations of the business. That is, Home Store, Inc., is not in the business of buying and selling equipment daily. Remember, we are trying to find the cash provided by operating activities in this section of the statement of cash flows.

Since equipment is a noncurrent asset, cash activity related to the disposal of equipment should be included in the investment activities section of the statement of cash flows. Thus the $6,000 loss shown as a deduction on the income statement is added back to net income, and it will be included later in the investing activities section as part of the proceeds from the sale of equipment. In effect, we are reversing the $6,000 loss because it is not an operating expense.

Here’s how the second adjustment to net income appears in the operating activities section of the statement of cash flows for Home Store, Inc.:

Adjustment Three: Adding and Subtracting Changes in Current Assets and Current Liabilities

Question: What is the third type of adjustment necessary to convert net income to a cash basis?

Answer: The third type of adjustment to net income involves analyzing the changes in all current assets (except cash) and current liabilities from the beginning of the period to the end of the period. Technically it is changes in operating assets and liabilities but most of the time current assets and liabilities will be operating assets and liabilities unless a note tells you differently. These changes are already shown in the far right column of the balance sheet portion of Figure 6.2 “Balance Sheet and Income Statement for Home Store, Inc.”. Two important rules must be followed to determine how the change is reflected as an adjustment to net income. Study these two rules carefully:

- Current assets. Increases in current assets are deducted from net income; decreases in current assets are added to net income. (There is an inverse relationship between the change in a current asset account and how it is shown as an adjustment.)

- Current liabilities. Increases in current liabilities are added to net income; decreases in current liabilities are deducted from net income. (There is a direct relationship between the change in a current liability account and how it is shown as an adjustment.)

Now let’s work through each current asset and current liability line item shown in the balance sheet (Figure 6.2 “Balance Sheet and Income Statement for Home Store, Inc.”) and use these rules to determine how each item fits into the operating activities section as an adjustment to net income.

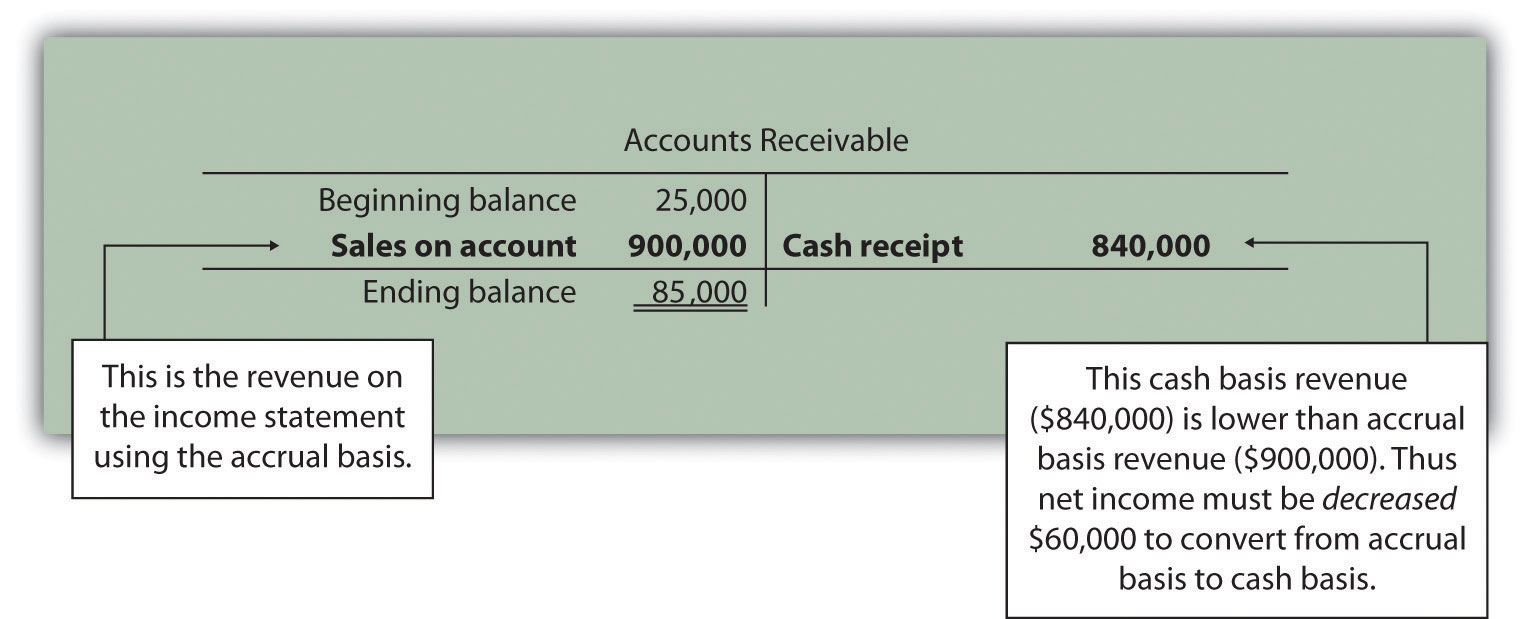

The first current asset line item, cash, shows the change in cash from the beginning of the year to the end of year. Cash decreased by $98,000. The goal of the statement of cash flows is to show what caused this $98,000 decrease. This amount will appear in step 4 when we reconcile the beginning cash balance to the ending cash balance. The next line item is accounts receivable.

Accounts receivable (current asset) increased by $60,000. The current asset rule states that increases in current assets are deducted from net income. Thus $60,000 is deducted from net income in the operating activities section of the statement of cash flows. Here’s why.

Assume all Home Store’s sales shown on the income statement are credit sales (each sale required a debit to accounts receivable and a credit to sales). The beginning accounts receivable balance of $25,000 is increased by $900,000 for credit sales made during the year, resulting in $925,000 in total receivables to be collected. Since $85,000 in accounts receivable remains at the end of the year, $840,000 in cash was collected (= $925,000 − $85,000). On a cash basis, Home Store, Inc., should show $840,000 in revenue rather than $900,000. Thus net income must be reduced by $60,000 (= $900,000 revenue using accrual basis − $840,000 revenue using cash basis). The accounts receivable T-account shown in the following provides further clarification.

Here’s how the accounts receivable adjustment to net income appears in the operating activities section of the statement of cash flows for Home Store, Inc.:

We will continue analyzing each current asset and current liability item in the balance sheet shown in Figure 6.2 “Balance Sheet and Income Statement for Home Store, Inc.” and present the resulting adjustments and completed operating activities section at the end of our analysis in Figure 6.4 “Operating Activities Section of Statement of Cash Flows (Home Store, Inc.)”.

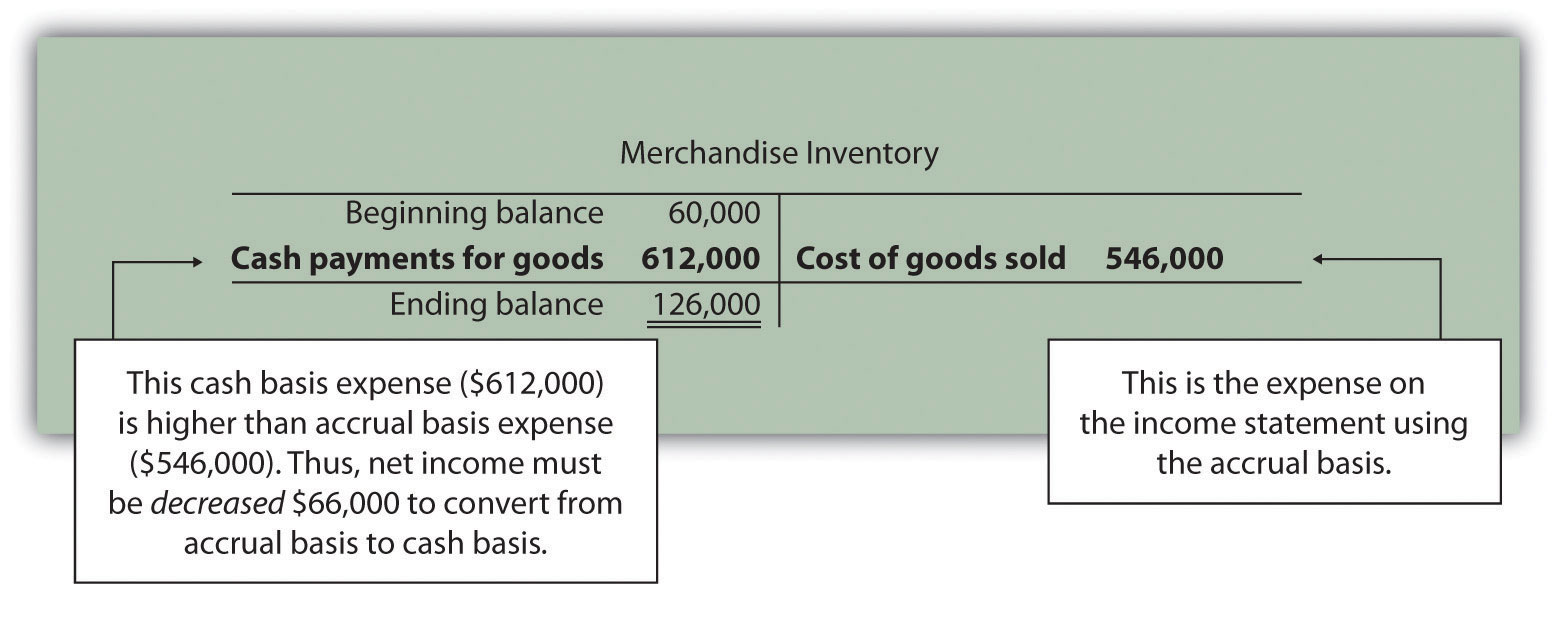

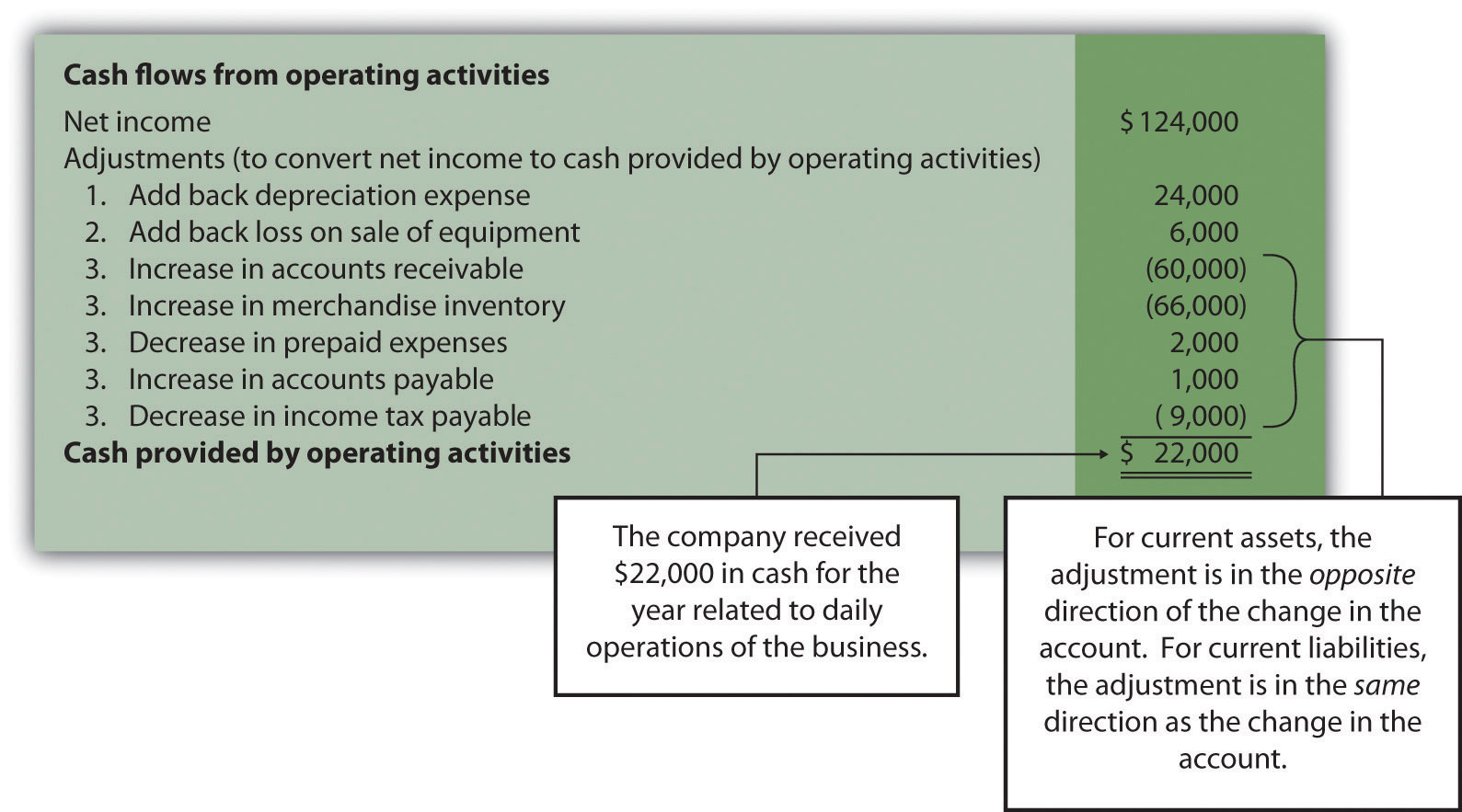

Merchandise inventory (current asset) increased by $66,000. Because the current asset rule states that increases in current assets are deducted from net income, $66,000 is deducted from net income in the operating activities section of the statement of cash flows. To explain why, let’s assume Home Store, Inc., pays cash for all purchases of merchandise inventory. If the merchandise inventory account increases over time, more goods are purchased than are sold. Because merchandise inventory at Home Store, Inc., increased $66,000 and cost of goods sold totaled $546,000, the company must have purchased inventory with a cost of $612,000 during the period (= $66,000 + $546,000). Thus more cash was paid for merchandise ($612,000) than was reflected on the income statement as cost of goods sold ($546,000). If expenses are higher using a cash basis, the adjustment must decrease net income. Therefore $66,000 is deducted from net income in the operating activities section of the statement of cash flows. This information is summarized in the merchandise inventory T-account in the following.

Prepaid expenses (current asset) decreased by $2,000. Because the current asset rule states that decreases in current assets are added to net income, $2,000 is added to net income in the operating activities section of the statement of cash flows. This is because cash paid for these expenses was lower than the expenses recognized on the income statement using the accrual basis. Since expenses are $2,000 lower using the cash basis, net income must be increased by $2,000.

Key Point

Important Operating/Current Asset Rule

When preparing the operating activities section of the statement of cash flows, increases in current/operating assets are deducted from net income; decreases in current/operating assets are added to net income.

Question: Now that we know how to handle the change in current/operating assets when preparing the operating activities section of the statement of cash flows, what do we do with current/operating liabilities?

Answer: The current liability rule is a bit different than the current asset rule as described next.

Accounts payable (current liability) increased by $1,000. Because the current liability rule states that increases in current liabilities are added to net income, $1,000 is added to net income in the operating activities section of the statement of cash flows. An increase in accounts payable signifies that Home Store, Inc., recorded more as an expense on the income statement (accrual basis) than the company paid in cash (cash basis). Since expenses are lower using the cash basis, net income must be increased by $1,000.

Income tax payable (current liability) decreased by $9,000. Because the current liability rule states that decreases in current liabilities are deducted from net income, $9,000 is deducted from net income in the operating activities section of the statement of cash flows. A decrease in income tax payable signifies that Home Store, Inc., paid more for income taxes (cash basis) than the company recorded as an expense on the income statement (accrual basis). Since expenses are higher using the cash basis, net income must be decreased by $9,000.

Key Point

Important Current/Operating Liability Rule

When preparing the operating activities section of the statement of cash flows, increases in current/operating liabilities are added to net income; decreases in current/operating liabilities are deducted from net income.

Question: What does the operating activities section of the statement of cash flows look like for Home Store, Inc.?

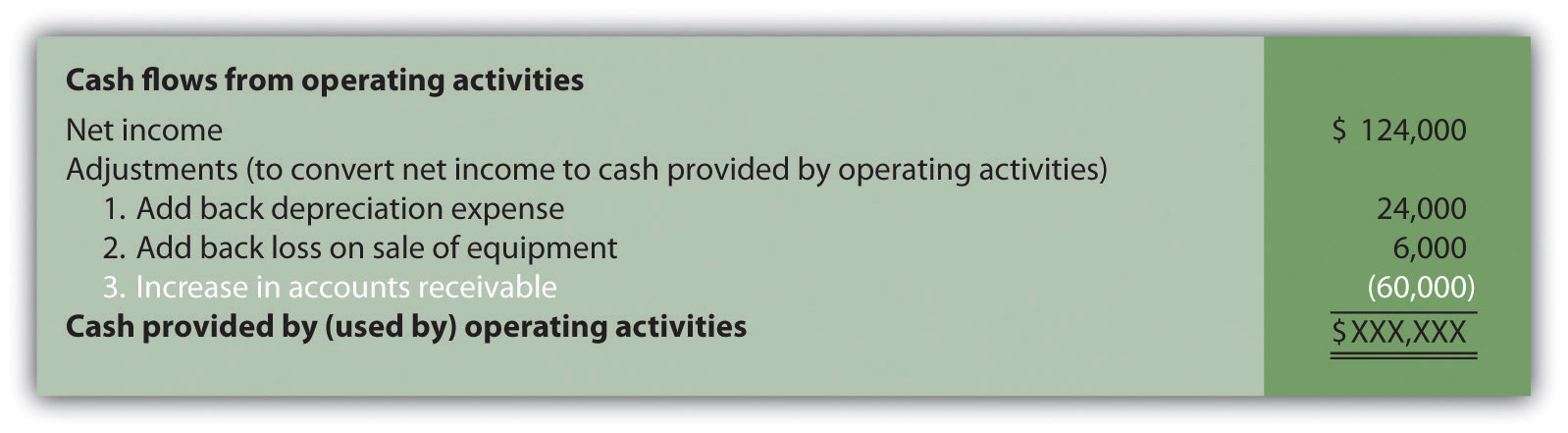

Answer: Figure 6.4 “Operating Activities Section of Statement of Cash Flows (Home Store, Inc.)” shows the completed operating activities section of the statement of cash flows for Home Store. Inc. The most important line is at the bottom, which shows cash of $22,000 was generated during the year from daily operations of the business. Notice this amount is significantly lower than the net income amount of $124,000 reported on the income statement. Study Figure 6.4 “Operating Activities Section of Statement of Cash Flows (Home Store, Inc.)” carefully noting the three types of adjustments made to net income.

Figure 6.4 Operating Activities Section of Statement of Cash Flows (Home Store, Inc.)

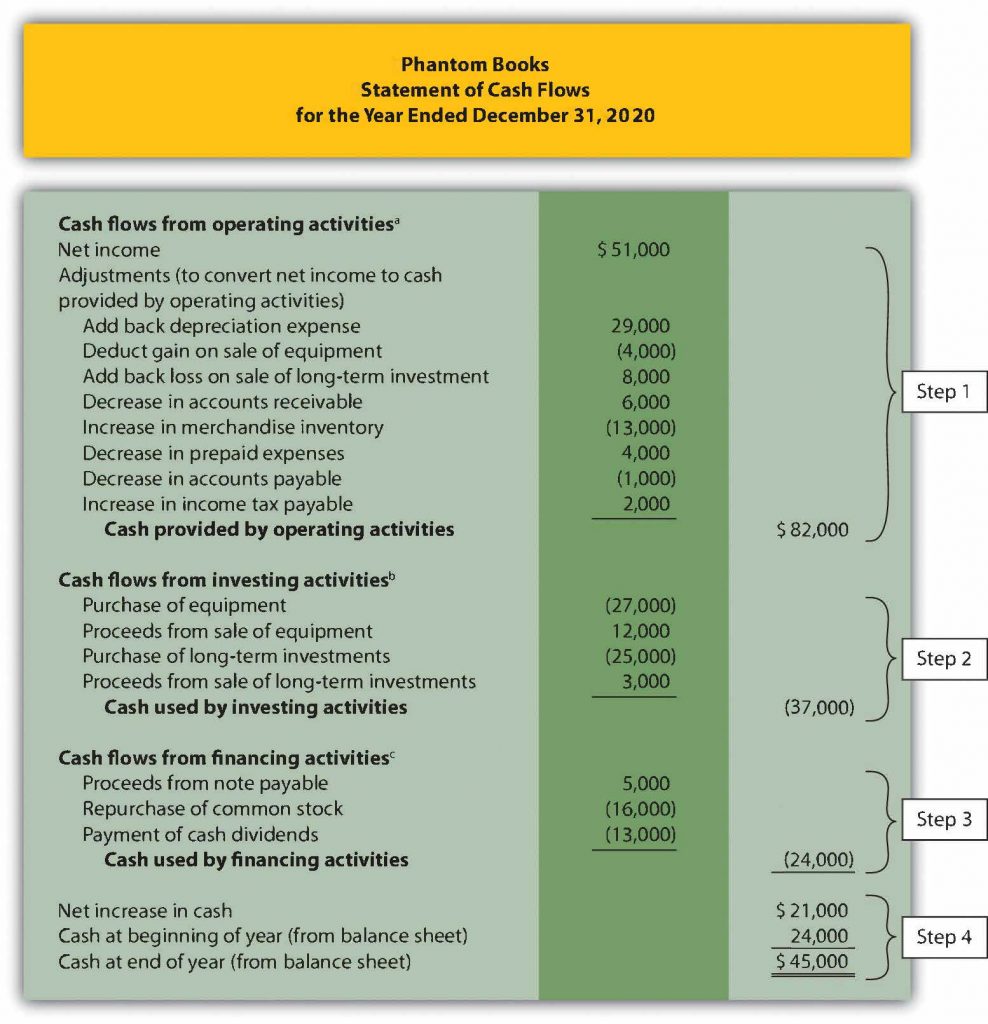

Check Yourself

This check yourself will use the data presented as follows for Phantom Books. Each review problem corresponds to the four steps required to prepare a statement of cash flows.

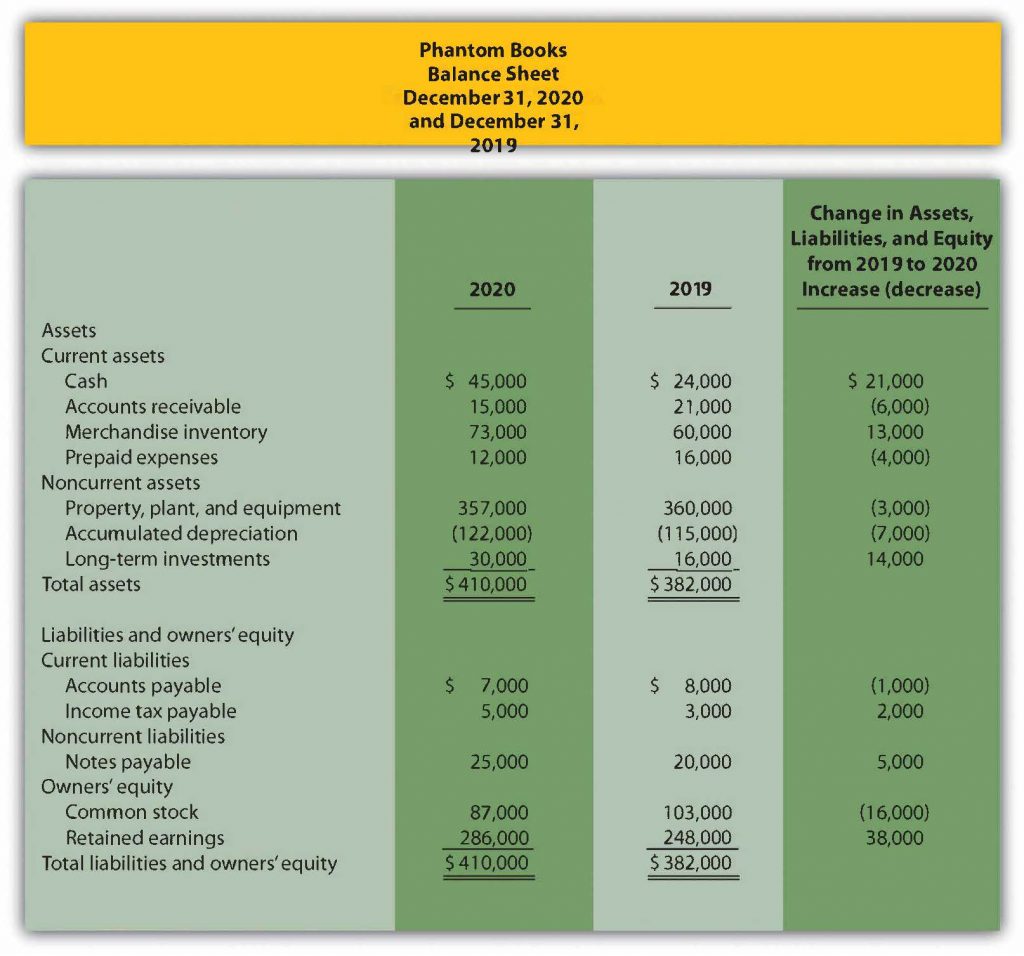

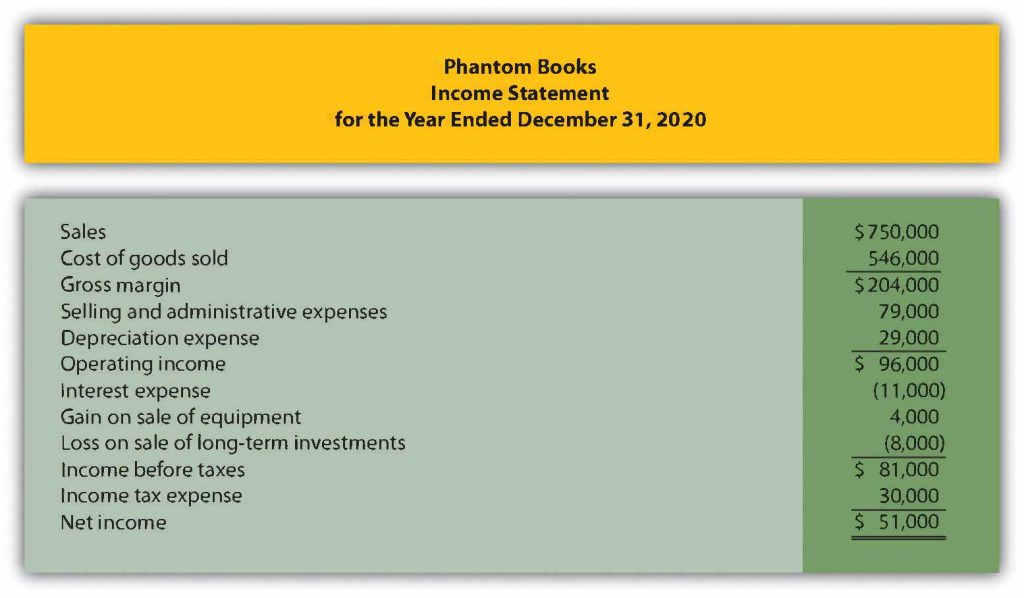

Phantom Books is a retail store that sells new and used books. Phantom’s most recent balance sheet, income statement, and other important information for 2020 are presented in the following.

Additional data for 2020 include the following:

- Sold equipment with a book value of $8,000 (= $30,000 cost − $22,000 accumulated depreciation) for $12,000 cash

- Purchased equipment for $27,000 cash

- Sold long-term investments with an original cost of $11,000 for $3,000 cash

- Purchased long-term investments for $25,000 cash

- Signed a note with the bank for $5,000 cash. No principal amounts were paid during the year

- Repurchased common stock (treasury stock) for $16,000 cash. No new common stock was issued

- Declared and paid $13,000 in cash dividends

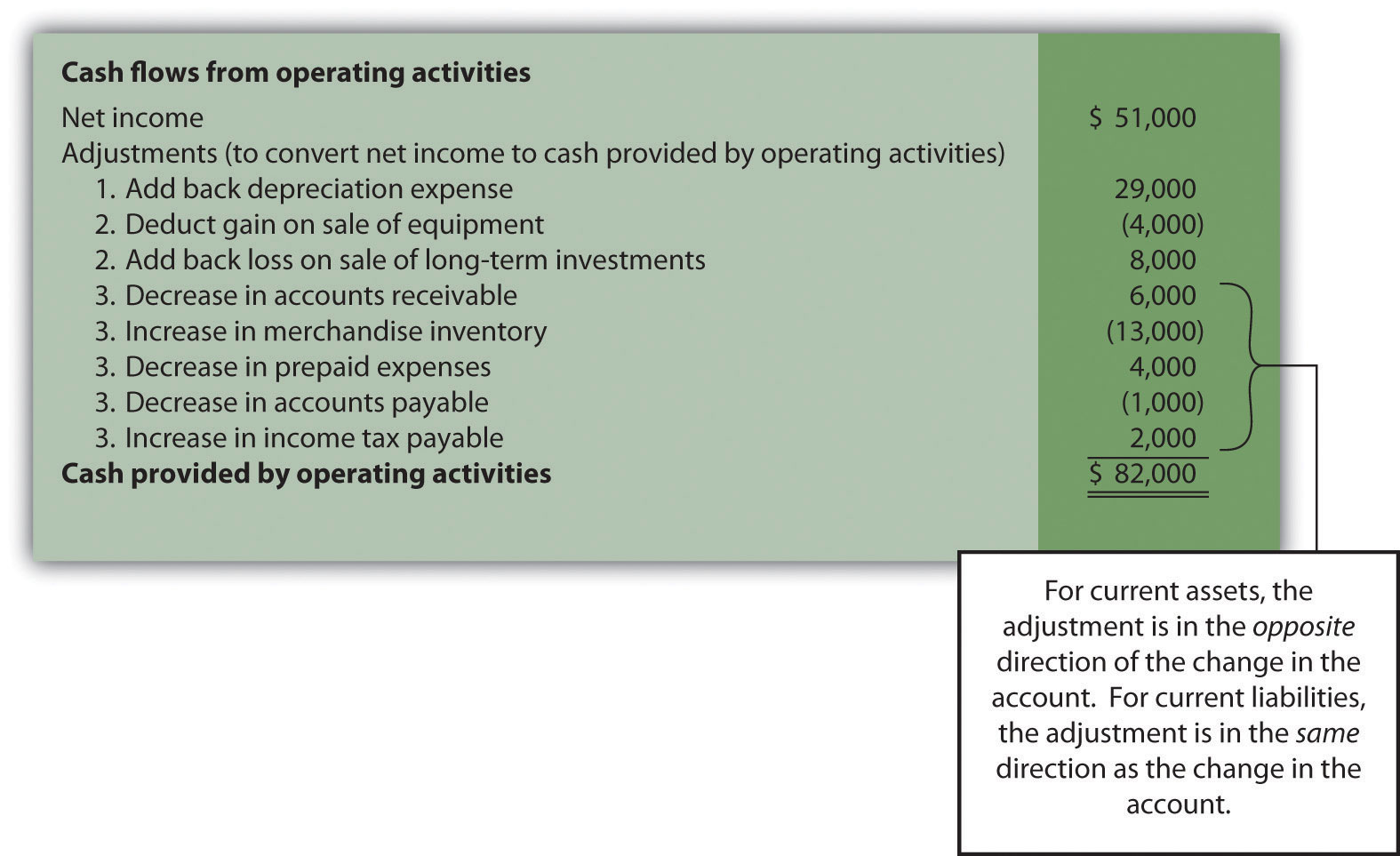

- Prepare the operating activities section of the statement of cash flows for Phantom Books using the indirect method. Follow the format presented in Figure 6.4 “Operating Activities Section of Statement of Cash Flows (Home Store, Inc.)”.

- How much cash did Phantom Books generate from operating activities for the year?

Solution

-

Start with net income from the income statement; make the appropriate adjustments for (1) noncash expenses, such as depreciation and amortization; (2) gains and losses related to investing activities; and (3) changes in current assets other than cash and current liabilities. The operating activities section of the statement of cash flows for Phantom Books appears as follows.

- Cash totaling $82,000 was generated from the company’s operating activities during the year.

Before moving on to step 2, note that investing and financing activities sections always use the same format whether the operating activities section is presented using the direct method or indirect method.

Step 2: Prepare the Investing Activities Section

Question: Now that we have completed the operating activities section for Home Store, Inc., the next step is to prepare the investing activities section. What information is used for this section, and how is it prepared?

Answer: The investing activities section of the statement of cash flows focuses on cash activities related to noncurrent assets. Review the noncurrent asset section of Home Store, Inc.’s balance sheet presented in Figure 6.2 “Balance Sheet and Income Statement for Home Store, Inc.”. Three noncurrent asset line items must be analyzed to determine how to present cash flow information in the investing activities section.

Property, plant, and equipment increased by $46,000. The additional information provided for 2020 indicates two types of transactions caused this increase. First, the company purchased equipment for $67,000 cash. Home Store, Inc., made the following journal entry for this transaction:

Second, the company sold equipment for $5,000 cash (often called a disposal of equipment). This equipment was on the books at an original cost of $21,000 with accumulated depreciation of $10,000. Home Store, Inc., made the following journal entry for this transaction:

Notice the two entries to property, plant, and equipment shown previously. The net effect of these 2 entries is an increase of $46,000 (= $67,000 − $21,000). This is summarized in the following T-account:

Question: How is this property, plant, and equipment information used in the investing activities section of the statement of cash flows for Home Store, Inc.?

Answer: First, the purchase of equipment for $67,000 cash is shown as a decrease in cash. Second, the sale of equipment for $5,000 is shown as an increase in cash. It is not enough to simply show a cash outflow of $62,000 in the investing activities section of the statement of cash flows (= $67,000 − $5,000). Instead, Home Store, Inc., must show the components of this cash outflow as separate line items in the statement of cash flows as required by U.S. GAAP. The formal presentation of this information in the investing activities section is shown later in Figure 6.5 “Investing Activities Section of Statement of Cash Flows (Home Store, Inc.)”.

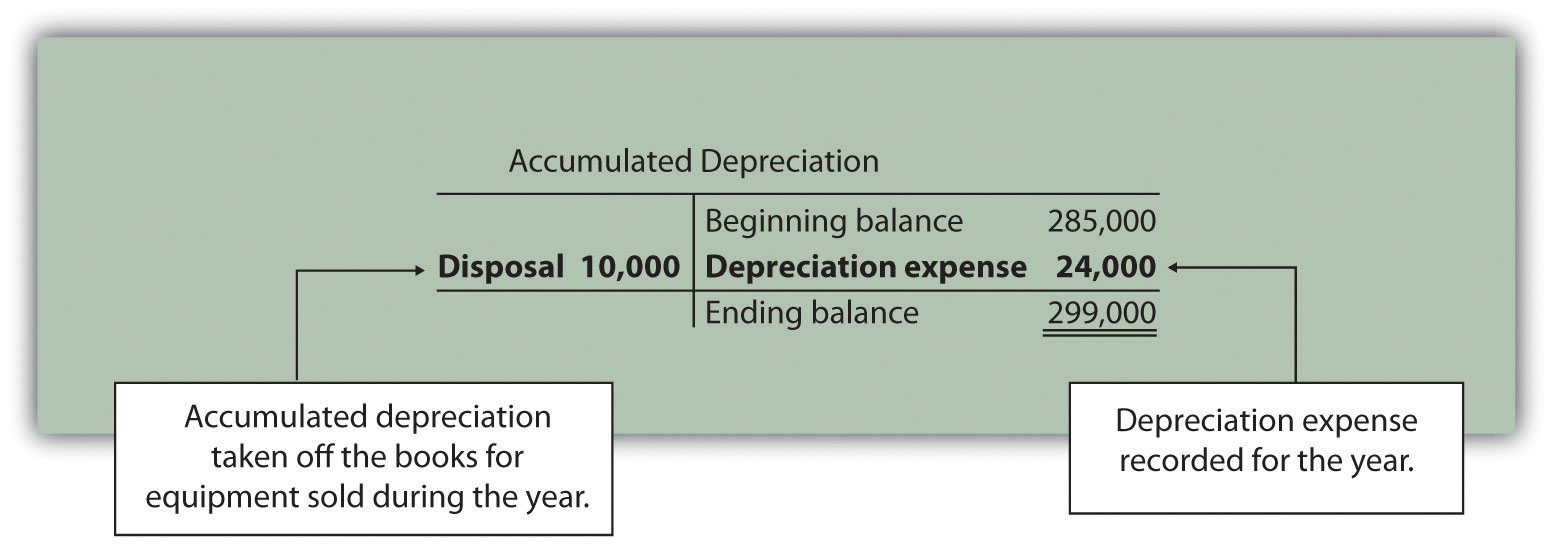

Accumulated depreciation decreased noncurrent assets by $14,000. This contra asset account is not typical of the other asset accounts shown on Home Store, Inc.’s balance sheet since contra asset accounts have the effect of reducing assets. Thus as this accumulated depreciation account increases, it further reduces overall assets. Terminology can get confusing, so here is a simple way to look at it. The higher the account goes; the more it reduces assets. This is why the change column shows this account as decreasing assets.

Two items caused the change in the accumulated depreciation account. First, the sale of equipment during the year caused the company to take $10,000 in accumulated depreciation off the books. Second, $24,000 in depreciation expense was recorded during the year (with a corresponding entry to accumulated depreciation). This information is summarized in the following T-account:

Question: How is accumulated depreciation information used in the statement of cash flows for Home Store, Inc.?

Answer: This information is already reflected in two places (the work has already been done!). First, depreciation expense is a noncash expense and is added back to net income in the operating activities section of the statement of cash flows (see Figure 6.4 “Operating Activities Section of Statement of Cash Flows (Home Store, Inc.)”). Second, $10,000 of accumulated depreciation related to disposals is included as part of the $5,000 proceeds from the sale of equipment in the investing activities section of the statement of cash flows (see Figure 6.5 “Investing Activities Section of Statement of Cash Flows (Home Store, Inc.)”). Here are the components of the equipment sale that support the $5,000 in cash proceeds shown in the investing activities section:

Long-term investments increased by $12,000. The additional information provided for 2020 indicates there were no sales of long-term investments during the year. The increase of $12,000 is solely from purchasing long-term investments with cash. Thus the purchase of long-term investments for $12,000 is shown as a decrease in cash in the investing activities section.

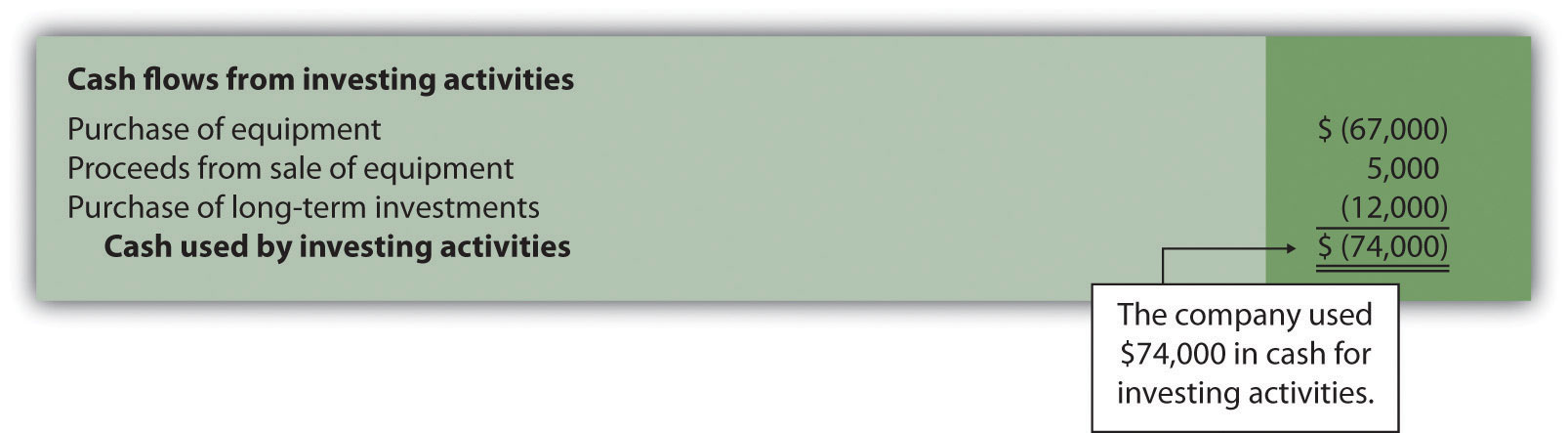

Figure 6.5 “Investing Activities Section of Statement of Cash Flows (Home Store, Inc.)” shows the three investing activities described previously: (1) a $67,000 decrease in cash from the purchase of equipment, (2) a $5,000 increase in cash from the sale of equipment, and (3) a $12,000 decrease in cash from the purchase of long-term investments. Examine Figure 6.5 “Investing Activities Section of Statement of Cash Flows (Home Store, Inc.)” carefully noting the impact these three items have on cash and the resulting cash used by investing activities of $74,000.

Figure 6.5 Investing Activities Section of Statement of Cash Flows (Home Store, Inc.)

Check Yourself

Using the information presented earlier for Phantom Books:

- Prepare the investing activities section of the statement of cash flows for Phantom Books. Follow the format presented in Figure 6.5 “Investing Activities Section of Statement of Cash Flows (Home Store, Inc.)”.

- How much cash did Phantom Books use for investing activities during the year?

Solution

-

Start by analyzing changes in noncurrent assets on the balance sheet. Then prepare the investing activities section of the statement of cash flows. The cash flows related to each noncurrent asset account are underlined as follows.

Property, plant, and equipment decreased by $3,000. Additional data provided indicate 2 items caused this change: (1) equipment was purchased for $27,000 cash, causing a $27,000 increase in the account; and (2) equipment with an original cost of $30,000 was sold for $12,000 cash, causing a $30,000 decrease in the account. The net effect of these 2 items on the property, plant, and equipment account is a decrease of $3,000 (= $27,000 purchase − $30,000 original cost of equipment sold). The impact these items have on cash is reflected in the investing activities section of the statement of cash flows by showing a $27,000 cash outflow for the purchase of equipment and a $12,000 cash inflow from the sale of equipment.

Accumulated depreciation decreased assets by $7,000. Two items caused this change: (1) the sale of equipment caused the company to take $22,000 in accumulated depreciation off the books—this was the accumulated depreciation on the books for the equipment sold, and (2) $29,000 in depreciation expense was recorded during the year, with a corresponding entry to accumulated depreciation. Neither of these entries to accumulated depreciation impacts the investing activities section. However, $29,000 in depreciation expense is a noncash expense and is added back to net income in the operating activities section.

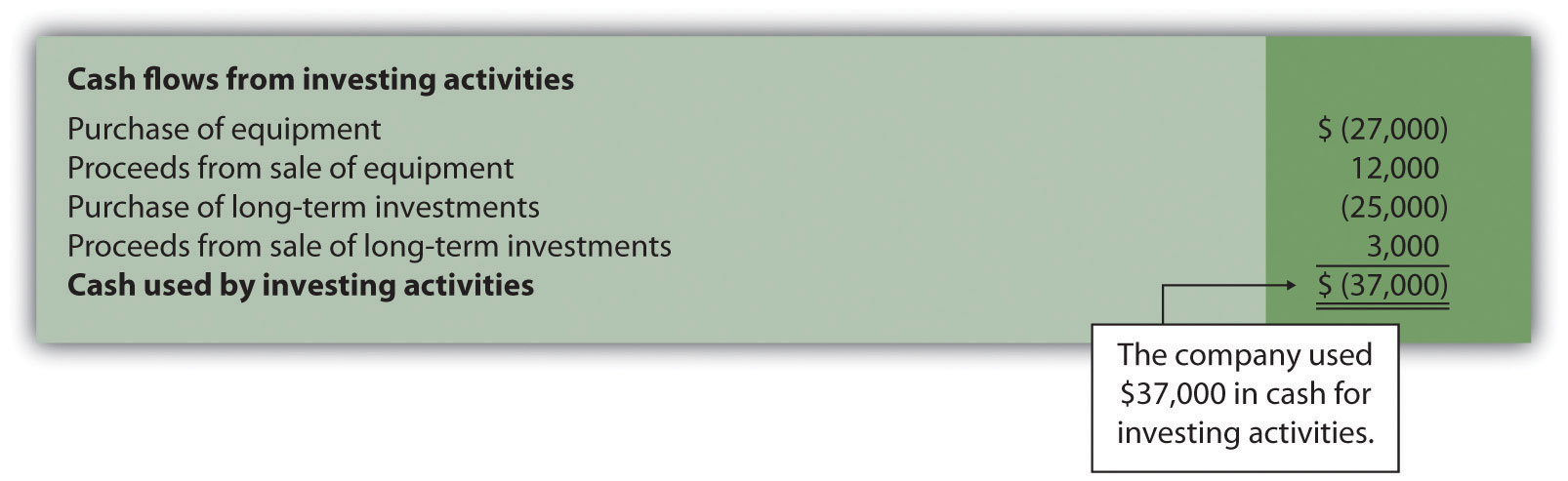

Long-term investments increased by $14,000. Additional data provided indicate 2 items caused this change: (1) long-term investments with an original cost of $11,000 were sold for $3,000 cash, and (2) long-term investments were purchased for $25,000 cash. The net effect of these 2 items on the long-term investments account is an increase of $14,000 (= $25,000 purchase − $11,000 original cost of investments sold). The impact these items have on cash is reflected in the investing activities section of the statement of cash flows by showing a $25,000 cash outflow for the purchase of investments, and a $3,000 cash inflow from the sale of investments.

The investing activities section of the statement of cash flows for Phantom Books is shown as follows:

- Cash totaling $37,000 was used for investing activities during the year.

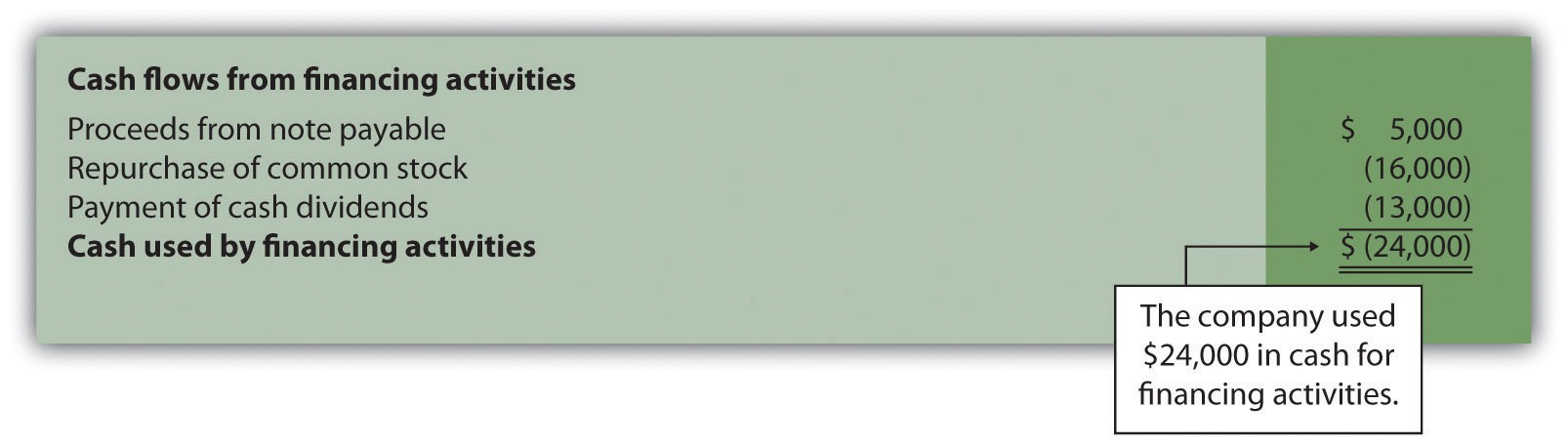

Step 3: Prepare the Financing Activities Section

Question: Now that we have completed the operating and investing activities sections for Home Store, Inc., the next step is to prepare the financing activities section. What information is used for this section, and how is it prepared?

Answer: The financing activities section of the statement of cash flows focuses on cash activities related to noncurrent liabilities and owners’ equity (i.e., cash activities related to long-term company financing). Review the noncurrent liability and owners’ equity sections of Home Store, Inc.’s balance sheet presented in Figure 6.2 “Balance Sheet and Income Statement for Home Store, Inc.”. One noncurrent liability item (bonds payable) and two owners’ equity items (common stock and retained earnings) must be analyzed to determine how to present cash flow information in the financing activities section. The formal presentation of this information in the financing activities section is shown later in Figure 6.6 “Financing Activities Section of Statement of Cash Flows (Home Store, Inc.)”.

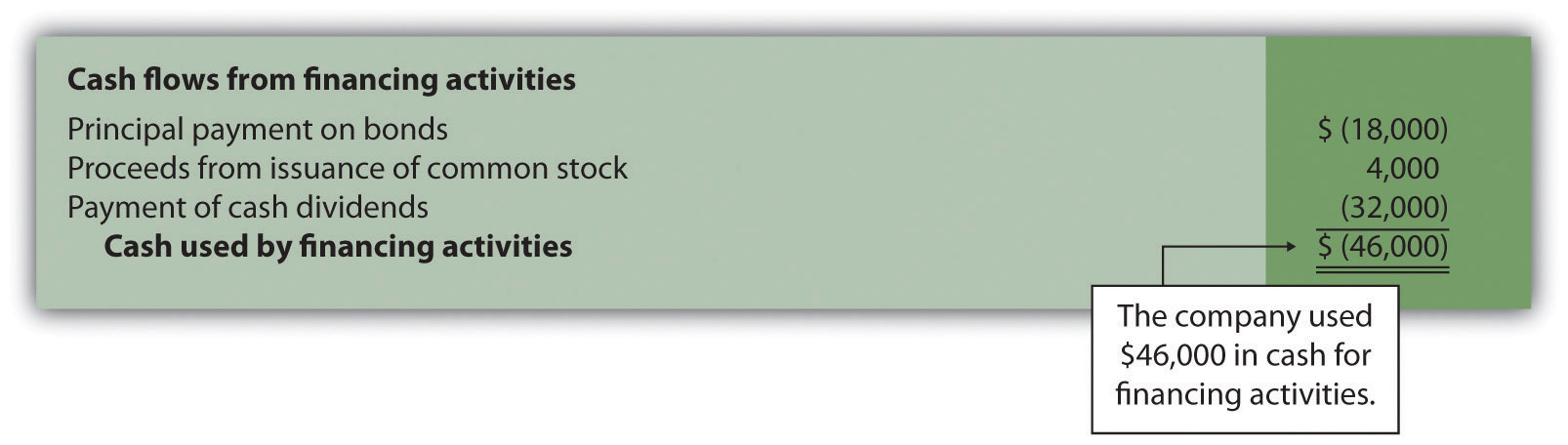

Bonds payable decreased by $18,000. The additional information provided for 2020 indicates Home Store, Inc., paid off bonds during the year with a principal amount of $18,000. This is reflected in the financing activities section of the statement of cash flows as an $18,000 decrease in cash.

Common stock increased by $4,000. The additional information provided for 2020 indicates the company issued common stock for $4,000 cash. This is reflected in the financing activities section of the statement of cash flows as $4,000 increase in cash.

Retained earnings increased by $92,000. Two items caused this increase: (1) net income of $124,000 increased retained earnings, and (2) cash dividends paid totaling $32,000 decreased retained earnings. The net effect of these two entries is an increase of $92,000 (= $124,000 net income − $32,000 cash dividends).

Question: How is this information used in the statement of cash flows?

Answer: Net income is already included at the top of the operating activities section as shown in Figure 6.4 “Operating Activities Section of Statement of Cash Flows (Home Store, Inc.)”. Cash dividends are included in the financing activities section as a $32,000 decrease in cash.

Figure 6.6 “Financing Activities Section of Statement of Cash Flows (Home Store, Inc.)” shows the three financing activities described previously: (1) an $18,000 decrease in cash from paying off the principal amount of bonds, (2) a $4,000 increase in cash from the issuance of common stock, and (3) a $32,000 decrease in cash from the payment of cash dividends. Examine Figure 6.6 “Financing Activities Section of Statement of Cash Flows (Home Store, Inc.)” carefully noting the impact these three items have on cash and the resulting cash used by financing activities of $46,000.

Figure 6.6 Financing Activities Section of Statement of Cash Flows (Home Store, Inc.)

Significant Noncash Investing and Financing Activities

Question: Some organizations have noncash activities involving the exchange of one noncurrent or owners’ equity balance sheet item for another (e.g., the issuance of common stock for a building; or the issuance of common stock in exchange for bonds held by creditors). Do these types of transactions appear in the statement of cash flows?

Answer: These exchanges do not involve cash and thus do not appear directly on the statement of cash flows. However, if the amount is significant, this type of exchange must be disclosed as a separate note below the statement of cash flows or in the notes to the financial statements.

Check Yourself

Using the information presented for Phantom Books do the following:

- Prepare the financing activities section of the statement of cash flows for Phantom Books. Follow the format presented in Figure 6.6 “Financing Activities Section of Statement of Cash Flows (Home Store, Inc.)”.

- How much cash did Phantom Books use for financing activities during the year?

Solution

-

Start by analyzing changes in noncurrent liabilities and owners’ equity on the balance sheet. Then prepare the financing activities section of the statement of cash flows. The cash flows related to each noncurrent liability and owners’ equity account are underlined as follows.

Note payable increased by $5,000. Additional data provided indicate the company signed a note with the bank and received $5,000 cash. This is reflected in the financing activities section as a $5,000 cash inflow.

Common stock decreased by $16,000. Additional data provided indicate the company repurchased common stock for $16,000 cash. This is reflected in the financing activities section as a $16,000 cash outflow. This purchase of company stock would be shown as Treasury Stock which would reduce stock holders equity.

Retained earnings increased by $38,000. Two items caused this increase: (1) net income of $51,000 increased retained earnings and (2) cash dividends paid totaling $13,000 (provided as additional data) decreased retained earnings. The net effect of these 2 items is an increase of $38,000 (= $51,000 net income − $13,000 cash dividends). Net income is already included at the top of the operating activities section. Cash dividends are included in the financing activities section as a $13,000 cash outflow.

The financing activities section of the statement of cash flows for Phantom Books is shown as follows:

- Cash totaling $24,000 was used for financing activities during the year.

Step 4: Reconcile the Change in Cash

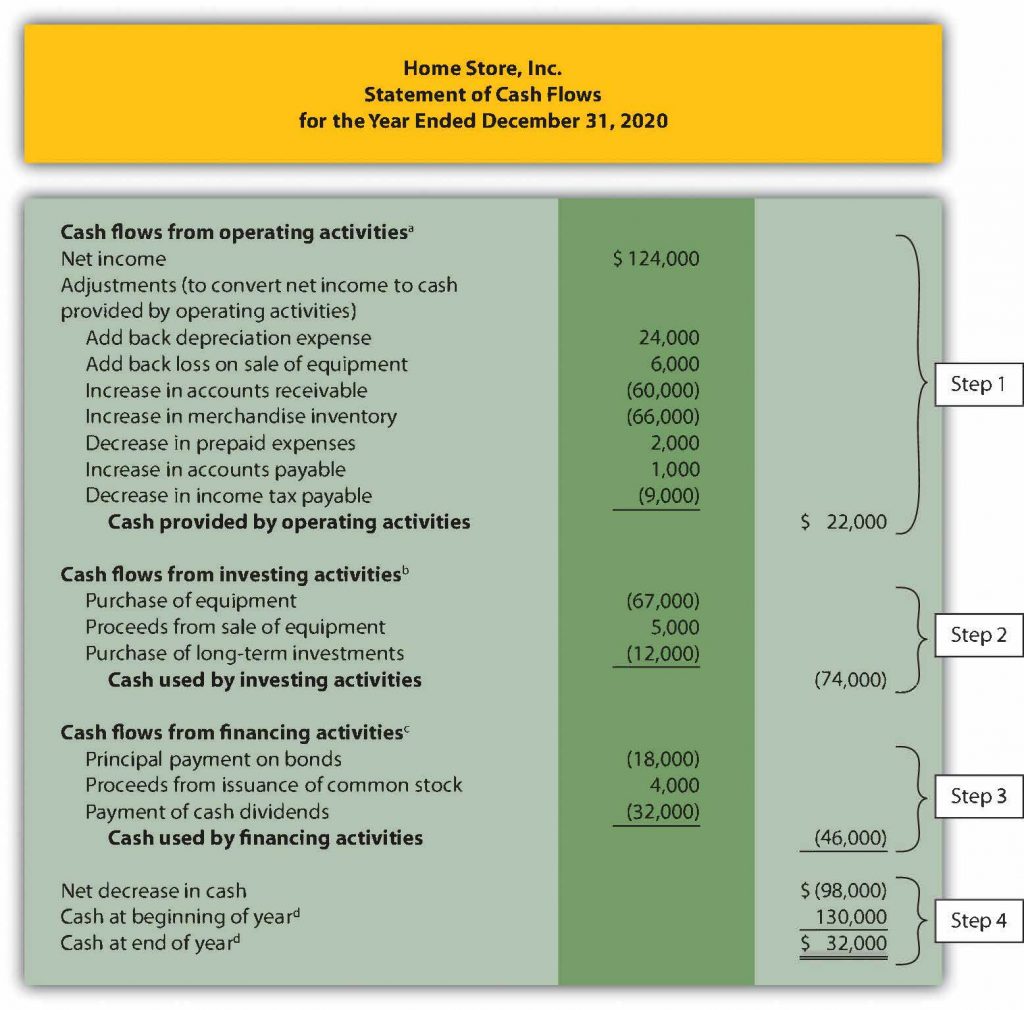

Question: We’re almost done with Home Store, Inc.’s statement of cash flows. What is the fourth and final step needed to complete the statement of cash flows?

Answer: The final step is to show that the change in cash on the statement of cash flows agrees with the change in cash on the balance sheet. As shown at the bottom of the completed statement of cash flows for Home Store, Inc., in Figure 6.7 “Statement of Cash Flows (Home Store, Inc.)”, the net decrease in cash of $98,000 shown on this statement (= $22,000 increase from operating activities − $74,000 decrease from investing activities − $46,000 decrease from financing activities) agrees with the change in cash shown on the balance sheet (= $32,000 ending cash balance − $130,000 beginning balance).

Figure 6.7 Statement of Cash Flows (Home Store, Inc.)

a From Figure 6.4 “Operating Activities Section of Statement of Cash Flows (Home Store, Inc.)”.

b From Figure 6.5 “Investing Activities Section of Statement of Cash Flows (Home Store, Inc.)”.

c From Figure 6.6 “Financing Activities Section of Statement of Cash Flows (Home Store, Inc.)”.

d From Figure 6.2 “Balance Sheet and Income Statement for Home Store, Inc.”.

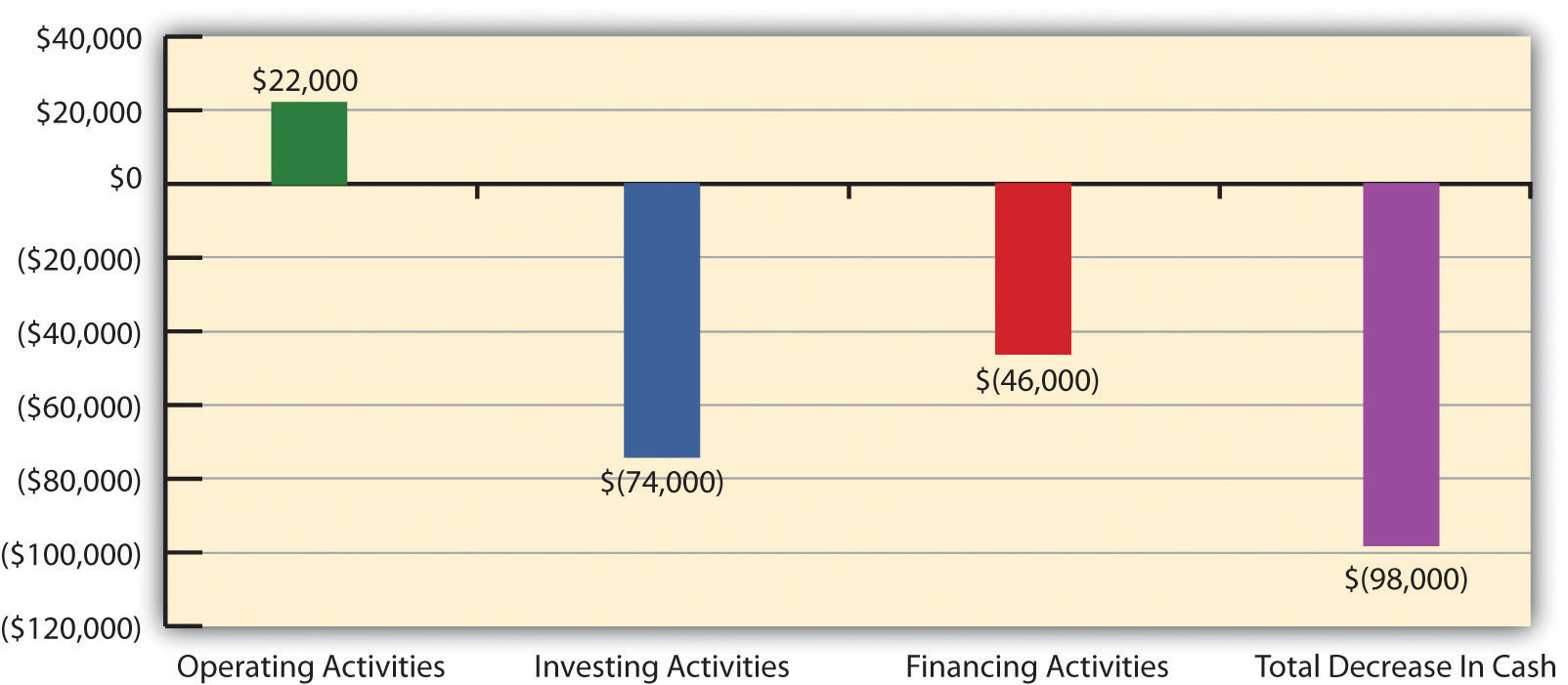

Figure 6.8 “Cash Flows at Home Store, Inc.” provides a summary of cash flows for operating activities, investing activities, and financing activities for Home Store, Inc., along with the resulting total decrease in cash of $98,000.

Figure 6.8 Cash Flows at Home Store, Inc.

Exercises

Review Problem 12.7

Using the information presented for Phantom Books, prepare a complete statement of cash flows for Phantom Books. Follow the format presented in Figure 6.7 “Statement of Cash Flows (Home Store, Inc.)”.

Solution

a From earlier check yourself

b From earlier check yourself

c From earlier check yourself

Home Store, Inc., Update

Recall the dialogue at Home Store, Inc., between John (CEO), Steve (treasurer), and Linda (CFO). John was concerned about the company’s drop in cash from $130,000 at the beginning of the year to $32,000 at the end of the year. He asked Linda to investigate and wanted to know how much cash was generated from daily operations during the year. The group reconvened the following week. As you read the dialogue that follows, refer to Figure 6.7 “Statement of Cash Flows (Home Store, Inc.)”; it is the statement of cash flows that Linda prepared for the meeting.

John (CEO):

Welcome, everyone. Linda, what information do you have for us regarding the company’s cash flow?

Linda (CFO):

I’ve completed a statement of cash flows for the year—here are copies for your review (see Figure 6.7 “Statement of Cash Flows (Home Store, Inc.)”). This statement tells us about the company’s cash activities during the year and ultimately explains why cash decreased by $98,000.

John:

How much cash did we generate from ongoing operations for the year?

Linda:

That can be found in the top portion of the statement under “cash flows from operating activities.” We generated $22,000 from operating activities.

Steve (Treasurer):

You’re kidding! We had net income totaling $124,000 but only generated $22,000 in cash?

John:

That does seem like a huge disparity. Linda, are you sure this is correct?

Linda:

Yes! The reason cash from operating activities is so much lower than net income is that accounts receivable and merchandise inventory increased significantly from the beginning of the year to the end of the year. In fact, both accounts more than doubled.

Steve:

The cash tied up in these two areas is definitely hurting our cash flow. We really struggled to meet our cash budgets for accounts receivable collections and inventory purchases.

John:

Clearly, we’ve got to get a handle on receivables and inventory. But even with this huge difference between net income and cash flows from operating activities, we generated $22,000 in cash. This does not explain why cash decreased by $98,000.

Linda:

You’re right, John. Operating activities produced positive cash flow in spite of these receivables and inventory issues. Let’s look further down the statement. Notice we spent $67,000 on equipment and purchased $12,000 in long-term investments.

Steve:

Yes, I recall purchasing a new forklift—the old one was a safety hazard—and purchasing long-term investments at the beginning of the year when our cash balance was on the high side.

Linda:

Once we factor in the cash proceeds from the old equipment, you can see we spent $74,000 in cash for equipment and investments.

John:

Looking back, we probably should have financed the equipment rather than having paid for it all at once. What else can you tell us, Linda?

Linda:

Bonds totaling $18,000 came due during the year, as shown toward the bottom of the statement, and we paid $32,000 in dividends.

Steve:

I realize the board felt cash levels were high enough during 2019 to warrant a large dividend payment in 2020, but we need to cut way back on these dividends in the future.

Linda:

I agree. To answer your question, John, the $98,000 decrease in cash came primarily from the purchase of equipment and long-term investments and payments for bonds and cash dividends.

John:

Thank you, Linda. This provides the information we need to improve cash flow going forward.

As you can see from this dialogue, the statement of cash flows is not only a reporting requirement for most companies, it is also a useful tool for analytical and planning purposes. Next, we will discuss how to use cash flow information to assess performance and help in planning for the future.

Key Takeaways

- The statement of cash flows is prepared using the four steps described in the previous segment. In step 1, the indirect method starts with net income in the operating activities section and makes three types of adjustments to convert net income to a cash basis. The first adjustment is adding back expenses that do not affect cash, such as depreciation. The second adjustment is adding back losses and deducting gains related to investing activities. The third adjustment is adding and subtracting changes in current assets (except cash) and current liabilities using the adjustment rules. Steps 2 and 3 are done by analyzing and presenting cash activities associated with noncurrent assets (investing activities) and noncurrent liabilities and owners’ equity (financing activities). Step 4 shows that the change in cash on the statement of cash flows agrees with the change in cash on the balance sheet.

12.5 Analyzing Cash Flow Information

Learning Objective

- Analyze cash flow information.

Question: Companies and analysts tend to use income statement and balance sheet information to evaluate financial performance. In fact, financial results presented to the investing public typically focus on earnings per share as covered in financial accounting. However, analysis of cash flow information is becoming increasingly important to managers, auditors, and outside analysts. What measures are commonly used to evaluate performance related to cash flows?

Answer: Three common cash flow measures used to evaluate organizations are (1) operating cash flow ratio, (2) capital expenditure ratio, and (3) free cash flow. We will use two large home improvement retail companies, The Home Depot, Inc., and Lowe’s Companies, Inc., to illustrate these measures.

Operating Cash Flow Ratio

Question: The operating cash flow ratio is cash provided by operating activities divided by current liabilities. What does this ratio tell us, and how is it calculated?

Answer: This ratio measures the company’s ability to generate enough cash from daily operations over the course of a year to cover current obligations. Although similar to the commonly used current ratio, this ratio replaces current assets in the numerator with cash provided by operating activities. The operating cash flow ratio is as follows:

Key Equation

Operating cash flow ratio= Cash provided by operating activities / Current liabilities

The numerator, cash provided by operating activities, comes from the bottom of the operating activities section of the statement of cash flows. The denominator, current liabilities, comes from the liabilities section of the balance sheet. (Note that if current liabilities vary significantly from one period to the next, some analysts prefer to use average current liabilities. We will use ending current liabilities unless noted otherwise.)

As with most financial measures, the resulting ratio must be compared to similar companies in the industry to determine whether the ratio is reasonable. Some industries have a large operating cash flow relative to current liabilities (e.g., mature computer chip makers, such as Intel Corporation), while others do not (e.g., startup medical device companies).

The operating cash flow ratio is calculated for Home Depot and Lowe’s in the following using information from each company’s balance sheet and statement of cash flows.

| Cash Provided by Operating Activities | Current Liabilities | Operating Cash Flow Ratio | |

| Lowe’s | 4,296 | 15,182 | .28 |

| Home Depot | 13,723 | 18,375 | .75 |

Home Depot and Lowe’s are in the same industry but Home Depot shows a much higher operating cash flow ratio meaning that meeting current obligations out of operating cash flow will be easier for Home Depot than for Lowe’s.

Capital Expenditure Ratio

Question: The capital expenditure ratio is cash provided by operating activities divided by capital expenditures. What does this ratio tell us, and how is it calculated?

Answer: This ratio measures the company’s ability to generate enough cash from daily operations to cover capital expenditures. A ratio in excess of 1.0, for example, indicates the company was able to generate enough operating cash to cover investments in property, plant, and equipment. The capital expenditure ratio is as follows:

Key Equation

Capital expenditure ratio=Cash provided by operating activities / Capital expenditures

The numerator, cash provided by operating activities, comes from the bottom of the operating activities section of the statement of cash flows. The denominator, capital expenditures, comes from information within the investing activities section of the statement of cash flows.

The capital expenditure ratio is calculated for Home Depot and Lowe’s in the following using information from each company’s statement of cash flows.

| Cash Provided by Operating Activities | Capital Expenditures | Capital Expenditure Ratio | |

| Lowe’s | 4,296 | 1,484 | 2.89 |

| Home Depot | 13,723 | 2,678 | 5.12 |

Since the capital expenditure ratio for each company is well above 1.0, both companies were able to generate enough cash from operating activities to cover investments in property, plant, and equipment (also called fixed assets). Home Depot’s ratio is almost double that of Lowe’s showing that Home Depot spends a much smaller part of its operating cash flow on new property, plant and equipment than Lowe’s does.

Free Cash Flow

Question: Another measure used to evaluate organizations, called free cash flow, is simply a variation of the capital expenditure ratio described previously. What does this measure tell us, and how is it calculated?

Answer: Rather than using a ratio to determine whether the company generates enough cash from daily operations to cover capital expenditures and dividends to shareholders, free cash flow is measured in dollars. Free cash flow is cash provided by operating activities minus capital expenditures minus dividends. The idea is that companies must continue to invest in fixed assets to remain competitive and must pay dividends to keep shareholders happy. Free cash flow provides information regarding how much cash generated from daily operations is left over after investing in fixed assets or paying current dividends so that other investments could be made or the dividends increased. Many organizations, such as Amazon.com, consider this measure to be one of the most important in evaluating financial performance. The free cash flow formula is as follows:

Key Equation

Free cash flow = Cash provided by operating activities − Capital expenditures – Dividends

The cash provided by operating activities comes from the bottom of the operating activities section of the statement of cash flows. The capital expenditures amount comes from information within the investing activities section of the statement of cash flows. The dividends are found in the financing section of the cash flow statement.

The free cash flow amount is calculated for Home Depot and Lowe’s as follows using information from each company’s statement of cash flows.

| Cash Provided by Operating Activities | -Capital Expenditures – Dividends | = Free Cash Flow | |

| Lowe’s | 4,296 | – 1,484 – 1,618 | 1,194 |

| Home Depot | 13,723 | – 2,678 – 5,958 | 5,087 |

Because free cash flow for each company is above zero, both companies were able to generate enough cash from operating activities to cover investments in fixed assets and pay dividends and have some left over to invest elsewhere. This conclusion is consistent with the capital expenditure ratio analysis, which uses the same information to assess the company’s ability to cover fixed asset expenditures.

Formulas for the cash flow performance measures presented in this chapter are summarized in Table 6.1 “Summary of Cash Flow Performance Measures”.

Table 6.1 Summary of Cash Flow Performance Measures

| Operating cash flow ratio= Cash provided by operating activities / Current liabilities |

| Capital expenditure ratio=Cash provided by operating activities / Capital expenditures |

| Free cash flow=Cash provided by operating activities − Capital expenditures – Dividends |

Key Takeaways

- Three measures are often used to evaluate cash flow. The operating cash flow ratio measures the company’s ability to generate enough cash from daily operations over the course of a year to cover current obligations. The formula is as follows:

Operating cash flow ratio=Cash provided by operating activities / Current liabilities

The capital expenditure ratio measures the company’s ability to generate enough cash from daily operations to cover capital expenditures. The formula is as follows:

Capital expenditure ratio=Cash provided by operating activities / Capital expenditures

Free cash flow measures the company’s ability to generate enough cash from daily operations to cover capital expenditures and determines how much cash is remaining to invest elsewhere in the company. The formula is as follows:

Free cash flow = Cash provided by operating activities − Capital expenditures – Dividends

Check Yourself

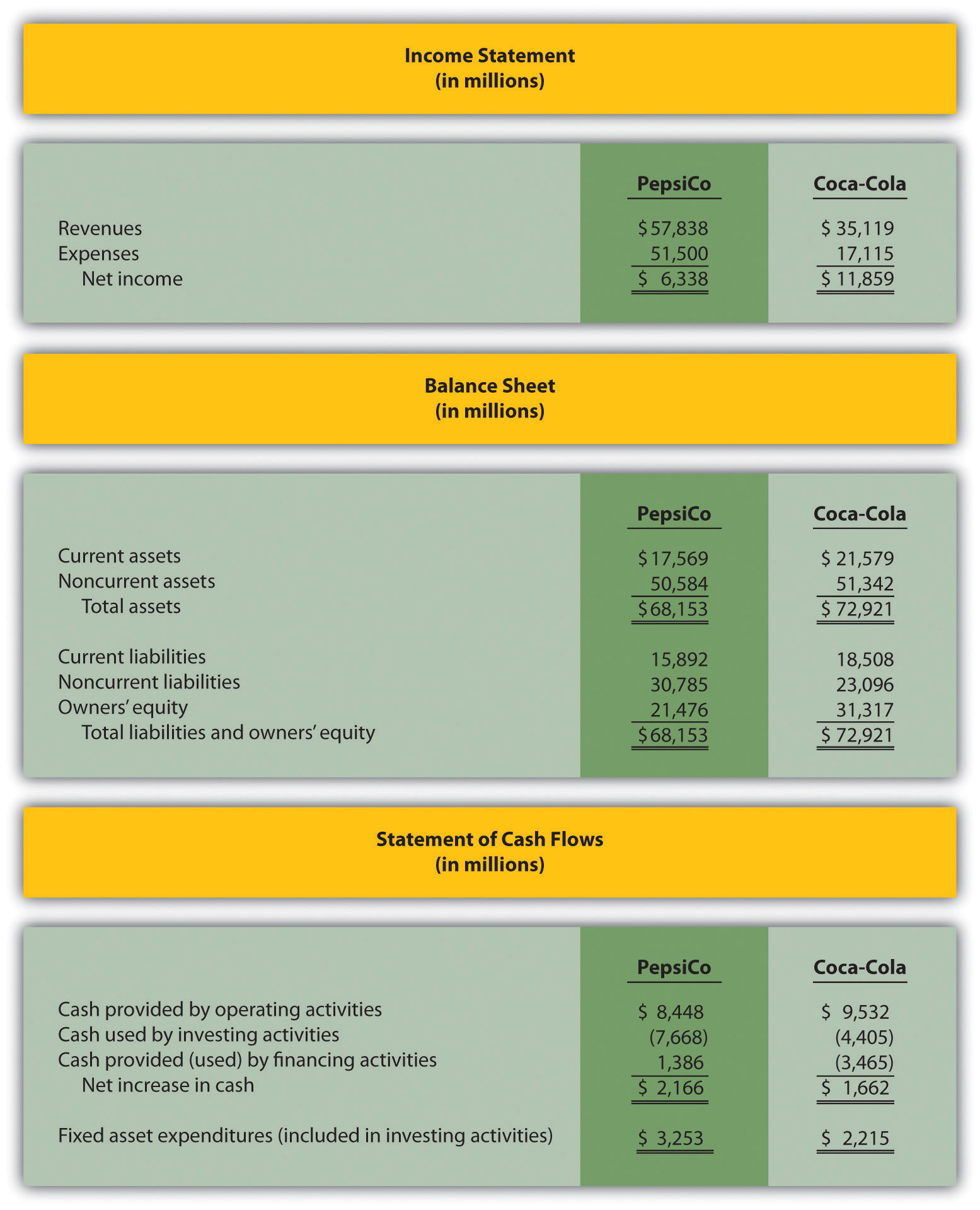

The following financial information is for PepsiCo Inc. and Coca-Cola Company for a recent fiscal year.

PepsiCo paid 5,304 in dividends and Coca-Cola paid 6,845 in dividends. For PepsiCo and Coca Cola, calculate the following measures and comment on your results:

- Operating cash flow ratio

- Capital expenditure ratio (Hint: fixed asset expenditures are the same as capital expenditures.)

- Free cash flow

Solution

All dollar amounts are in millions.

-

The formula for calculating the operating cash flow ratio is as follows:

Operating Cash Flow Ratio=Cash provided by operating activities / Current liabilities

PepsiCo operating cash flow ratio=$8,448÷$15,892=0.53

Coca-Cola operating cash flow ratio=$9,532÷$18,508=0.52PepsiCo generated slightly more cash from operating activities to cover current liabilities than Coca-Cola.

-

The formula for calculating the capital expenditure ratio is as follows:

Capital Expenditure Ratio=Cash provided by operating activities / Capital expenditures

PepsiCo capital expenditure ratio=$8,448÷$3,253=2.60

Coca-Cola capital expenditure ratio=$9,532÷$2,215=4.30Both companies generated more than enough cash from operating activities to cover capital expenditures.

-

The formula to calculate free cash flow is as follows:

Free cash flow = Cash provided by operating activities − Capital expenditures – Dividends

PepsiCo free cash flow=$8,448−$3,253 – 5,304 =$(109)

Coca-Cola free cash flow=$9,532−$2,214 – 6,845 = $473While Coca Cola has cash flow left over after purchasing new property, plant and equipment, Pepsi does not and thus Pepsi would not have the flexibility to pursue other options to improve their business.

End-of-Chapter Exercises

Questions

- Why was the statement of cash flows created by the Financial Accounting Standards Board (FASB)?

- Describe the three classifications of cash flows, and provide examples of activities that would appear in each classification.

- Which section of the statement of cash flows is widely regarded as the most important? Why?

- Briefly describe the four steps required to prepare the statement of cash flows using the indirect method.

- Describe the three adjustments necessary to convert net income to a cash basis using the indirect method. Provide an example for each adjustment.

- Why is depreciation expense added back to net income using the indirect method of preparing the statement of cash flows?

- Assume you are using the indirect method to prepare the operating activities section of the statement of cash flows. Describe the adjustment rules for current assets and current liabilities, and provide one example for each rule.

- You have just completed the statement of cash flows for a company, and the bottom of the statement shows a net increase in cash of $250,000. Describe where this increase should be shown elsewhere in the financial statements.

- Provide an example of a noncash investing or financing activity. Describe how these transactions are disclosed in the financial statements.

- How is the operating cash flow ratio calculated, and what does it tell the user?

- How is the capital expenditure ratio calculated, and what does it tell the user?

- How is free cash flow calculated, and what does it tell the user?

Brief Exercises

-

Evaluating Cash Flows at Home Store, Inc. Refer to the dialogue at Home Store, Inc., presented at the beginning of the chapter and the follow-up dialogue.

Required:

- Why was the CEO concerned about the company’s cash flow?

- Why did the CEO state, “We probably should have financed the equipment rather than having paid for it all at once”?

-

Classifying Cash Flows. Identify whether each of the following items would appear in the operating, investing, or financing activities section of the statement of cash flows. Briefly explain your answer for each item.

- Cash receipts from the sale of common stock

- Cash receipts from the sale of a building

- Cash payments for income taxes

- Cash receipts from issuance of bonds

- Cash payments for the purchase of equipment

-

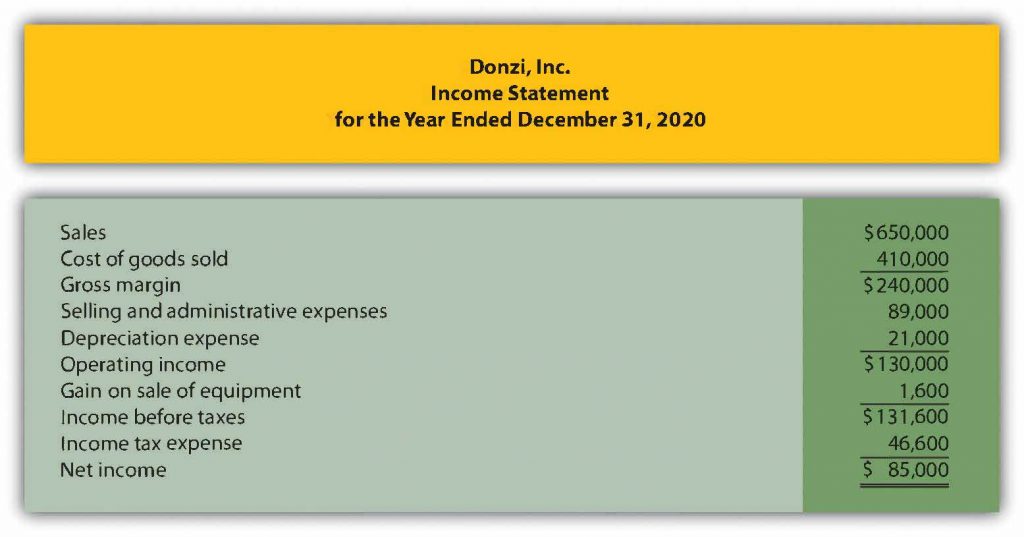

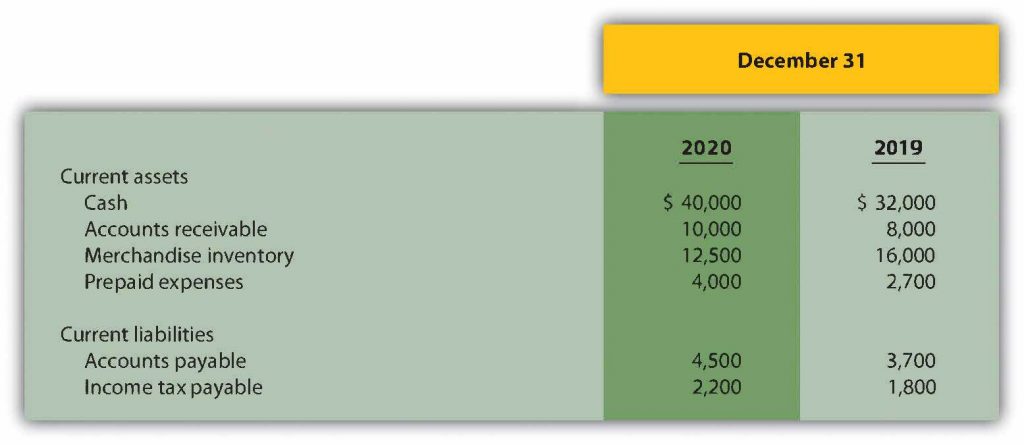

Operating Activities Section Using the Indirect Method. The following income statement and current sections of the balance sheet are for Donzi, Inc.

Required:

Using the indirect method, prepare the operating activities section of the statement of cash flows for Donzi, Inc., for the year ended December 31, 2020. Use the format presented in Figure 6.4 “Operating Activities Section of Statement of Cash Flows (Home Store, Inc.)”.

-

Investing Activities Section. The following information is from the noncurrent asset portion of Santana, Inc.’s balance sheet.

The following activities occurred during 2020:

The following activities occurred during 2020:- Sold equipment with a book value of $3,000 (= $13,000 cost − $10,000 accumulated depreciation) for $4,000 cash and depreciation expense for the year totaled $26,000

- Purchased property for $43,000 cash

- Purchased long-term investments for $15,000 cash

Required:

Prepare the investing activities section of the statement of cash flows for Santana, Inc., for the year ended December 31, 2020. Use the format presented in Figure 6.5 “Investing Activities Section of Statement of Cash Flows (Home Store, Inc.)”.

-

Financing Activities Section. The following information is from the noncurrent liabilities and owners’ equity portions of Canton Company’s balance sheet.

The following activities occurred during 2020:

- Issued bonds for $80,000 cash

- Issued common stock for $100,000 cash

- Earned net income totaling $60,000

- Paid cash dividends totaling $15,000

Required:

Prepare the financing activities section of the statement of cash flows for Canton Company for the year ended December 31, 2020. Use the format presented in Figure 6.6 “Financing Activities Section of Statement of Cash Flows (Home Store, Inc.)”.

-

Cash Flow Measures. The selected information in the following is from Diaz Company’s financial records for the most recent fiscal year.

Current assets $600,000 Current liabilities $250,000 Cash provided by operating activities $700,000 Net income $300,000 Capital expenditures $550,000 Required:

Calculate Diaz Company’s

- Operating cash flow ratio;

- Capital expenditure ratio; and

- Free cash flow.

Exercises:

23. Classifying Cash Flows. Identify whether each of the following items would appear in the operating, investing, or financing activities section of the statement of cash flows. Briefly explain your answer for each item.

-

- Cash payments for the repurchase of common stock

- Cash payments for the purchases of merchandise

- Cash receipts from the collection of interest on loans made to other entities

- Cash receipts from the collection of principal on loans made to other entities

- Cash payments to shareholders for dividends

- Cash payments for the purchase of equipment

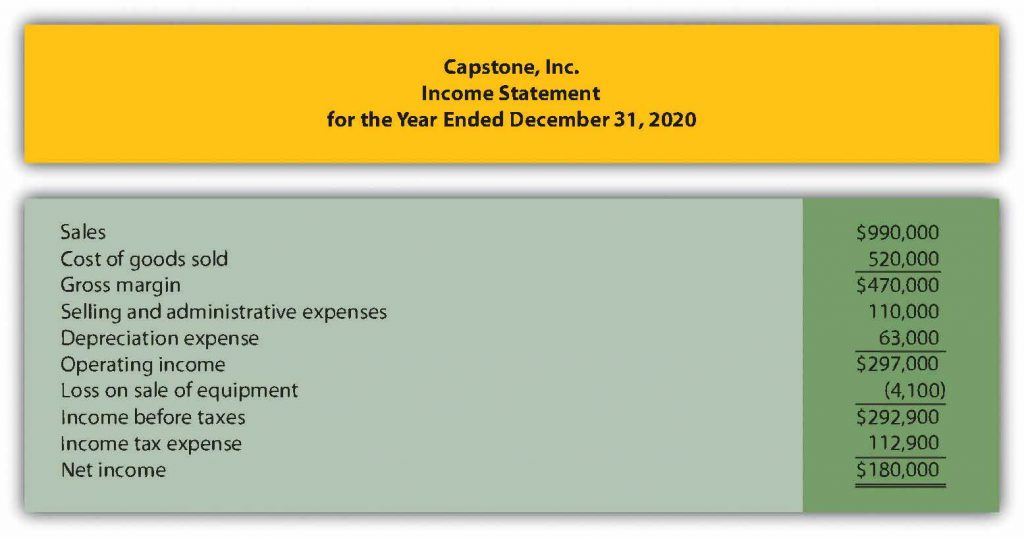

24. Operating Activities Section Using the Indirect Method. The following income statement and current sections of the balance sheet are for Capstone, Inc.

Required:

- Using the indirect method, prepare the operating activities section of the statement of cash flows for Capstone, Inc., for the year ended December 31, 2020. Use the format presented in Figure 6.4 “Operating Activities Section of Statement of Cash Flows (Home Store, Inc.)”.

- How much cash was provided by (used by) operating activities? Briefly describe what this amount tells us about the company.

-

-

-

Investing Activities Section. The following information is from the noncurrent asset portion of Caldera, Inc.’s balance sheet.

The following activities occurred during 2020:

- Sold equipment with a book value of $46,000 (= $170,000 cost − $124,000 accumulated depreciation) for $37,000 cash and depreciation expense for the year totaled $159,000

- Purchased equipment for $310,000 cash

- No additional loans to other entities were made during the year (Hint: Solve for the principal amount on loans collected during the year.)

- Sold long-term investments with an original cost of $27,000 for $33,000 cash

Required:

- Prepare the investing activities section of the statement of cash flows for Caldera, Inc., for the year ended December 31, 2020. Use the format presented in Figure 6.5 “Investing Activities Section of Statement of Cash Flows (Home Store, Inc.)”.

- How much cash was provided by (used by) investing activities? Briefly describe what this amount tells us about the company.

-

Financing Activities Section. The following information is from the noncurrent liabilities and owners’ equity portions of Flash, Inc.’s balance sheet.

The following activities occurred during 2020:

- Paid principal amount of $20,000 for long-term notes payable

- Received $110,000 for long-term notes payable

- Paid principal amount on bonds totaling $33,000

- Repurchased common stock for $60,000 cash

- Earned net income totaling $200,000

- Paid cash dividends totaling $40,000

Required:

- Prepare the financing activities section of the statement of cash flows for Flash, Inc., for the year ended December 31, 2020. Use the format presented in Figure 6.6 “Financing Activities Section of Statement of Cash Flows (Home Store, Inc.)”.

- How much cash was provided by (used by) financing activities? Briefly describe what this amount tells us about the company.

-

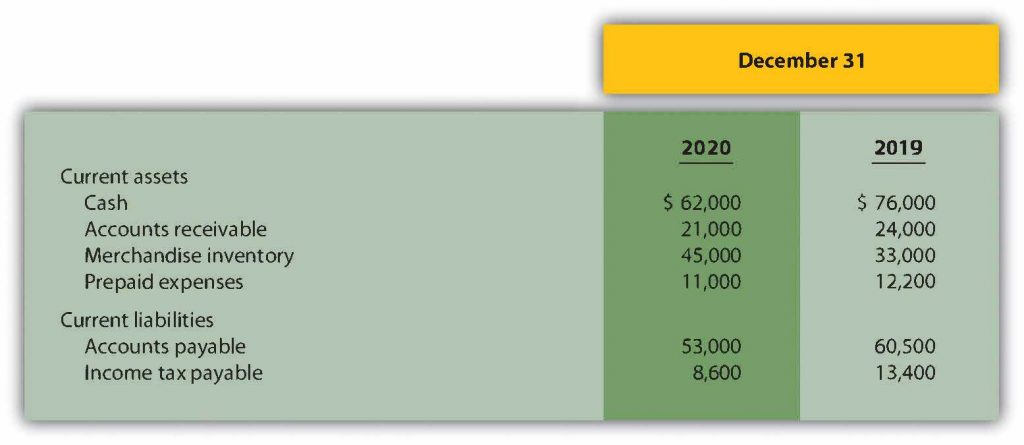

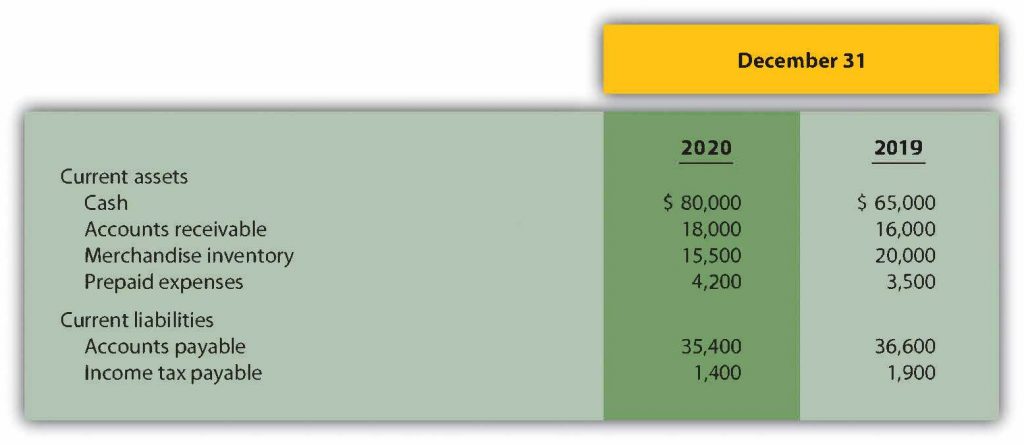

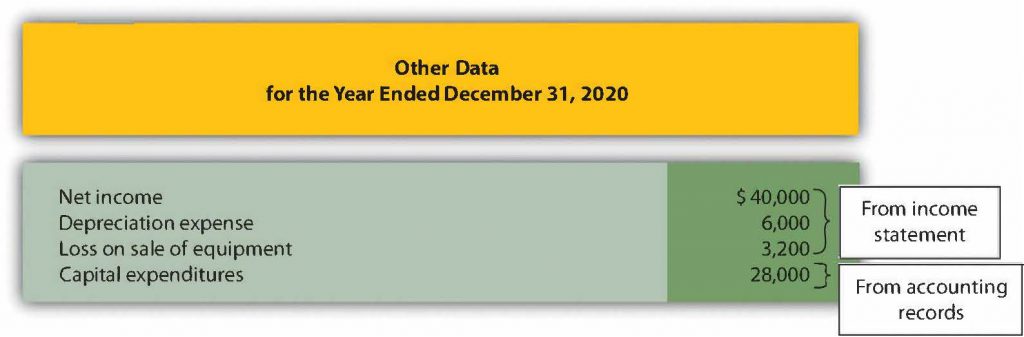

Operating Activities Section Using the Indirect Method and Cash Ratios. The following data are for Cycle Company.

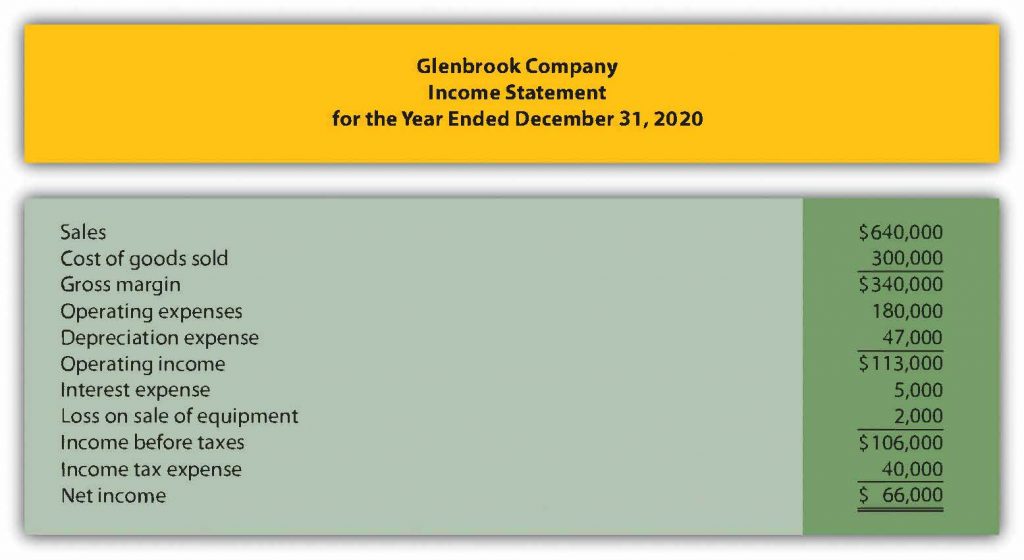

Required: