4.2: Tech and Timing- Creating Killer Assets

- Page ID

- 4522

Learning Objectives

After studying this section you should be able to do the following:

- Understand how many firms have confused brand and advertising, why branding is particularly important for online firms, and the factors behind Netflix’s exceptional brand strength.

- Understand the long tail concept, and how it relates to Netflix’s ability to offer the customer a huge (the industry’s largest) selection of movies.

- Know what collaborative filtering is, how Netflix uses collaborative filtering software to match movie titles with the customer’s taste, and in what ways this software helps Netflix garner sustainable competitive advantage.

- List and discuss the several technologies Netflix uses in its operations to reduce costs and deliver customer satisfaction and enhance brand value.

- Understand the role that scale economies play in Netflix’s strategies, and how these scale economies pose an entry barrier to potential competitors.

- Understand the role that market entry timing has played in the firm’s success.

To understand Netflix’s strengths, it’s important to view the firm as its customers see it. And for the most part, what they see they like—a lot! Netflix customers are rabidly loyal and rave about the service. The firm repeatedly ranks at the top of customer satisfaction surveys. Ratings agency ForeSee has named Netflix the number one e-commerce site in terms of customer satisfaction nine times in a row (placing it ahead of Apple and Amazon, among others). Netflix has also been cited as the best at satisfying customers by Nielsen and Fast Company, and was also named the Retail Innovator of the Year by the National Retail Federation.

Building a great brand, especially one online, starts with offering exceptional value to the customer. Don’t confuse branding with advertising. During the dot-com era, firms thought brands could be built through Super Bowl ads and expensive television promotion. Advertising can build awareness, but brands are built through customer experience. This is a particularly important lesson for online firms. Have a bad experience at a burger joint and you might avoid that location but try another of the firm’s outlets a few blocks away. Have a bad experience online and you’re turned off by the firm’s one and only virtual storefront. If you click over to an online rival, the offending firm may have lost you forever. But if a firm can get you to stay through quality experience, switching costs and data-driven value might keep you there for a long, long time, even when new entrants try to court you away.

If brand is built through customer experience, consider what this means for the Netflix subscriber. They expect the firm to offer a huge selection, to be able to find what they want, for it to arrive on time, for all of this to occur with no-brainer ease of use and convenience, and at a fair price. Technology drives all of these capabilities, so tech is at the very center of the firm’s brand building efforts. Let’s look at how the firm does it.

Selection: The Long Tail in Action

Customers have flocked to Netflix in part because of the firm’s staggering selection. A traditional video store (and Blockbuster had some 7,800 of them) stocks roughly three thousand DVD titles on its shelves. For comparison, Netflix is able to offer its customers a selection of over one hundred thousand DVD titles, and rising! At traditional brick-and-mortar retailers, shelf space is the biggest constraint limiting a firm’s ability to offer customers what they want when they want it. Just which films, documentaries, concerts, cartoons, TV shows, and other fare make it inside the four walls of a Blockbuster store is dictated by what the average consumer is most likely to be interested in. To put it simply, Blockbuster stocks blockbusters.

Finding the right product mix and store size can be tricky. Offer too many titles in a bigger storefront and there may not be enough paying customers to justify stocking less popular titles (remember, it’s not just the cost of the DVD—firms also pay for the real estate of a larger store, the workers, the energy to power the facility, etc.). You get the picture—there’s a breakeven point that is arrived at by considering the geographic constraint of the number of customers that can reach a location, factored in with store size, store inventory, the payback from that inventory, and the cost to own and operate the store. Anyone who has visited a video store only to find a title out of stock has run up against the limits of the physical store model.

But many online businesses are able to run around these limits of geography and shelf space. Internet firms that ship products can get away with having just a few highly automated warehouses, each stocking just about all the products in a particular category. And for firms that distribute products digitally (think songs on iTunes), the efficiencies are even greater because there’s no warehouse or physical product at all (more on that later).

Offer a nearly limitless selection and something interesting happens: there’s actually more money to be made selling the obscure stuff than the hits. Music service Rhapsody makes more from songs outside of the top ten thousand than it does from songs ranked above ten thousand. At Amazon.com, roughly 60 percent of books sold are titles that aren’t available in even the biggest Borders or Barnes & Noble Superstores (Anderson, 2004). And at Netflix, roughly 75 percent of DVD titles shipped are from back-catalog titles, not new releases (at Blockbuster outlets the equation is nearly flipped, with some 70 percent of business coming from new releases) (McCarthy, 2009). Consider that Netflix sends out forty-five thousand different titles each day. That’s fifteen times the selection available at your average video store! Each quarter, roughly 95 percent of titles are viewed—that means that every few weeks Netflix is able to find a customer for nearly every DVD title that has ever been commercially released.

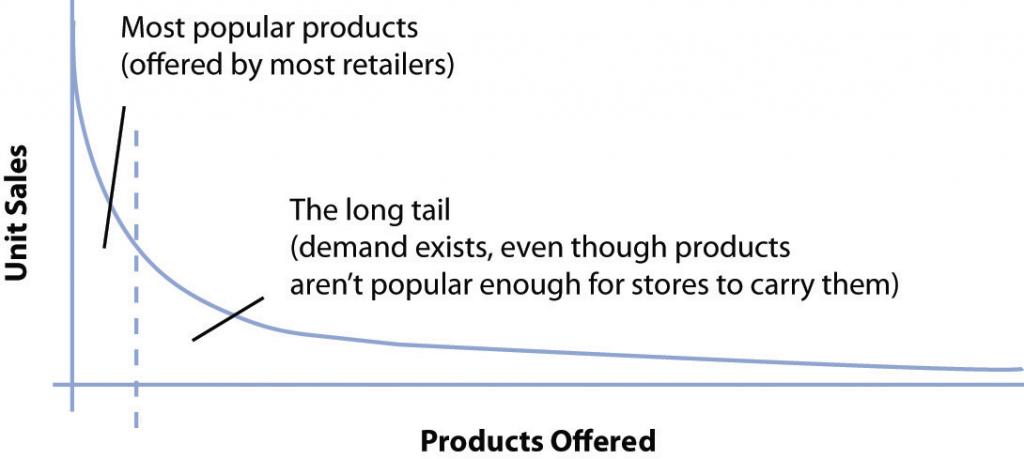

This phenomenon whereby firms can make money by selling a near-limitless selection of less-popular products is known as the long tail. The term was coined by Chris Anderson, an editor at Wired magazine, who also wrote a best-selling business book by the same name. The “tail” (see Figure 4.2 “The Long Tail”) refers to the demand for less popular items that aren’t offered by traditional brick-and-mortar shops. While most stores make money from the area under the curve from the vertical axis to the dotted line, long tail firms can also sell the less popular stuff. Each item under the right part of the curve may experience less demand than the most popular products, but someone somewhere likely wants it. And as demonstrated from the examples above, the total demand for the obscure stuff is often much larger than what can be profitably sold through traditional stores alone. While some debate the size of the tail (e.g., whether obscure titles collectively are more profitable for most firms), two facts are critical to keep above this debate: (1) selection attracts customers, and (2) the Internet allows large-selection inventory efficiencies that offline firms can’t match.

Figure 4.2 The Long Tail

The long tail works because the cost of production and distribution drop to a point where it becomes economically viable to offer a huge selection. For Netflix, the cost to stock and ship an obscure foreign film is the same as sending out the latest Will Smith blockbuster. The long tail gives the firm a selection advantage (or one based on scale) that traditional stores simply cannot match.

For more evidence that there is demand for the obscure stuff, consider Bollywood cinema—a term referring to films produced in India. When ranked by the number of movies produced each year, Bollywood is actually bigger than Hollywood, but in terms of U.S. demand, even the top-grossing Hindi film might open in only one or two American theaters, and few video stores carry many Bollywood DVDs. Again, we see the limits that geography and shelf space impose on traditional stores. As Anderson puts it, when it comes to traditional methods of distribution, “an audience too thinly spread is the same as no audience at all (Anderson, 2004).” While there are roughly 1.7 million South Asians living in the United States, Bollywood fans are geographically disbursed, making it difficult to offer content at a physical storefront. Fans of foreign films would often find the biggest selection at an ethnic grocery store, but even then, that wouldn’t be much. Enter Netflix. The firm has found the U.S. fans of South Asian cinema, sending out roughly one hundred thousand Bollywood DVDs a month. As geographic constraints go away, untapped markets open up!

The power of Netflix can revive even well-regarded work by some of Hollywood’s biggest names. In between The Godfather and The Godfather Part II, director Francis Ford Coppola made The Conversation, a film starring Gene Hackman that, in 1975, was nominated for a Best Picture Academy Award. Coppola has called The Conversation the finest film he has ever made (Leonhardt, 2006), but it was headed for obscurity as the ever-growing pipeline of new releases pushed the film off of video store shelves. Netflix was happy to pick up The Conversation and put it in the long tail. Since then, the number of customers viewing the film has tripled, and on Netflix, this once underappreciated gem became the thirteenth most watched film from its time period.

For evidence on Netflix’s power to make lucrative markets from nonblockbusters, visit the firm’s “Top 100 page.”1 You’ll see a list loaded with films that were notable for their lack of box office success. As of this writing the number one rank had been held for over five years in a row, not by a first-run mega-hit, but by the independent film Crash (an Oscar winner, but box office weakling) (Elder, 2009).

Netflix has used the long tail to its advantage, crafting a business model that creates close ties with film studios. In most cases, studios earn a percentage of the subscription revenue for every disk sent out to a Netflix customer. In exchange, Netflix gets DVDs at a very low cost. The movie business is characterized by large fixed costs up front. Studio marketing budgets are concentrated on films when they first appear in theaters, and when they’re first offered on DVD. After that, studios are done promoting a film, focusing instead on their most current titles. But Netflix is able to find an audience for a film without the studios spending a dime on additional marketing. Since so many of the titles viewed on Netflix are in the long tail, revenue sharing is all gravy for the studios—additional income they would otherwise be unlikely to get. It’s a win-win for both ends of the supply chain. These supplier partnerships grant Netflix a sort of soft bargaining power that’s distinctly opposite the strong-arm price bullying that giants like Wal-Mart are often accused of.

The VCR, the Real “Killer App”?

Netflix’s coziness with movie studios is particularly noteworthy, given that the film industry has often viewed new technologies with a suspicion bordering on paranoia. In one of the most notorious incidents, Jack Valenti, the former head of the Motion Picture Association of American (MPAA) once lobbied the U.S. Congress to limit the sale of home video recorders, claiming, “the VCR is to the American film producer and the American public as the Boston strangler is to the woman home alone” (Bates, 2007).

Not only was the statement over the top, Jack couldn’t have been more wrong. Revenue from the sale of VCR tapes would eventually surpass the take from theater box offices, and today, home video brings in about two times box office earnings.