14.2: Selling Short

- Page ID

- 79802

Okay, Fun Seekers, have we got a strategy for you! You say you believe a stock, or any security, for that matter, is overvalued and the price is bound to fall? Well, you can sell that stock short, also called shorting the stock, and if the price goes down, you will make money. Of course, if the price goes up, you will lose money. In fact, if the price goes up, you can lose a whole lot o’ money very quickly. Selling short is much more dangerous than buying on margin. And you know how we feel about buying on margin, right?

Don’t miss the article at the end of our discussion of selling short. We don’t want you to wind up like that poor slob. (If you want to see what happened to him before you understand how to sell short, please see the sad story here.)

Long Purchases

A long purchase is a transaction in which investors buy securities in the hope that they will increase in value and can be sold at a later date for profit. Long purchases go by various names such as “buying long,” “going long,” “long position,” or simply just, “long.” Long purchases are the type of transaction that people commonly think of when they hear that someone bought stock. They are the transactions that we have been discussing since the beginning of our journey together. Buying long is the most common form of transaction. Investors have the expectation of dividends or capital appreciation or both. “Buy low, sell high.”

Here is an example: You purchase one share of common stock for $20. The market price rises to $30. Congratulations! You made $10 on a $20 investment! That is a 50% increase. Of course, if the price dropped to $10, you lost $10, or one half of your investment, a 50% decrease.

But what if we told you that buying long was not the only way to make money with stocks? That there was another method other than, “Buy low, sell high?” Oh, boy, you’re gonna’ love this!

Short Sales

Participants in the stock marketplace can engage in short selling. Short selling also goes by various names such as “selling short,” “shorting the stock,” “going short,” or again, simply just “short.” Short selling is the sale of borrowed securities, their eventual repurchase by the short seller, and their return to the lender. It is the opposite of “buying long.” You are hoping that the price goes down. You have reversed the process. You want to, “Sell high, buy low.” Selling short must take place in a margin account since you are borrowing the stock you sell from the brokerage firm. However, with short selling, you are borrowing stock instead of cash.

“Wait a minute!” you exclaim. “That doesn’t sound legal! How can you sell something that isn’t yours?” This is the first reaction that many individuals experience. Although from time to time, some call for short selling to be banned, it’s perfectly legal. The first short sales took place hundreds of years ago and it doesn’t appear that the practice will be barred any time soon.

Here is how selling short works: You borrow the stock from another shareholder without their knowledge and sell it on the market. You receive money for selling stock that you do not own. You wait for the stock price to go down. You then buy back the shares at a lower price, pocketing the difference. The shareholder you borrowed the shares from never knows that the shares were borrowed. The brokerage firm does all the financial sleight-of-hand. Oh, by the way, you must pay any dividends the company declares to the investor who you borrowed the shares from. Why? The company is now paying the dividends to whomever bought the shares you sold short.

The graphic above details the process. Today, you initiate a short sale. You believe that a company’s share price will decline. You borrow shares from another investor at your brokerage firm. Again, that investor never knows that the shares were borrowed; your brokerage firm takes care of all the accounting. You then sell those shares in the open market. You are now “short.” Eventually, some day in the future, you will need to buy back those shares and return them to the investor that you borrowed them from. If the price goes down, you have made money. If the price goes up, you have lost money. It is the opposite of buying long. Oh, by the way, if the investor wants to sell their shares and the brokerage firm doesn’t have any other shares available to borrow, the brokerage firm can close out your transaction without your consent. This does not happen very often but it can happen.

The Rationale for Selling Short

If you find yourself in a conversation with an economist or a market professional, they will often defend selling short as an efficient method to “root out hype and irrational exuberance” or “keep prices in line with reality.” It’s all hogwash! Selling short is dangerous speculation. As with all the previous speculations we have been exploring, you can make a lot of money quickly but you can also lose a whole lot more money quickly, sometimes instantly. It is also anathema to capitalism. (Anathema is a fancy word for hateful or offensive.) As we have learned, as the global economy has expanded over the last two centuries, stock prices have risen along with it. We want the global economy to expand and for companies to do well so that we citizens of the world will enjoy a better standard of living and everyone will have their basic needs met, food, clothing, and shelter … and Internet access. When you sell short, you are betting against this future. You want a company to do poorly. Yes, we know that some companies will fail. That is part of capitalism. However, we as a society should be rooting for all individuals and companies to prosper.

In short (ah, pun intended), if you really want to know why certain speculators and traders short stocks, you will need to discuss the topic in earnest with them. Yours Truly is one of those fanatical outliers who believe that short selling should simply be banned, once and for all. (Don’t worry. We fanatics won’t get our way. Short selling is not going anywhere anytime soon. Okay, end of rant. Let’s get on with the mechanics of selling short.)

The Aspects and Mechanics of Selling Short

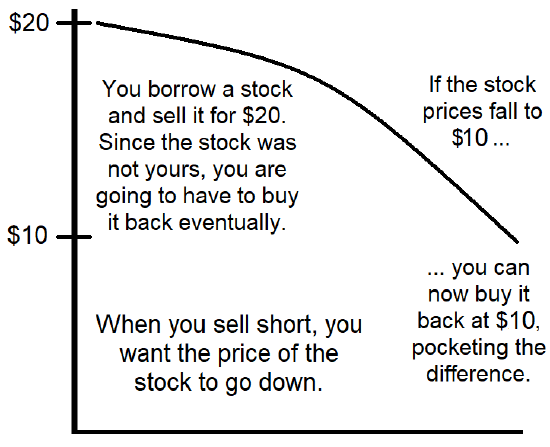

Let’s take a look at an example which is the opposite of the buying long example above. You sell a stock short for $20. You receive $20 from the sale of the stock even though the stock was not yours. You borrowed it from someone else. The stock price goes down to $10. You buy back the stock at $10, “closing out the transaction.” You give the stock back to the person you borrowed it from. You get to keep the $10 difference. Congratulations! You just made $10 on a $0 investment! Well, not quite.

You cannot actually make $10 on a $0 investment. It is a margin account, remember? You borrowed the stock that you sold. The rules for a margin account still apply. You must deposit at least 50%. “50% of what?!” you ask confusedly. 50% of what you borrowed! “Huh? What?” You must deposit 50% of the proceeds from the sale of the borrowed stock. You borrowed the stock that you sold. Again, the brokerage firms use the Account Balance Sheet to keep track of the investor’s margin. We will revisit the Account Balance Sheet shortly. But first, let’s see what happens if the price rises instead of falls.

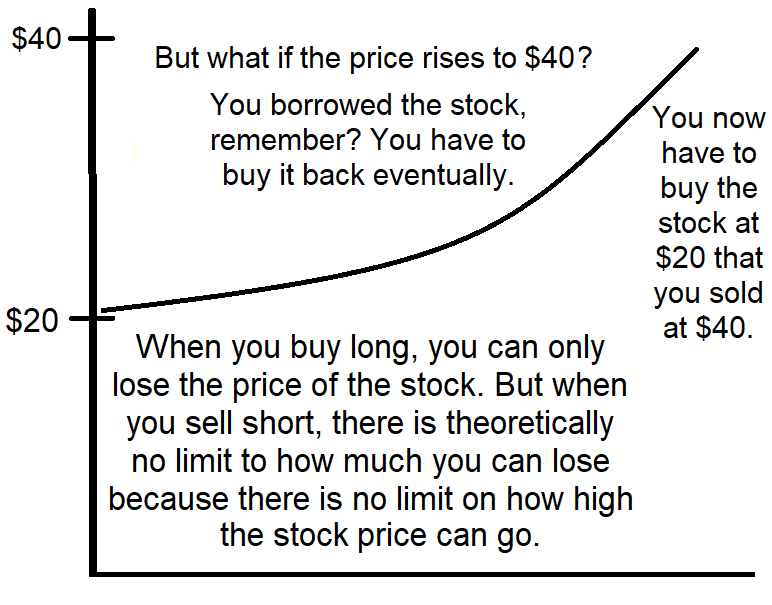

Again, you sell a stock short for $20. You receive $20 from the sale of the stock even though the stock was not yours. You borrowed it from someone else. This time, the stock price goes up to $40. You buy back the stock at $40. Remember, you borrowed the shares. You must replace them at some future date. You must buy the shares back. Uh-oh! You just lost $20 on your short transaction!

When you buy long, you can only lose the purchase price of the stock. If you buy a stock for $20 and it goes to zero, you lose $20. But once a stock reaches $0, it cannot go any lower. However, when you sell short, there is no limit to the amount of money you can lose theoretically. Why? Because there is no limit to the price of a stock. The price can always go higher. The playful Wall Street saying for this situation is, “He who sells what isn’t his’n, must buy it back or go to prison.” Of course, since you sell short in a margin account, your account is still being watched carefully for signs of trouble and if the price rises enough, you will get a margin call. Remember, if you don’t make good on the transaction, the brokerage firm is left holding the bag. And they don’t want that scenario to take place!

The Account Balance Sheet, Revisited

Let’s see how the Account Balance Sheet works with short sales. The previous formula for margin now becomes:

Account Margin = Account Equity / Short Position

In this example, we short 100 shares of a stock priced at $100. We receive $10,000 from the proceeds from the sale of the shares. We must deposit $5,000, 50% of the $10,000 proceeds.

| Assets | Liabilities and Equity | ||

| 100 Shares @ $100/shr | $10,000 | Short Position | $10,000 |

| Initial Margin Deposit | $5,000 | Account Equity | $5,000 |

| Total Assets: | $15,000 | Total Liabilities and Equity: | $15,000 |

Our initial margin is 50%. The account equity of $5,000 divided by the short position of $10,000. Now what happens if the stock price falls to $80. The Account Balance Sheet becomes:

| Assets | Liabilities and Equity | ||

| 100 Shares @ $100/shr | $10,000 | Short Position | $8,000 |

| Initial Margin Deposit | $5,000 | Account Equity | $7,000 |

| Total Assets: | $15,000 | Total Liabilities and Equity: | $15,000 |

The short position fell and the account equity rose. You made money because the stock price fell. So far, you have made $2,000 on the transaction with an initial outlay of only $5,000. Well done! But what if the stock price rose to $120. The situation is very different.

| Assets | Liabilities and Equity | ||

| 100 Shares @ $100/shr | $10,000 | Short Position | $12,000 |

| Initial Margin Deposit | $5,000 | Account Equity | $3,000 |

| Total Assets: | $15,000 | Total Liabilities and Equity: | $15,000 |

The short position, the value of the shares, has risen to $12,000 and the account equity has fallen to $3,000. The account margin formula is now:

Account Margin = Account Equity / Short Position = $3,000 / $12,000 = 25%

Uh, oh! Your brokerage’s maintenance margin is 35%. You have another margin call! Notice how the stock only had to rise 20% for you to get the margin call. Selling short is very risky. The brokerage firm will keep a close eye on you and may buy back the shares without even consulting you. (Isn’t it time you decided to close your margin account and open a cash account?)

Short Squeeze, Short Interest, and Shorting Against the Box

When a stock or the market as a whole is going down, momentum speculators often short stocks to try to take advantage of the downward momentum. This pushes the stock or the market down even further but eventually, the short shares must be repurchased. The subsequent up movement of the market is often dramatic as short sellers cover their positions. This is called a short squeeze. It is the reason that we often see powerful upswings in stocks and the market as a whole after a stomach-churning downturn. When there is a strong downturn, friends and family members will often ask me, “Aren’t you worried? Shouldn’t we sell?” I always respond, “Nah. Just wait a few days.” When the market responds, they invariably ask me, “How did you know that was going to happen?” I answer, “First, I didn’t know. I was just playing the odds. But it is very typical. It’s called a short squeeze. It is especially typical if there is a tremendous amount of short interest.”

Short interest is the amount of stock shares that have been sold short. The more short interest, the more shares that will need to be purchased in the future to cover the short positions. It is similar to a spring being pushed downward and then released. In August of 2002, short interest was the highest it had ever been in the history of the United States stock markets. That gave Your Humble Author great comfort because it signaled that the long market downturn that started in March of 2000 was close to an end. The market bottom was October of 2002.

Actually, there used to be a valid reason for shorting a stock. It was called, “shorting against the box.” Yes, it’s a dumb name but it had a valid purpose. You shorted a stock that you already owned. This allowed you to essentially sell the stock without creating a taxable transaction until you closed out the transaction with your own stock. For example, you could sell the stock short in December, receive the money and then deliver your shares in January, effectively postponing the taxes for another year. The IRS removed this loophole in 1997. Oh, well.

Final Thoughts Regarding Selling Short

NEVER SHORT A STOCK!

Do you happen to remember the quote attributed to Sir John Maynard Keynes? "The market can stay irrational longer than you can stay solvent." He was responding to market professionals who believed that stocks were overpriced. These market professionals were shorting stocks based on that belief. They were eventually proven correct. The market eventually experienced a sharp downturn. However, before that happened, stocks continued to rise. And the short sellers lost tremendous sums of money in the process. They were absolutely right but as Sir Keynes so astutely observed, "The market can stay irrational longer than you can stay solvent." My advice? Never short a stock!

But you don’t have to take my word for it. Take it from Peter Lynch, who racked up 29% per year as the mutual fund manager of the Fidelity Magellan fund over 13 years. Peter Lynch says, “Never short a stock!” And if that doesn’t convince you, take a look at this poor, unfortunate soul who woke up one morning and found that his $37,000 margin account now had a negative balance of over $106,000. Yes, you read that correctly. He wound up owing his brokerage firm $106,000, and unless he declares bankruptcy or flees the country, he will be required to repay the amount. (Aye, what is he going to tell his wife? “Honey, we have a small problem.”) Dear Students, never short a stock!