11.2: Asset Allocation

- Page ID

- 79793

Video - Audio - YouTube (Material for this section starts on slide 17.)

Asset Allocation is a fancy term for a simple series of questions that all investors should ask themselves or review with their financial advisor. “How much should I have in stocks? How much in bonds? How much of each stock & bond type?” Many advisors suggest a formula such as subtract your age from 100 (or maybe now 110 or 120). That is the percentage of stocks you should own and the rest should be in bonds. For example, a 40-year-old would have 100-40 or 60% invested in stocks and 40% in bonds. “Poppycock!” say others. Buy high-quality stocks and put up with the risk. Once you near retirement, start buying bonds. (Why does that number seem to be rising from 100 to 110 or 120? We are living longer! More about investing in retirement later.)

This example asset allocation is for someone who is comfortable with a significant percentage of stock investments. It does have some bonds, though, to add some stability. Notice that there is only a bit of “spice” in the form of aggressive growth and small company stocks. Do you like it? It is yours! But remember that everyone's situation and risk tolerance are different. This allocation might be too aggressive for some and too conservative for others.

Rebalancing

Another very popular diversification strategy is the technique of rebalancing. Let’s say you start off with the popular 60% stocks, 40% bonds portfolio. Every year, check to see if your percentages are still in balance. If stocks have had a banner year, you might now be at 70% stocks, 30% bonds instead of your original target of a 60%/40% allocation. You would sell enough stocks and buy enough bonds to bring the balance back to your target 60%/40% allocation. Likewise, if stocks have tanked, you would sell enough bonds and buy enough stocks to bring the percentage back up to 60%/40%. This strategy forces us to, “Do the right thing.” It forces us to, “Buy Low, Sell High.” Think about it. If stocks are rising, who wants to sell? Similarly, if stocks have tanked, who wants to buy? This strategy helps us to remove some of the influence our emotions have on our investing.

Recall the strategy of one of the balanced mutual funds that we discussed: The fund will never be more than 75% stocks, 25% bonds, and never less than 50% stocks, 50% bonds. This strategy forces the balanced mutual fund to stay balanced.

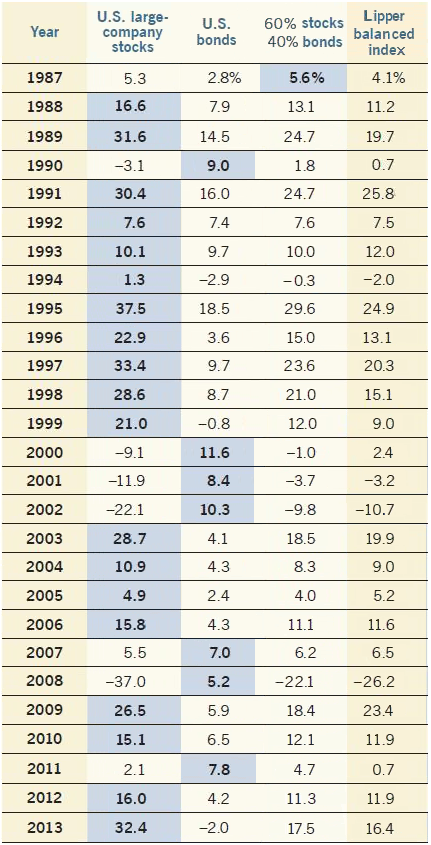

A Stock Portfolio Versus a Bond Portfolio Versus a Balanced Portfolio

The table below compares a 100% stock portfolio versus a 100% bond portfolio versus a balanced portfolio.

Source: The Capital Group

Having a balanced portfolio means that you almost never have the best returns in any one year. However, it also means you will very rarely ever have the worst returns in any one year, either. In addition, although it is very unlikely that you will not equal or surpass an all-stock portfolio, you should do much better than an all-bond portfolio. But you already know what we are going to add, right? There are no guarantees!

Stocks and Bonds in Retirement

Throughout our journey together, we have been discussing the accumulation phase of investing. In retirement, we move into the distribution phase. To that end, many advisors suggest that retirees shed the bulk of their stock investments in favor of bonds and cash investments in order to protect against market downturns. The only problem is people are living much, much longer today. A 65-year-old couple has a 45 percent chance that one of them will survive to age 90. As you near retirement, start migrating your investments from stocks to bonds but don’t abandon stocks entirely. Retirees still need some growth in their portfolio even as they are in the distribution phase of their investing career. In the chapter 11 section of the class website, there is a presentation that compares bonds in retirement, stocks in retirement, and then two versions of a balanced portfolio. Both versions of the balanced portfolio were able to generate much stronger returns than the bond portfolio while damping down the volatility that accompanied the stock portfolio.