10.2: Convertible Securities

- Page ID

- 79790

Video - Audio - YouTube (Material for this section starts on slide 9.)

Convertible Securities are fixed-income obligations that can be converted into a specified number of shares of the issuing company’s common stock. There are both convertible bonds and convertible preferred stock. Convertible securities are often referred to as Deferred Equity because the convertible securities could become part of the company’s pool of common stock in the future. Because of this ability to share in the possible appreciation of common stock, convertible securities are also sometimes referred to as an “Equity Kicker.”

Example: A single $1,000 bond can be converted into 20 shares of common stock

One of the major disadvantages of both bonds and preferred stock is that if the company is wildly successful, the bonds and preferred stock do not participate in the success. The ability to convert their convertible security into common stock allows the investor to partake in the potential success of the company. Oh, by the way, once you convert from the convertible bond or convertible preferred stock to the common stock, you can’t convert back.

Conversion Measures

There are several measures and conditions of the conversion feature of convertible securities, some are fixed and others depend upon the current price of the company’s common stock. The Conversion Period is the time period during which a convertible issue can be converted. The ability to convert a convertible bond or convertible preferred stock is normally deferred for a period of years. This is not usually a serious problem since when the convertible security is issued, a conversion is not normally advantageous to the investor. The common stock price normally will have to rise substantially before an investor would want to convert the security.

The Conversion Ratio is the number of shares of common stock into which a convertible security can be converted and is fixed. In the example above, an investor might receive 20 shares of common stock for each convertible bond. Hence, the Conversion Price is the price per share at which common stock will be delivered to the investor. The formula is:

Par Value $1,000

Conversion Price = ────────────────── = ───────── = $50 Conversion Price

Conversion Ratio 20

The Conversion Value is an indication of what a convertible issue would trade for if it were priced to sell on the basis of the price of the corresponding common stock.

Conversion Value = Conversion Ratio * Market Price of Common Stock

In the example above, if the market price of the common stock were $60, the formula would be:

Conversion Value = 20 * $60 = $1,200 Conversion Value

Assuming the conversion period has begun, we would expect the $1,000 convertible bond to be selling for at least $1,200 since an investor can instantly convert the bond into 20 common stock shares worth $1,200. However, the convertible bond would probably sell for more than $1,200 because of its ability to convert to the common stock plus the fact that it is a bond and is generating interest every six months. This extra amount is called the Conversion Premium. It is the amount by which the market price of a convertible security exceeds its conversion value.

Conversion Premium = Market Price of Common Stock - Conversion Value

Let’s continue the above example. Assume we have a $1,000 bond with conversion ratio of 20 and the common stock shares are trading at $60.00. As computed above, the conversion value is $1,200, 20 shares * $60 market price of the common stock. Let’s also assume that the bond is currently selling for $1,400. Therefore, the conversion premium formula would be:

Conversion Premium = $1,400 - $1,200 = $200 Conversion Premium

The bond is selling for $200 above the conversion value. The Conversion Parity is the price at which the common stock would have to sell in order to make the convertible security worth its present price. It is also called the Conversion Equivalent. The formula is:

Market Price of Bond $1,400

Conversion Parity = ────────────────────── = ──────── = $70 Conversion Parity

Conversion Ratio 20

We would expect the market price of common stock to be close to $70. However, the price would most likely be less than $70 because of the convertible security’s conversion premium.

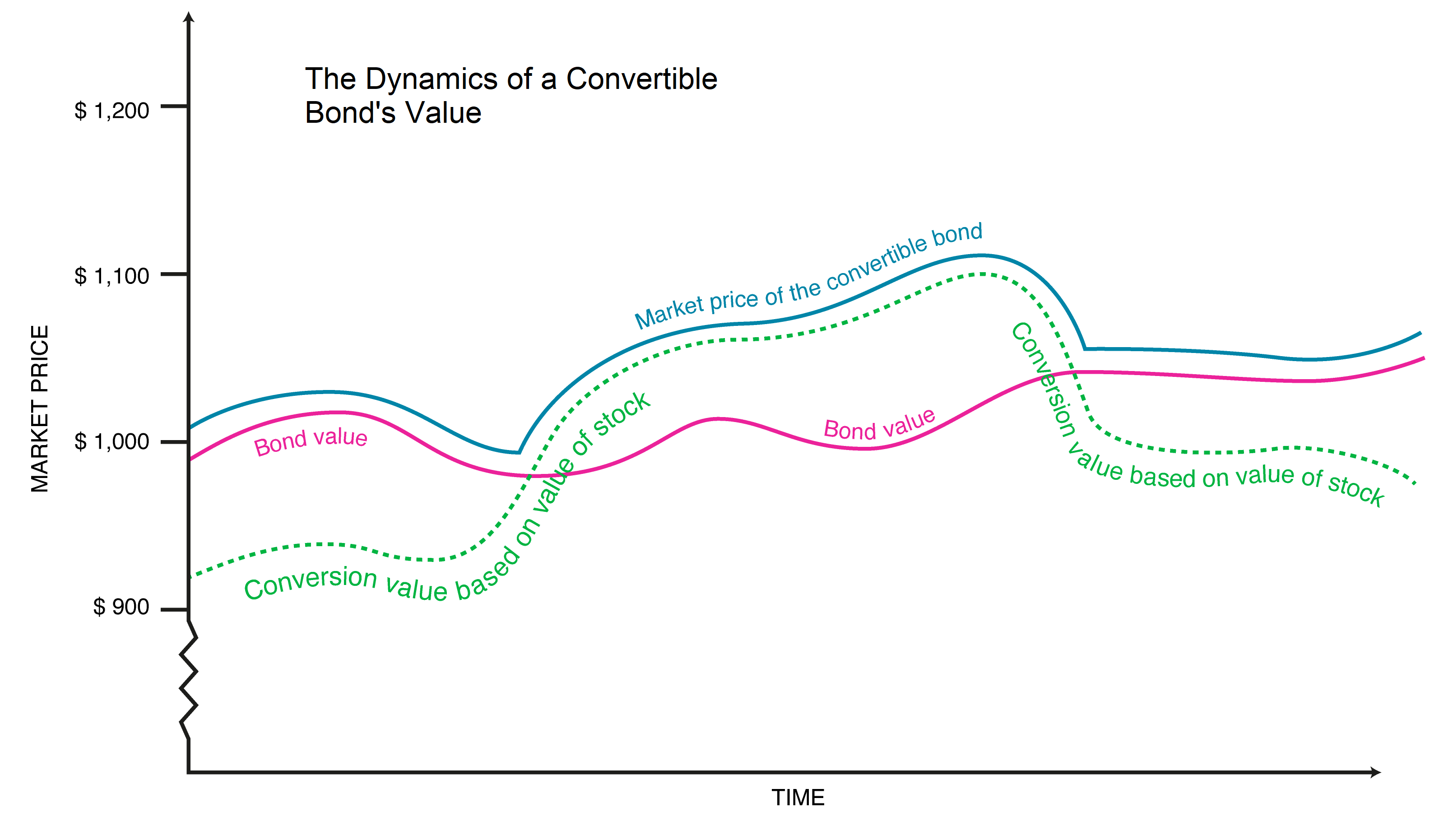

Graphic courtesy of Ferran Capo: StudioCapo

The graphic above shows that the value of a convertible bond depends upon both the underlying common stock price and the value of the interest payments and principal repayment that the bond generates. If the underlying common stock price creates a conversion value above and beyond the value of the bond from interest payments and the principal repayment, the bond will sell for more than the value of the bond from just being a bond. However, if the underlying common stock price falls below the value of the bond from just being a bond, the price of the convertible bond will be propped up since the bond is still generating interest payments and the principal repayment.

What’s the bottom line on convertible securities? Convertible securities allow you to partake in the potential capital appreciation of the common stock with less risk because of the income from the convertible bond or convertible preferred stock. If the stock price is below the conversion price, then the convertible security’s price will be kept up because of its value from being an income producing investment. However, you pay for the reduced risk via the conversion premium. Again, our personal opinion is that we believe individual retail investors are best served by focusing their attention on common stocks for growth and income and bonds for income but there are always exceptions.