9.1: Bond Yields

- Page ID

- 79786

Bond yield is one of the most important factors in bond valuation. What income is the bond paying? Over the long sweep of time, income is the principal reward an investor receives from investing in bonds. Although there are sometimes opportunities for capital gains, when the bond is redeemed, you are only going to get back the par value of the bond. Given that most all bond issuers repay their principal without incident, the valuations calculated using bond yields tend to be very predictable.

The unpredictable factor in bond valuation is the future direction of interest rates. However, for the many investors who hold onto their bonds until maturity when they get their principal back, the direction of interest rates is unimportant to them. They are mostly interested in the income and are not affected by the direction of interest rates since they have no intention of ever selling their bonds before they mature. You are only concerned about changing interest rates if you intend or are forced to sell your bonds before they mature.

There are several different types of bond yields. We will cover the most important.

Nominal Yield, also called the Coupon Yield

The Nominal Yield is the named interest rate of the bond. It also is called the Coupon Yield, the Nominal Rate, and the Coupon Rate. Recall that the term coupon came from the historical aspect of certain bonds that had coupons attached to the bond document. When the interest was due, the investor would clip the coupon and send the coupon to the bond issuer who would then send the bond investor a check. So to this day, “clipping the coupon” is the phrase that you will hear bond investors say even though no bonds have had coupons attached to them for decades.

The absolute dollar amount of annual interest is calculated by multiplying the nominal yield by the par value. For our purposes, we will always use $1,000 as the par value of our bonds even though some bonds have par values of $5,000 or $10,000. For example, if a bond had a nominal yield of 8%, we would multiply $1,000 by 8%. That would give us $80 of annual interest. Recall that most bonds pay interest every six months so that would signify that we were going to receive $40 every six months from our bonds.

The Nominal Yield, however, is not as important as the Current Yield, Yield to Maturity, and the Yield to Call. Let’s learn how to calculate each.

Current Yield

The Current Yield is the amount of current income a bond provides relative to its market price. It is also called the Current Rate. The method for calculating the Current Yield is:

Annual Interest

Current Yield = ————————————————————————————————

Current Market Price of the Bond

For example, say we found a bond with a Nominal Yield of 8% that was selling for $800. This is a bond that is selling at a discount, most likely because interest rates have risen or possibly because the bond issuer is in distress and investors are worried about the possibility of default on the interest and principal payments.

Annual Interest $80

Current Yield = ———————————————————————————————— = ——————— = 0.10 or 10%

Current Market Price of the Bond $800

The nominal yield is 8% but because the bond is selling at a discount, the current yield is actually 10%. We only have to pay $800 to get $80 of annual interest. What if the bond is selling at a premium because interest rates have fallen? Let’s say that the same 8% bond was selling for $1,200.

Annual Interest $80

Current Yield = ———————————————————————————————— = ———————— = 0.066667 or 6.67%

Current Market Price of the Bond $1,200

The nominal yield is the same 8% and the annual interest is the same $80, but because the bond is selling at a premium, the current yield is only 6.67%. We would have to pay a premium of $1,200 to get the $80 of annual interest.

Yield to Maturity

The Current Yield tells us what the bond is paying us at this moment. However, we must remember that when the bond matures, we will receive the par value, no matter what price we actually pay for the bond. Therefore, we need to look at the Yield to Maturity to know what the fully compounded rate of return that will be earned by an investor over the life of the bond. It is often abbreviated as YTM and is sometimes called the Promised Yield. The Yield to Maturity includes both the current income and the price appreciation or depreciation of the bond.

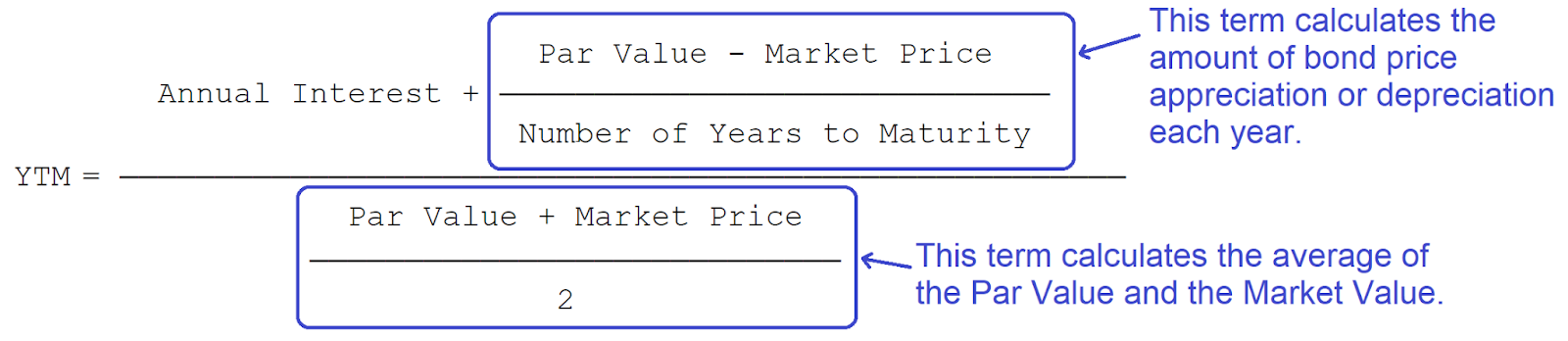

There are two primary methods of calculation. The more accurate method is the bond pricing formula that we will discuss later combined with an internal rate of return approximation. Although it is a more accurate method, it is difficult to do manually and is better left to a spreadsheet. The other more popular method is a formula that is much easier to use and gives a very good approximation to the more accurate method. The formula looks scary but is actually fairly easy to use. The Yield to Maturity approximation formula is:

Par Value - Market Price

Annual Interest + —————————————————————————————

Number of Years to Maturity

YTM = ——————————————————————————————————————————————————

Par Value + Market Price

——————————————————————————————

2

Relax. Let’s break it down into pieces. The first observation that we can make is that it is somewhat similar to the Current Yield formula. Annual Interest is on the left in the numerator just like the Current Yield formula. In the denominator, instead of just the Market Price as we had in the Current Yield formula, we take the average of the Par Value and Market Price. Why do we use the average? Because we bought the bond at the Market Price but we will receive the Par Value when the bond matures. As mentioned, the Yield to Maturity formula takes into account not only the interest we receive but also the par value, the principal amount that we will receive when the bond matures.

Okay, how about that scary part on the right side of the numerator? What is that for? Remember that although we might have paid a premium or a discount for the bond, when the bond matures, we will only receive the par value. We do not receive the market price that we paid for the bond. The calculation takes that into account. The Par Value minus the Market Price computes the difference between what we paid for the bond (Market Price) and what we will receive when the bond matures (Par Value). We then divide by the Number of Years to Maturity to determine how much per year the price of the bond will appreciate (if it is a discount bond) or depreciate (if it is a premium bond). Let’s take a look at an annotated version of the formula:

Let’s return to our first example of an 8% bond selling at a discount for $800 and now add that the bond will mature in 10 years. Remember that for our purposes, the Par Value will always be $1,000. The formula becomes

$1,000 - $800 $200

$80 + ————————————————— $80 + ————

10 10 $80 + $20 $100

YTM = ———————————————————————————— = ————————————— = ——————————— = ————— = 0.1111 or 11.11%

$1,000 + $800 $1,800 $900 $900

——————————————— ————————

2 2

In the denominator, the average of the $1,000 Par Value and the $800 Market Value is $900. In the numerator, we compute the difference between the $1,000 Par Value and the $800 Market Value and then divide by 10, the Number of Years to Maturity. The difference between $1,000 and $800 is $200. The bond will increase in value $200 from the Market Price of $800 to the Par Value of $1,000 when the bond matures. We then divide by the Number of Years to Maturity of 10 to get $20. Every year, theoretically, the price of the bond will increase by $20. (It doesn’t actually work that way in the marketplace since interest rates and bond prices are continuously changing due to market forces. However, this approximation serves our purpose.) Purchasing the bond at a discount means that we will receive more than the Current Yield of 10%. We will not only receive the interest payments but we will receive more than what we paid for the bond when it matures. If we hold the bond for 10 years, our Yield to Maturity will be approximately 11.1%.

The situation reverses if we buy a bond at a premium. The Yield to Maturity will be less than the Current Yield. Let’s return to the second example of an 8% bond selling at a premium of $1,200 and matures in 10 years. The formula is:

$1,000 - $1,200 -$200

$80 + ————————————————— $80 + —————

10 10 $80 + (-$20) $60

YTM = ———————————————————————————— = ————————————— = —————————————— = —————— = 0.054545 or 5.45%

$1,000 + $1,200 $2,200 $1,100 $1,100

————————————————— ————————

2 2

The Current Yield was 6.67% but because we are paying $1,200 for the bond and only receiving $1,000 when the bond matures in 10 years, our Yield to Maturity is only 5.45%. Each year, we subtract $20 from our Annual Interest as the price of the bond makes its way from the Market Price down to the Par Value.

Yield to Call

In the case of callable premium bonds, there is always the risk of the bond being called away from us. The Yield to Call calculates the yield on a bond assuming it will be called away from us on a specified date sometime in the future. This is only used on premium-priced bonds. A bond issuer would never call in discount bonds. That would mean they would be refinancing at a higher rate. As with the Yield to Maturity, there are two common methods of calculation. There is the bond pricing formula discussed later combined with an internal rate of return approximation that we would use with a computer spreadsheet. We can also use the same approximation formula as we used for the Yield to Maturity. The difference is we replace the Par Value with the Call Price and we replace the Number of Years to Maturity with the Number of Years to Call.

Call Value - Market Price

Annual Interest + —————————————————————————————

Number of Years to Call

YTC = ——————————————————————————————————————————————————

Call Value + Market Price

——————————————————————————————

2

Returning to the second Yield to Maturity example above, let’s say that the premium 8%, 10-year bond selling for $1,200 is eligible to be called in 5 years. The Call Protection Period ends in 5 years. For this example bond, if the bond issuer chooses to call the bond away from us, they must pay a Call Premium of $85. Hence, the Call Value is $1,085. Replacing the Par Value with the Call Value and the Number of Years to Maturity with the Number of Years to Call, we get the following formula:

$1,085 - $1,200 -$115

$80 + ————————————————— $80 + —————

5 5 $80 + (-$23) $57

YTC = ———————————————————————————— = ————————————— = ————————————— = ————————— = 0.049891 or 4.99%

$1,085 + $1,200 $2,285 $1,142.5 $1,142.50

————————————————— ————————

2 2

The Yield to Call was less than the Yield to Maturity. This is typical because if the bond is called away before maturity, we would have less time to take advantage of the outsized interest income payments of the premium bond. Note that if a bond is selling at Par Value, then the Nominal Yield / Coupon Yield, the Current Yield, the Yield to Maturity, and the Yield to Call will all be the same.

Taxable Equivalent Yield

Recall that municipal bonds are exempt from Federal income taxes. The Taxable Equivalent Yield formula takes this tax-exempt status into account. Before we compare the yield of a municipal bond with the yield of a corporate bond, we must calculate the Taxable Equivalent Yield. The formula is:

Taxable Municipal Bond Yield

Equivalent = ————————————————————————

Yield 1 - Marginal Tax Rate

Let’s take a look at a municipal bond that is paying 6% and assume that the investor is in the 25% Federal marginal tax bracket. The marginal tax bracket, also called the marginal tax rate, depends upon your level of income. As your income rises, so does your marginal tax bracket.

Taxable 0.06 0.06

Equivalent = —————————— = —————— = 0.08 or 8.00%

Yield 1 - 0.25 0.75

e result is telling us that our municipal bond is paying us as much as a corporate bond that is paying 8%. How is that? Well, the interest on the municipal bond is tax-exempt. We get to keep all of the interest we receive. On a 6% bond, that would be $60 annually. However, the interest on the corporate bond is fully taxable. That means we have to pay income taxes on the interest. We would receive $80 interest on the corporate bond but we would have to pay the Federal government 25% of that. The $80 of interest times 25% is $20 taxes. We would only get to keep $60. The two bonds would give us the same amount of money. They are equivalent.

Double Tax-free Equivalent Yield

If an investor purchases a municipal bond domiciled in their state of residence, most states will waive the state income tax on the interest, hence the bond is said to be double tax-free or double tax-exempt. In order to compare our double tax-exempt bond with a fully taxable corporate bond, we need to calculate the Double Tax-free Equivalent Yield. There are two versions of the formula, one for taxpayers who itemize their deductions and the other for taxpayers who do not itemize. Since most municipal bond investors are typically high net worth, high income taxpayers, this first formula is more useful.

Double

Tax-free Double Tax-Free Municipal Bond Yield

Equivalent = ———————————————————————————————————————————————————————————————

Yield 1 - (Federal Bracket + (State Bracket*(1- Federal Bracket)) )

Again, it looks a bit scary but if we just plug in the numbers and then work our way from the innermost parentheses to the outermost, we can do it. Let’s revisit the previous example with a 6% municipal bond yield and a 25% Federal tax bracket. Let’s assume this is a California bond and the taxpayers are California residents in the 8% California tax bracket. The formula becomes:

Double

Tax-free 0.06 0.06

Equivalent = ——————————————————————————— = —————————————————————— =

Yield 1 - (0.25+(0.08*(1-0.25))) 1 - (0.25+(0.08*0.75)

0.06 0.06 0.06

= ———————————————— = ——————————— = —————— = 0.0890565 or 8.696%

1 - (0.25+0.06) 1 - 0.31 0.69

Because the California resident does not pay Federal or state taxes on the interest from the California municipal bond, the Double Tax-free Equivalent Yield is higher than the Taxable Equivalent Yield. The second form of the formula is used when the taxpayer does not itemize deductions on their Federal income taxes. This is very unusual as most municipal bond investors are high net worth and high-income taxpayers. Here is the second version of the formula:

Double

Tax-free Double Tax-Free Municipal Bond Yield

Equivalent = ———————————————————————————————————————

Yield 1 - (Federal Bracket + State Bracket)

If the taxpayer in the previous example did not itemize deductions on their Federal tax return, then the Double Tax-free Equivalent Yield will be higher. The calculations would be:

Double

Tax-free 0.06 0.06 0.06

Equivalent = ———————————————— = ————————— = —————— = 0.89552 or 8.955%

Yield 1 - (0.25+0.08) 1 - 0.33 0.67

It turns out, the higher the taxpayer’s marginal tax bracket, the higher the Taxable Equivalent Yield and the Double Tax-free Equivalent Yield will be. For this reason, as mentioned, municipal bonds are more desirable for those in the high income tax brackets. For those in the lower tax brackets, municipal bond yields often do not compete with fully taxable corporate bonds. We must always compute the Taxable Equivalent Yield or the Double Tax-free Equivalent Yield before we can make an informed decision about which bond is best for us.