3.1: What Are Stocks?

- Page ID

- 79768

Stocks represent ownership in a corporation. The legal term is actually common stocks. Where did the term common stocks come from? The investors are “shareholders in common.” Investing in corporations goes back to the 1600’s. Entrepreneurs were eager to take advantage of the new trade routes and opportunities for development as pioneers explored the world. The entrepreneurs needed resources and sought out investors to fund their new ventures. Before the advent of stock investing, entrepreneurs would borrow money from wealthy investors with a promise to repay the money. These new corporations, on the other hand, sold common stock to raise the funds and the investors were now part owners of the venture. Hence, another term for stock investing is equity financing. Equity is another word for ownership.

The term stock is somewhat unfortunate. A much better term would be business. As a stock investor, you are investing directly in a business. You are a partial owner of the business. You are able to participate in the profits and growth generated by the business enterprise. Contrary to what many believe and how many behave, stocks are not simply millions upon millions of worthless pieces of paper ‒ now electronic bits! ‒ that people trade with one another each day for no apparent reason. Stocks represent ownership in real businesses.

However, unlike other forms of businesses such as a sole proprietor, investors of common stock are limited liability owners. A stock investor is only liable for their investment, even if the corporation incurs debts above and beyond the value of the stock. A sole proprietor, on the other hand, can be held liable for debts beyond the business value and creditors can attempt to seize the personal assets of the business owner, up to and including their personal residence. There are corporations that are established for the mere purpose of shielding assets from creditors. If the courts deem that the corporation’s sole purpose was simply to hide assets from creditors, the courts might allow creditors to “pierce the corporate veil.” For those interested in business structures and how businesses interact with the law, we recommend to you our BUS-120, Introduction to Business, and BUS-140, Business Law, at Southwestern Community College.

Why invest in stocks? Stock investors receive two optional benefits, dividends and capital appreciation. Dividends are optional payments of earnings from the business. Capital gains, also known as capital appreciation, occur when the value of the corporation rises as the business grows. Please note that both of these benefits are optional. They are not guaranteed. The corporation is not under any obligation to pay dividends although some companies have paid dividends for decades. Also note that there is no guarantee that the business will succeed. Hence, the expected capital gain may result in a capital loss. Stocks are risky! Stocks are volatile! (Recall that “volatility” is our industry’s euphemism for, “Aye! I lost a whole lot o’ money!”)

Prudent, long-term stock investors must learn how to handle the volatility of stocks. We discussed this in our previous chapter on mutual funds. If we can keep our heads while others are losing theirs and resist the temptation to panic when the markets fall, then we can learn to use the volatility to our advantage. And if we can keep that long-term perspective and not panic, historically, the rewards for stock investing have been significant. (Ah, did we mention that there are no guarantees? Yes? Good. Just wanted to be sure.)

Historical Performance

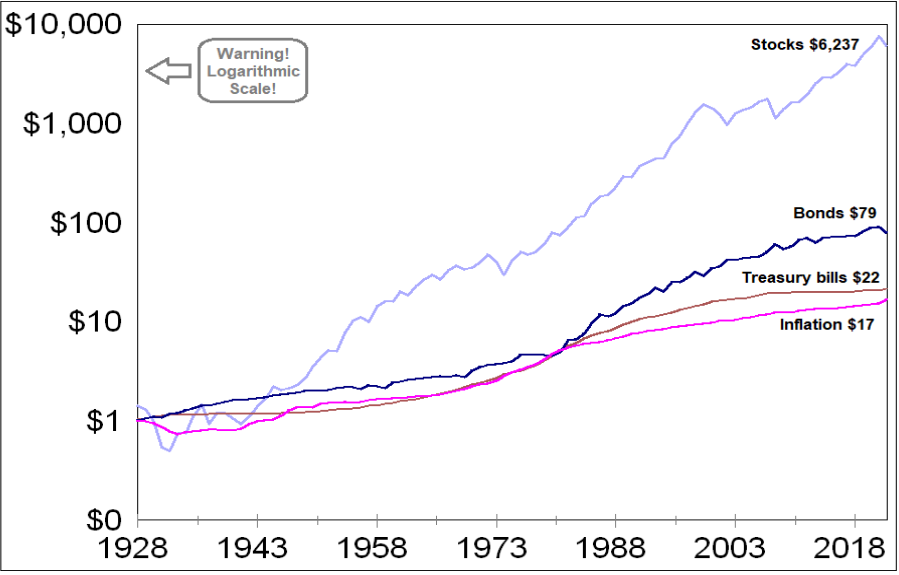

Over the long-term history of modern finance, stocks have given investors the best rewards of the major financial investment alternatives. The return from the stock market has averaged approximately 10% to 11% annually for the last ninety years. We get this statistic from a list of stocks called the Standard and Poor’s 500 Index which we will discuss in detail soon. Ten to eleven percent annual return on your investment is pretty good, yes? Wouldn’t it be just grand if we received that 10% or 11% each year? Sadly, investing in stocks does not work that way. In any given year, it is highly unlikely that the return will be 10% or 11%. The return has varied from a high of 53.8% in 1954 to a low of -43.4% in 1931. The return in 2008 was -38.5%, one of the worst! In any given year, there has been a one-in-three or one-in-four chance of a down market. And no, the stock market does not predictably go up for three or four years and then go down for one year. For example, from 1982 to 2000, with only two years of slight downturns, the market went in two directions, up and way up. It then proceeded to fall for three years in a row. Let’s revisit and reexamine some graphs from chapter 1.

Source: New York University Stern School of Business

The above graphic shows how investing in stocks compared with other popular alternatives. We see that over the long term, the rewards for stock investing have outpaced loans (represented by bonds), savings accounts and other short-term investments (represented by Treasury bills), and inflation (represented by the Consumer Price Index). However, to show this disparity, we used a logarithmic scale. Notice that the numbers of the left do not increase arithmetically, they increase exponentially. From $1, we jump to $10, then to $100, on to $10,000. This is because if we used an arithmetic scale, the lower three alternatives would all appear as essentially flat lines. The danger of using a logarithmic scale is that it makes large movements look small and may mask the magnitude of the historical downturns. It appears that the return on stocks is moving in a relatively straight line upward. This is not the case! Those little squiggles that represent downturns from 1973 to 1973, 2000 to 2002, and in 2008 were large drops downward, approximately 50% down in all three cases.

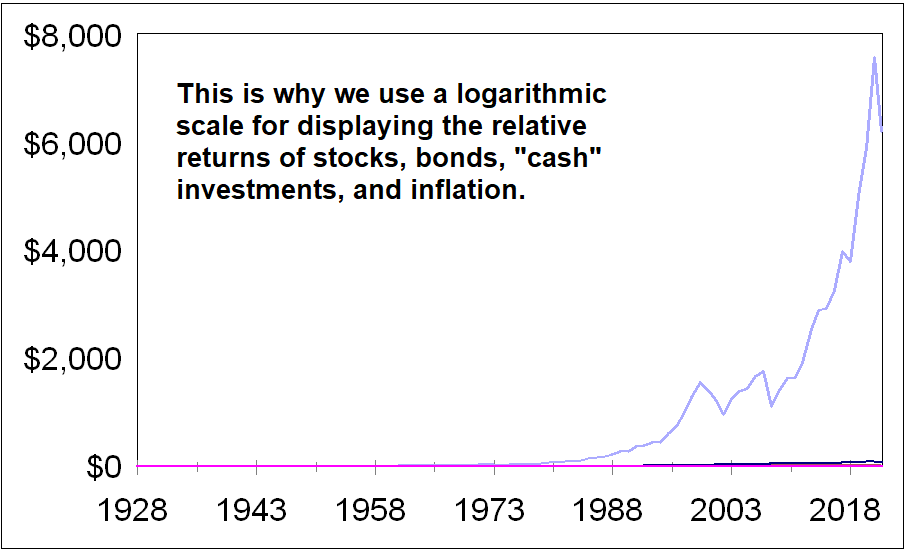

Here is the graph if we did not use a logarithmic scale:

This second graph uses an arithmetic scale. You know, the ones that we mere mortals are used to using. However, because of the exponential growth, we don’t begin to see any change in any of the investments until the 1970’s. Then we begin to see business investments, as represented by stocks, begin to climb far above their alternatives. We can begin to see the exponential swoosh upward of growth in the stock investments. And we can also see that the downturns in 2000-2002, 2008-2009, and 2022 were far more pronounced than they were in the first graph.

Why are we emphasizing the downturns? As you may already have guessed, we want you to be emotionally prepared for them. History tells us they will occur, most likely at least once or twice or more times in your investing career. Intellectually, we can see and learn and know that stocks reward us with the best financial investment returns. But when the economy falters, when the outlook is bleak, when the organic matter hits the ventilating device, when the end of the world is nigh, etc., and the markets subsequently plummet, we have to be prepared emotionally. We must not panic.

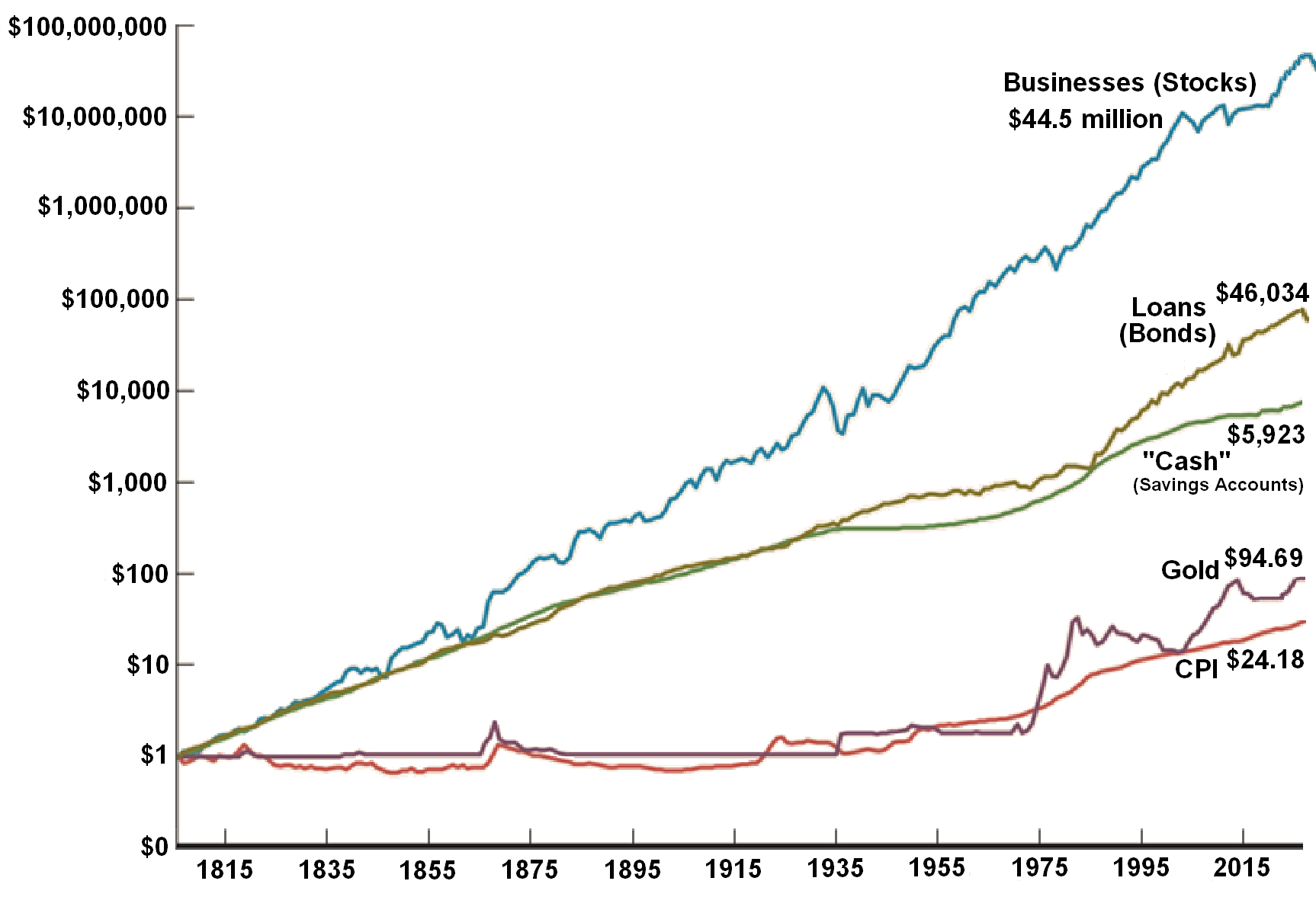

Let’s now take a look at a much longer time frame. Let’s go back to the dawn of the Industrial Revolution. We see that the rewards from investing in stocks are staggering. Again, if we used an arithmetic scale, none of the other alternatives would be noticeable. Notice how poorly gold has done relative to the other alternatives. We will discuss investing in precious metals near the end of our journey together.

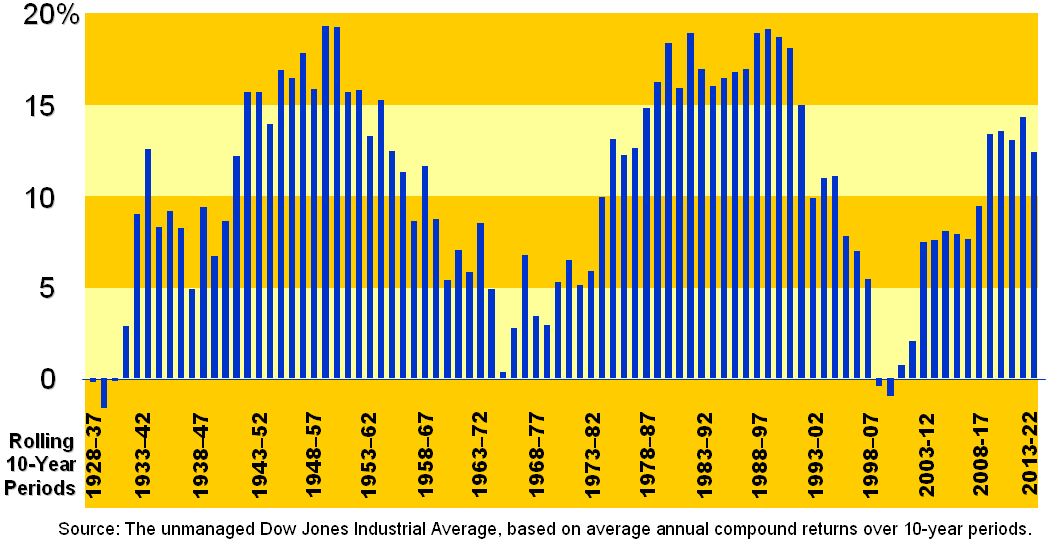

Okay, all right, none of us have a 200-year time frame. (It is entirely possible that some of the younger adults reading this may have a 100-year time frame, though. Supposedly, the first person to live to 150 has already been born.) Let’s break down our investment time horizons into rolling 10-year periods. Once again, we are reminded of the volatility that accompanies stock investing.

Source: Dow Jones Industrial Average, based on average annual compound returns over 10-year periods

Starting just before the Great Depression, we see three 10-year rolling periods where stocks have lost money. You invested $1,000 and in ten years, you had less than $1,000, for example. What did we hear people say? “Ooo, ooo, ooo! Is it too late to get out?!” Yes, as the United States and the world emerged from the Great Depression and World War II, we saw the greatest expansion of the economies of the United States and many parts of the globe that the world had ever seen. Dishwashers, televisions, air conditioning, refrigerators, washers and dryers, an automobile in every driveway! By the late 1950’s, the United States stock market had returned upwards of 20% over the 10-year rolling periods. What did your great-grandparents hear from their family members, friends, neighbors, and colleagues? “Ooo, ooo, ooo! Is it too late to get in?!” Once again, the answer was yes. We will let the famed investor, Peter Lynch, in his excellent, must-read book, One Up On Wall Street, describe the resulting 1973/1974 market crash:

“For two decades after the Crash of ’29, stocks were regarded as gambling by a majority of the population. This impression wasn’t fully revised until the late 1960’s when stocks once again were embraced as investments, but in an overvalued market that made most stocks very risky. Historically, stocks are embraced as investments and dismissed as gambles in routine and circular fashion, and usually at the wrong times. Stocks are most likely to be accepted as prudent at the moment they’re not.” – Peter Lynch

The 10-year return in the mid-1970’s was close to zero. It was a golden opportunity to invest in stocks. Yet, most potential investors ran the other way. Why? By now, we hope that you can answer that question on your own. Our emotions get the better of us. “Investing is simple … but it ain’t easy!”

Like clockwork, the cycle began all over again. Coming out of the 1970’s, the world began to hear the terms, “globalization,” “personal computers,” “mobile phones,” “telecommunications,” “Internet,” etc. The stock market in the 1980’s and 1990’s then proceeded to go in two directions, up and way up. By the end of the 1990’s, the 10-year rolling returns were again approaching 20%. “Ooo, ooo, ooo! Is it too late to get in?!” You know the answer! We were greeted with two vicious downturns, from 2000 to 2002 and then again in 2008. We saw for the first time since the Great Depression rolling 10-year periods with negative returns. “Ooo, ooo, ooo! Is it too late to get out?!”

Why? Why do we humans act this way, over and over again? We will discuss some of the psychological issues of investing later. For an in-depth study, we recommend Thinking Fast and Slow by Daniel Kanneman, the Nobel laureate who proved, once and for all, humans are not rational. Be prepared for some illuminating yet disconcerting news about human nature.

For ten years after the Global Financial Crisis and the Great Recession in 2008, the stock market again moved in two directions, up and way up. The Covid-induced recession of 2020 and then the rise of inflation and interest rates of 2022 led to two jarring downturns. But as of early 2023, the markets are again rising. Are we destined to repeat the cycle? We will know in 10 or 20 years. In the meantime, your guess is about as good as anyone else’s. The one truth we do know is that if you had kept investing, prudently and consistently, and did not panic when the markets fell, you would have profited greatly by investing in stocks.

The Power of Dividends

Traditionally, close to half of the return from stocks was from reinvested dividends. Stockholders used to expect 4% to 6% in dividends each year. That was as much or more than bonds returned in interest since stocks were considered much riskier than bonds. From 1936 to 2008, the average dividend return was 3.8%. Starting in the 1980’s, the return from dividends fell dramatically. From 1997 to 2007, the average dividend return was 1.5%. At the peak of the market in March of 2000, the dividend yield had fallen to 1.0%. Capital gains & growth were what investors wanted in the 1990’s. Many reasons were forwarded. They included the fact that dividends were taxed at a higher rate than capital gains, people wanted the business to reinvest the earnings for growth instead of distributing it to the investors, stocks were no longer considered riskier than bonds, and savings accounts were now paying less than 2%. But probably the most compelling reason was that people lost track of their senses and bid up the prices. It was the New Millennium! (Feels kinda' like the old millennium, don't you think?)

The market downturns of 2000-2002 and 2008 changed investors’ perception about dividends. We now see investors and companies focusing more and more attention on dividends. Many companies that never paid dividends in the past are doing so now. Good examples of this are the tech companies. Many tech companies are no longer growing at phenomenal rates and the industry as a whole is maturing. Mature companies can afford to distribute more of their earnings to shareholders. Also, the tax law has changed dividends so that they are taxed roughly the same as capital gains.

“Dividends Don’t Lie.” − Geraldine Weiss

“Do you know the only thing that gives me pleasure? It’s to see my dividends coming in.” − attributed to John D. Rockefeller

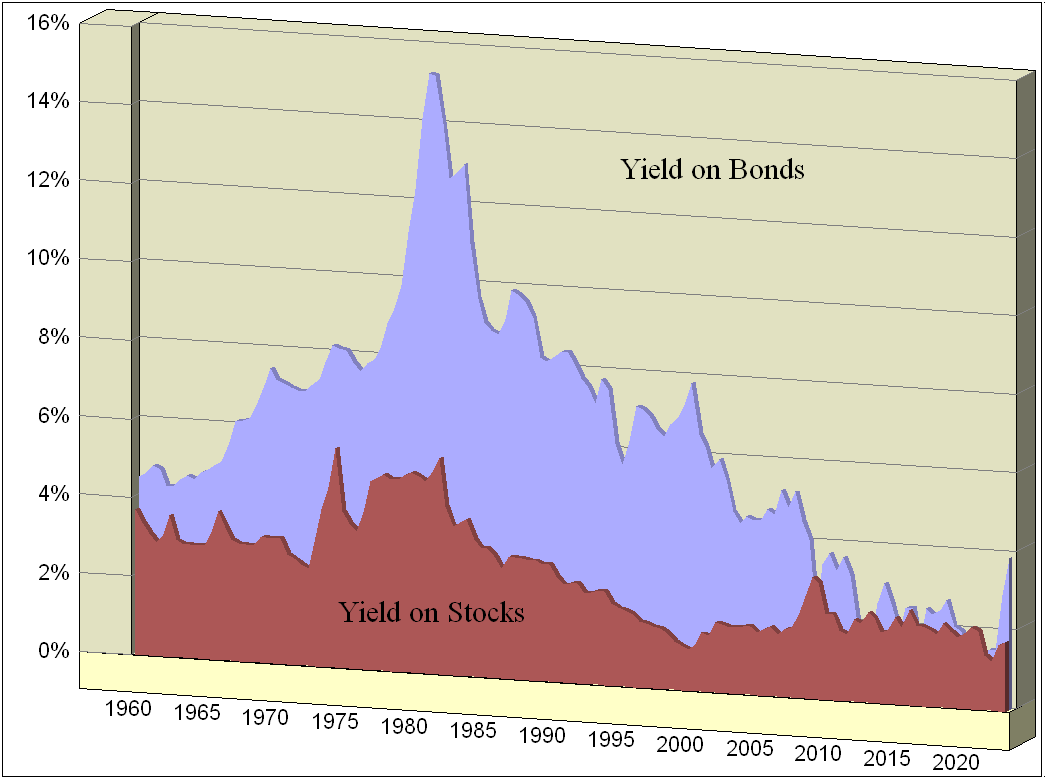

The dividend yield from stocks compared to the interest rate from bonds.

The graphic above shows the relationship between the dividend yield from stocks in red and the interest rate from bonds in blue. In 1960, they were fairly close to one another. As inflation rose in the late 1970’s, we saw the interest yield on bonds climbing as investors demanded a higher rate of interest to lend money. The dividend yield on stocks climbed also, but that was mostly because the prices of stocks fell sharply in the mid-1970’s. Starting in 1979 and then into the early 1980’s, the Federal Reserve Bank raised short-term interest rates to break the back of inflation. It worked! We saw both the interest rates on bonds and the dividend yields on stocks falling in what has been called the Great Moderation. It was a time of great wealth accumulation … until the market crashes of 2000 to 2002 and 2008. Since the Global Financial Crisis and Great Recession, the two had been fairly close to one another and the markets have gone in two directions, up and way up. That changed in 2022 when the Federal Reserve Bank raised interest rates dramatically to combat the Covid-induced inflation. What will the future bring? Your Humble Author’s crystal ball is about as useful as anyone else’s. However, we do know that the only constant is change and that we are guaranteed at least one or maybe two dramatic downturns in the next 10 to 20 years. As Mr. Peter Lynch says, down markets are as inevitable as snowstorms in January. Prudent, long-term investors weather the storms and wait for the good times to come again. In the meantime, dividends always give us investors a positive return on our investment. “Dividends don’t lie!”

Bull Markets versus Bear Markets

By now, no doubt you have heard the two popular phrases for the upward and downward swings in the stock market. Bull markets are favorable markets normally associated with rising prices, investor optimism, economic recovery, and government stimulus. Bear markets are unfavorable markets normally associated with falling prices, investor pessimism, economic slowdown, and government restraint. Where did the terms bull market and bear market come from? Typically, we point to the manner in which bulls and bears fight and attack their opponents. Bulls charge ahead and throw their opponents up into the air. Bears use their paws and claws to slash downward. Of course, the actual origins of the phrases are more complicated than these simplistic descriptions and a great source of sport and entertainment for all budding etymologists, seeking to enlarge their knowledge base of word origins.

Advantages and Disadvantages of Stock Investing

Along with the best historical returns over time for financial assets via dividends and capital gains, there are other advantages of stock investing. To review, stock investing allows the general public to share in the rewards of global business enterprises. Stock investors enjoy limited liability and can only be held responsible for their monetary investment. Additionally, in general, stocks are very liquid investments; they are easy to buy and sell. (There are exceptions to this advantage. Stocks of many sham or very distressed companies may be very illiquid. Most are “penny stocks” that are utilized in scams and swindles perpetrated by con artists. We will learn how to identify and stay far away from these tricksters.)

Finally, an advantage that is often overlooked is that the capitalist system has resulted in an increased standard of living for all. Nothing we humans do or have done is perfect and that includes our economic system. In fact, capitalism might just be the worst possible system for distributing goods and services to a population … except for all the others! We have a long way to go until the time when every person has access to clean water and healthy food, adequate clothing, and safe shelter … and Internet access, of course. If some other system comes along that proves its worth above and beyond capitalism, we will be sure to give it a chance. In the meantime, we global investors are helping raise the standard of living all around the world and at the same time, earning a good return on our investments. (My apologies. It sounds like a public service advertisement, eh?)

Now, what are the disadvantages of stock investing? Hopefully, as you have already observed and internalized, stock investing is risky. Stocks are “volatile.” (Recall that “volatility” is our industry’s popular euphemism for, “Hey! I lost a whole lot o’ money!”) The volatility of the stocks of legitimate companies is bad enough when markets fall or a company falls on bad times. Added to this is the fact that there are many scam “penny stock” corporations that are used in various swindles. Even some well-known, bona fide companies have engaged in deception and misconduct. But even with all the volatility and financial “hanky-panky,” remember that stocks have been the best financial assets over the long term. (Note that we are qualifying our statement about investment returns with the use of the word financial. This is to placate the real estate investors who might now be jumping up and down screaming that real estate investing has done better than stock investing. Recall that the two are very different. The difference mainly rests with how stocks are purchased and how real estate is purchased. We will discuss real estate investing and highlight the differences near the end of our journey together.)

Volatility Examined

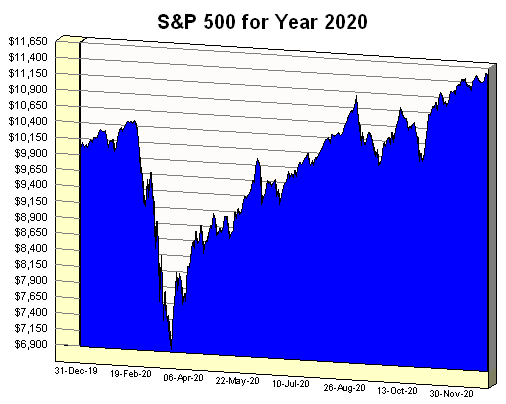

The graphic below demonstrates the volatility inherent in stock investing. Suppose you had stock investments of $10,000 on January 1, 2020. To be sure, the year 2020 is one that most of us would rather forget thanks to the Covid-19 pandemic. But for some unfortunate investors, there is another reason they will want to forget 2020. Note the dramatic downturn as the world became aware of just how dangerous Covid-19 was. 2020 recorded the fastest bear market on record. Those uninformed investors who sold in late March or early April locked in 30% declines. They were then left with the difficult decision of when to jump back in. Many never did. (Psst. When would you have heard your friends, family members, and colleagues saying, “Ooo, ooo, ooo! Is it too late to get out?” Hint: It was about the same time that we were all hoarding toilet paper.)

On the other hand, if you had simply turned off the tele, stopped swiping your mobile device, and stopped checking your brokerage account online and instead went to the park to play volleyball with your kids, you would have enjoyed the fastest recovery from a bear market on record. In fact, you did pretty darn well for yourself in spite of the Covid-19 pandemic and a very contentious United States presidential election.

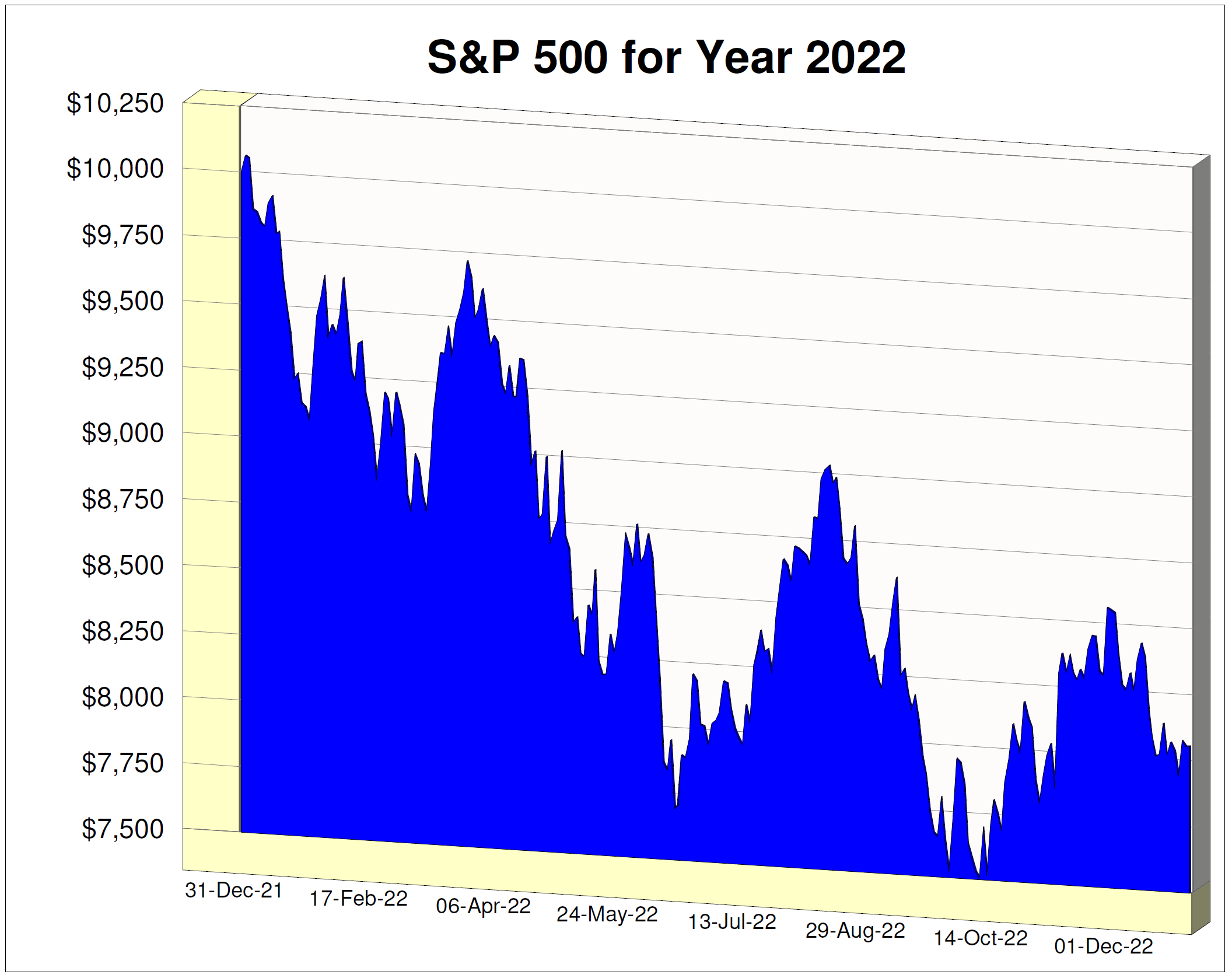

Let’s now take a look at 2022, another challenging year.

What a roller coaster! You put $10,000 into the market at the beginning of the year. It promptly dropped more than 10% to less than $9,000. Of course, being a concerned investor, you quickly pull out your money … only to see the market rise 10%. You put your money back in and watch it now fall 20%! Okay, that’s enough, you pull out your money and the market then rises 16%. All right, one more time. You put your money back in and it falls again, this time 16%. “¡Aye, no más! ¡Nunca jamas!” Never again you will invest. Oh, by the way, if you had just left your $10,000 in the market the whole year, you lost about 18% and your $10,000 became $8,200. By trying to time the market and moving in and out, your $10,000 became $5,880.

The volatility is real, Dear Students. It’s the price we pay for investing in stocks. Oh, well.