2.5: Regulation and Organization of Mutual Funds

- Page ID

- 79827

Video - Audio - YouTube (Material for this page starts on slide #16.)

The mutual fund industry in the United States started in the mid-1920’s. The concept was borrowed from the famous Scottish Investment Trust that has been in operation since the 1880’s. The idea was to be able to bring professional money management and diversification to the masses. At first, some regulators were very skeptical about these new investment alternatives and some states had conflicting rules and regulations. Especially troublesome from the governments’ viewpoints was how these entities should be taxed. That all changed with the Investment Company Act of 1940. This legislation is the foundation of the modern mutual fund industry. The Investment Company Act defined a “regulated investment company,” also known as a “pass-through” investment vehicle. The mutual fund does not pay taxes on the interest, dividends, and capital gains from the underlying investments. Instead, the mutual fund “passes through” the rewards to the investors and the investors are responsible for any subsequent taxes. (The mutual fund earns its money from the fees charged to the investors and must pay any taxes on those earnings.)

There are several rules, regulations, and guidelines that must be adhered to for a company to qualify as an investment company. The entity must hold almost all its assets as investments in stocks, bonds, and other traditional securities. It has a very limited ability to use derivatives and other risky strategies. Also, the mutual fund may use no more than 5% of its assets when acquiring a particular security. This rule is crucial. By limiting the amount of assets to 5% to any one particular stock or bond, the mutual fund is guaranteed to have at least 20 securities. Obviously, most mutual funds have far more investments in their portfolio but there are some mutual funds that do limit their portfolios to the bare minimum. One such fund was the infamous Janus 20 mutual fund. Where did the name come from? Again, a mutual fund must have at least 20 different stocks, bonds, or other securities. The strategy of the Janus 20 fund was to have a portfolio of only 20 stocks. This anti-diversification strategy works great ‒ if you choose 20 great stocks. Of course, if even one or two of your choices don’t work out as expected, it can quickly sour the long-term results of a mutual fund. If you investigate the history of the Janus 20 fund, you will find that this is exactly what happened. Janus 20 was a high-flying and very popular mutual fund ‒ until 2008. Janus finally merged the fund into another mutual fund ‒ Janus 40! This is an example of what is called in the industry “burying the evidence.” It happens far more often than it should.

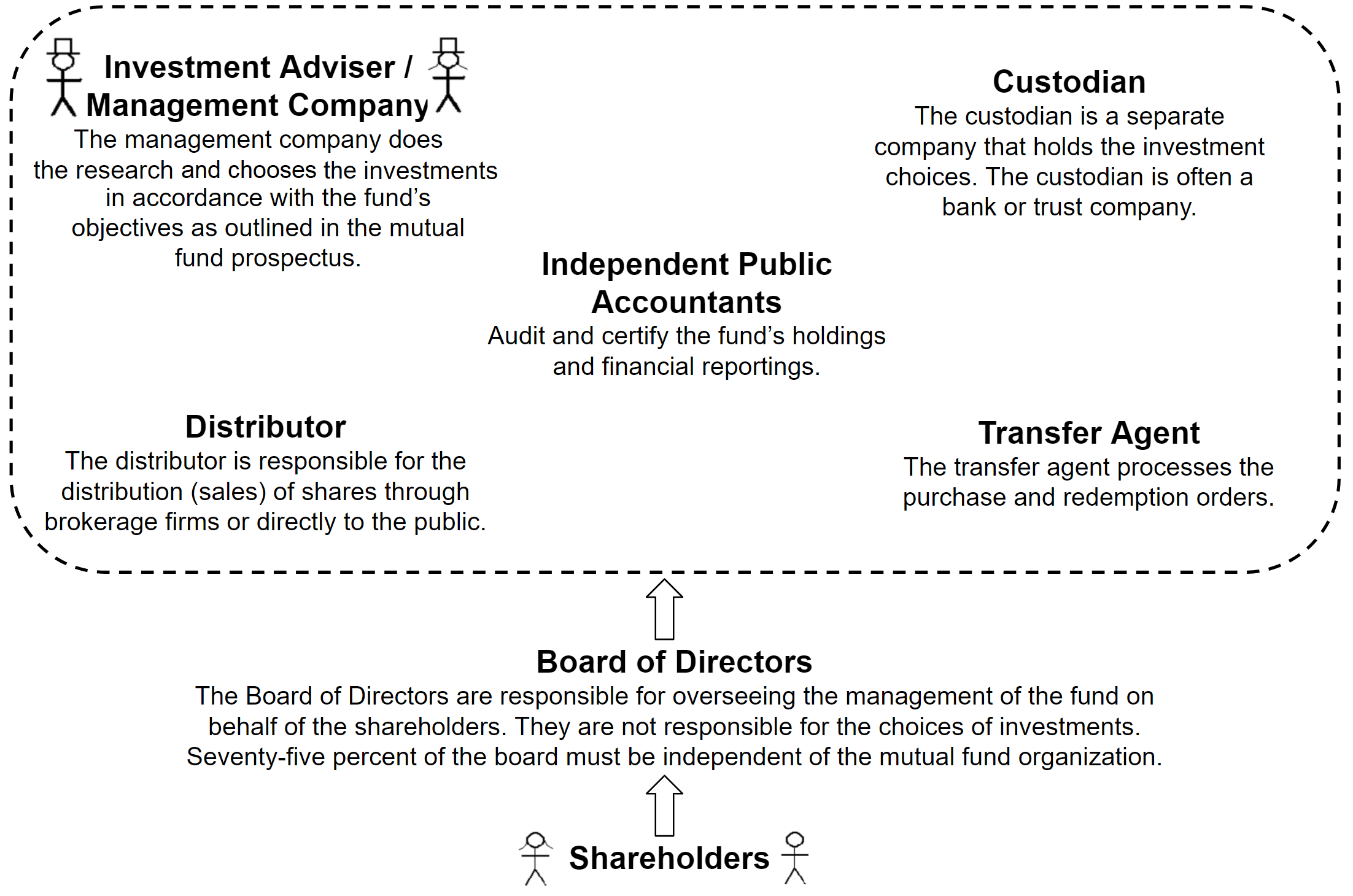

Another important provision of the Investment Company Act of 1940 is that mutual funds must create an organization with “checks and balances.” This is the exact same concept that is embedded into the Constitution of the United States and is taught in high school Civics and United States History classes. In the case of mutual funds, the idea was to help ensure that the investors’ assets would be protected by separating the various tasks among several different entities. In truth, a mutual fund is not just one company; it consists of a group of companies.

The mutual fund is a corporation run by a Board of Directors for the benefit of the investors who are shareholders in the corporation. The Board of Directors is voted in by shareholders and are charged with overseeing the fund operations on behalf of the shareholding investors. In the past, some Boards of Directors were criticized for not exercising the highest standards in fiduciary oversight. This is a fancy way of saying that they were asleep at the wheel. Some Board Members are paid handsomely for their services. Critics contend that this creates a conflict of interest and question whether Board Members would be fearful of jeopardizing their positions by being too critical of the mutual fund management.

By far, the most important component of the mutual fund structure is the Investment Manager, also known as the Management Company or simply the Fund Manager. This is the company that is charged with researching, identifying, choosing, and then monitoring the securities that will populate the mutual fund. Many mutual fund companies use what is sometimes referred to as the “star manager” approach where one individual is responsible for all the final decisions of what investments will be included in the fund. This person is assisted by many research analysts who cover specific sectors and industries such as energy, technology, and health care. Other companies use a committee that must come to a consensus about which securities to buy. An approach that is a hybrid of these two strategies is to have several money managers responsible for the investment decisions. The group does their research as a team but the individual money managers make their own decisions. This approach is gaining popularity as it has some advantages over the “star manager” approach. It allows the portfolio managers to focus on fewer investment choices, ones in which they have the most conviction. It also allows for a smoother transition when a money manager leaves the firm. This is in stark contrast to the problem a “star manager” mutual fund has when their individual retires or joins another firm.

The custodian is the company that actually holds the securities. This company is often a bank or trust company. The investment manager makes the decisions, the custodian company holds the investments. This is done to reduce the risk of any financial misconduct and is part of the “checks and balances” that is built into the mutual fund. As their name suggests, the distributors distribute the shares to the public or to other financial professionals dealers who then deal with their own clients. The transfer agent keeps track of purchase and redemption requests from shareholders, not the most glamorous of tasks in the investment industry but very important, nonetheless. Lastly, the independent public accounting firm certifies the fund’s financial operations and reports. They are the watchdog that ensures that the investments are safe and sound and that there is no financial fraud. Normally the independent public accounting firm is one of the Big Four public accounting firms. (Note: In the case of the fraud perpetrated by Bernie Madoff, the accounting firm that he was using was some guy out in Connecticut working who worked out of his garage.)

Why the large diversification of tasks and companies? Mutual funds are highly regulated in order to protect shareholders’ investment from fraud and collapse. How often have you heard of a scandal at a mutual fund company? Until 2003, never.

“Wait a minute, Paiano! Did you just say, ‘Mutual Fund Scandals?!’ You want me to invest in an industry that is plagued with scandal?!” Well, as a matter of fact, yes, I do. I want you to invest in mutual funds. But on the contrary, the industry is not nor has it ever been plagued with scandal. Since 1940, the mutual fund industry has been regulated and for decades escaped any but the slightest hints of impropriety. In 2003, some practices that were not quite illegal but obviously unethical were uncovered. Only a handful of mutual fund companies and people in the firms were affected such as Strong, Janus, Bank of America, Putnam, and Alliance. The vast majority of companies never engaged in any of the shenanigans. Two individuals at Alliance were guilty of these improper actions and the entire company was unfairly tarred and feathered. The worst example was the sad story of Strong Funds where the CEO, Richard Strong, who built the company from scratch, supposedly earned $600,000 in ill-gotten gains. This was a man who was worth a reported $800 million dollars at the time of the ruse. What causes a titan in the industry to risk their most important asset, their good name and reputation, for what to him was essentially pocket change? Mr. Strong was barred from life from the securities industries, paid a $60 million fine, and publicly apologized for his actions. Strong Funds paid $115 million in penalties and $80 million to investors. And unlike most such settlements, the firm admitted wrongdoing and apologized to its investors. The assets of Strong Funds were eventually sold to Wells Fargo and, once again, the evidence was buried.

What were these terrible things that these few rascals were guilty of? We won’t get into the gory details of mutual fund late trading and market timing. Although these actions were certainly dishonest and corrupt, the effect upon the average mutual fund investor was essentially unnoticeable. Those who invested heavily in Enron, WorldCom, or Bernie Madoff lost $99,999 on a $100,000 investment. In contrast, the investors of the affected mutual funds typically lost less than a penny on a $100,000 account. The offenders were stealing hundredths of pennies from their fellow mutual fund investors. There just happened to be millions of said fellow mutual fund investors to steal a few hundredths of a penny from every few days or so. Even though the harm was negligible to the typical mutual fund investor, these actions were counter to the honest and principled operation of a mutual fund. Again, only a handful of culprits were guilty. As usual, it is the very few who give all the hard-working, honest professionals a bad name.