2.1: Introduction to Mutual Funds

- Page ID

- 79765

When teaching Introduction to Investments, one is confronted with the thorny problem of where to put mutual funds in the class. There are advantages to having mutual funds taught after stocks and bonds. Since almost all mutual funds rely on stocks and bonds as their underlying investments, it helps to have become acquainted with the ins and outs of stock and bond investments before tackling mutual funds. However, the advantages of teaching mutual funds before stocks and bonds are tempting. First, since investing in mutual funds is almost certainly to be in almost everyone’s future via individual and employer-sponsored retirement plans, it pays to be introduced to them as soon as possible, especially since for whatever reasons, many students will drop the class within the first few weeks. Also, as we slog through the copious amount of concepts, definitions, attributes, calculations, etc. of stocks and bonds, inevitably several students will decide, “Ya’ know, this stuff just ain’t for me.” That is fine! That is something we hope you will be able to decide for yourself as we progress through the semester. Not everyone will have the time, inclination, aptitude, and most importantly, receive enjoyment from doing the detailed research necessary to identify, choose, and continuously monitor individual stock and bond purchases. If you are one of those who decides that investing in individual stocks and bonds is not for you, no problem! That’s why mutual funds exist! But whether you are an Investment Guru that relies upon mutual funds or one who chooses your own individual stocks and bonds, or both, it is important that you know and understand mutual funds thoroughly. Mutual funds are in your future. And remember that your friends, family members, and colleagues are counting on you. So let’s get started!

What is a Mutual Fund? An Investment Company!

A mutual fund is an investment company that invests its shareholders’ money in a diversified portfolio of securities. Investment company is the legal term; mutual fund is the popular term. Mutual funds are one type of investment company; there are others. By far, though, the most popular investment companies are mutual funds. Although the term mutual fund does connote that investors are getting together to invest with one another, the term investment company more accurately describes the work of the mutual fund. The mutual fund will invest on your behalf.

The mutual fund industry is immense. There are approximately 12,000 mutual funds available in the United States. How could this be? Are there 12,000 different types of breakfast cereals in the grocery stores? Are there 12,000 different types of cars or mobile phones available for purchase? Why and how has the number of mutual funds grown to such an unwieldy number? The mutual fund industry is also very lucrative. The competition is ferocious. As we shall see, the number of categories and numbers of mutual funds has exploded as companies have been competing for business for the past several decades. Also, as mentioned, mutual funds are very popular with employer-sponsored and individual retirement plans. We find that this is the most difficult issue with mutual funds: How do you choose the best mutual fund for you?! The answer: It ain’t easy! However, once you have chosen a mutual fund or maybe two or three mutual funds, your work is done. The rest is up to the mutual fund.

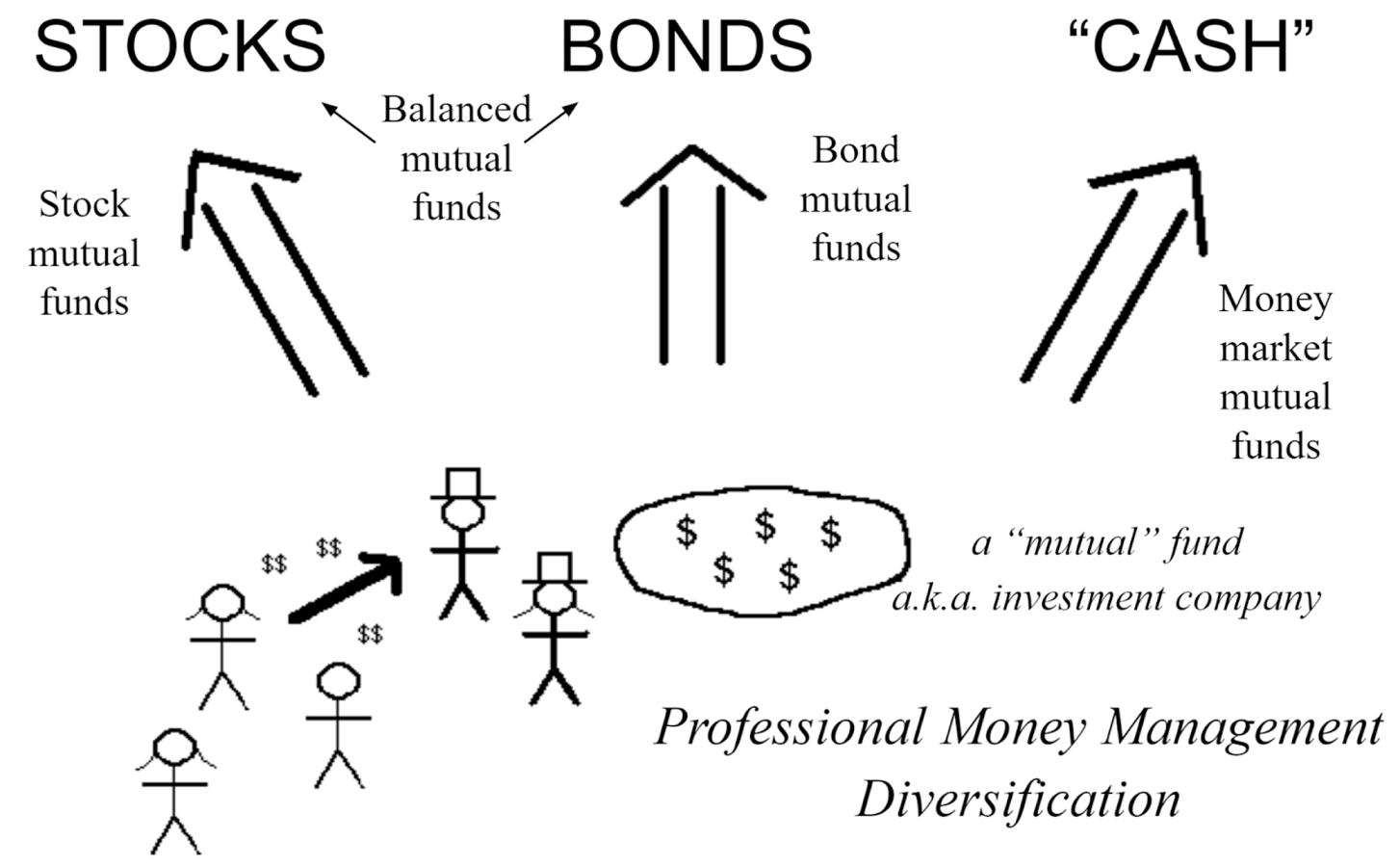

The graphic below is a very rudimentary representation of how mutual funds work. The people on the lower left are we, the Little Folk. We contribute $25 or $50 or $100 or whatever we can comfortably afford per month to the people in the top hats. These individuals are the mutual fund managers, also known as portfolio managers, portfolio counselors, and money managers. The mutual fund managers are highly skilled and well-paid professionals whose job it is to identify, choose, and monitor the underlying investments in the mutual fund. If the mutual fund managers purchase stocks for the mutual fund, it is called a stock mutual fund. If they purchase bonds, it is called a bond mutual fund. If the mutual fund concentrates on the short-term “cash” vehicles that we discussed in chapter 1, the mutual fund is called a money market mutual fund but is usually just referred to as a money market or money market fund. We also can see that a mutual fund that invests in both stocks and bonds is called a balanced mutual fund. This is just the beginning of the many categories and types of mutual funds. There are literally dozens of other categories. We will learn about a dozen as the rest are variations on the categories that we will cover.

Every month, there are millions of us Little Folk giving billions of dollars to the folks in the top hats. They create huge pools of money, hence the term “mutual funds.” Because this is their career and their full-time job, the mutual fund managers can afford to identify many choices of their underlying investments. The mutual fund managers don’t just purchase 10 or 20 stocks or bonds, which is typical for an individual investor. They purchase 100 or 200 or many hundreds of stocks or bonds. Therefore, we find that the two major advantages of mutual funds over individual stock and bond investments are professional money management and diversification.

Professional money management is sometimes the subject of some controversy. There are some in the industry and the public who question whether or not the mutual fund managers are really worth the high salaries they earn. For now, suffice to say that some are and some aren’t. We will discuss this controversy throughout our coverage of mutual funds. However, most investors do not question the advantage of managing the risks inherent in investing through diversification. Having a wide range of stocks or bonds across the various categories of each will help us eliminate much but not all of the risks of choosing individual stocks and bonds. You have heard the saying, “Don’t put all your eggs in one basket.” With a mutual fund, you are putting your eggs into hundreds of baskets. There are some who shun and even mock diversification but they are not investors. They are the short-term speculators and traders. They most likely put down this book before reaching the end of chapter 1 since we are catering to prudent, patient, long-term investors. Dear Students, for us investors, diversification is a good thing.