21.1: Introduction

- Page ID

- 34239

As noted earlier in this text, individuals rely on several sources for income during retirement: Social Security, employer-sponsored retirement plans, and individual savings (depicted in our familiar three-step diagram). In "18: Social Security", we discussed how Social Security, a public retirement program, provides a foundation of economic security for retired workers and their families. Social Security provides only a basic floor of income; it was never intended to be the sole source of retirement income.

Employees may receive additional retirement income from employer-sponsored retirement plans. According to the Employee Benefit Research Institute (EBRI), of the $1.5 trillion in total employee benefit program outlays in 2007, employers spent $693.9 billion on retirement plans. Retirement obligations, mostly in the form of mandatory social insurance programs, made up the largest portion of employer spending on benefits in 2007.Employee Benefits Research Institute, EBRI Databook on Employee Benefits, ch. 2: “Finances of the Employee Benefit System,” updated September 2008, http://www.ebri.org (accessed April 17, 2009). Private retirement benefits are an important component of employee compensation, especially because many large employers are transitioning from providing a promise at retirement through a defined benefits plan (as explained later) into helping employees invest in 401(k) plans. Big corporations such as IBM froze their promise for defined benefits plans for new employees entering employment with the company. Watson Wyatt Worldwide found that seventy-one Fortune 1,000 companies that sponsored defined benefits plans froze or terminated their defined benefits plans in 2004, compared with forty-five in 2003 and thirty-nine in 2002. An example is Hewlett Packard where, effective 2006, newly hired employees and those not meeting certain age and service criteria are covered by 401(k) with matching only.Judy Greenwald, “Desire for Certainty, Savings Drives Shift from DB Plans,” Business Insurance, September 19, 2005, www.businessinsurance.com/cgi-bin/article.pl?articleId=17551&a=a&bt=desire+for+certainty,+savings (accessed April 17, 2009); Jerry Geisel, “HP to Phase out Defined Benefit Plan,” Business Insurance, July 25, 2005, www.businessinsurance.com/cgi-bin/article.pl?articleId=17263&a=a&bt=hp+to+phase+out (accessed April 17, 2009); Jerry Geisel, “Congress Responds to Pension Failure Stories,” Business Insurance, July 11, 2005, www.businessinsurance.com/cgi-bin/article.pl?articleId=17156&a=a&bt=pension+failure+stories (accessed April 17, 2009).

These issues and more will be clarified in this chapter as we discuss the objectives of group retirement plans, how plans are structured and funded, and the current retirement crisis for the baby boomers (U.S. workers born between 1946 and 1964) who are entering their golden retirement years.Matt Brady, “ACLI: Bush Is Right About the Boomers,” National Underwriter Online News Service, February 1, 2006, www.lifeandhealthinsurancenews.com/News/2006/2/Pages/ACLI--Bush-Is-Right-About-The-Boomers.aspx?k=bush+is+right+about+the+boomers (accessed April 17, 2009). The chapter covers the following topics:

- Links

- The nature of qualified pension plans

- Types of qualified plans, defined benefits plans, defined contribution plans, other qualified plans, and individual retirement accounts (IRAs)

- Annuities

- Pension plan funding techniques

Links

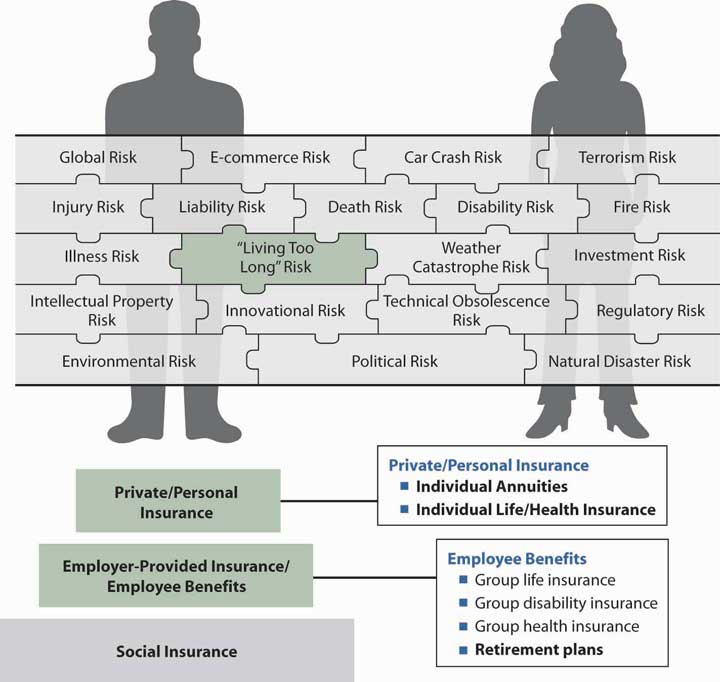

In our search to complete the risk management puzzle of Figure \(\PageIndex{1}\, we now add an important layer that is represented by the second step of the three-step diagram: employer-sponsored pension plans. The pension plans provided by the employer (in the second step of the three-step diagram) can be either defined benefit or defined contribution. Defined benefit pension plans ensure employees of a certain amount at retirement, leaving all risk to the employer who has to meet the specified commitment. Defined contribution, on the other hand, is a promise only to contribute an amount to the employee’s separate, or individual, account. The employee has the investment risk and no assurances of the level of retirement amount. Defined benefit plans are insured by the Pension Benefit Guaranty Corporation (PBGC), a federal agency that ensures the benefits up to a limit in case the pension plan cannot meet its obligations. The maximum monthly amount of benefits guaranteed under the PBGC in 2009 for a straight life annuity at 65 percent is $4,500 and for joint and 50 percent survivor annuity (explained later) is $4,050.Pension Benefit Guaranty Corporation (PBGC) News Division, “PBGC Announces Maximum Insurance Benefit for 2009,” November 3, 2008, www.pbgc.gov/media/news-archive/news-releases/2008/pr09-03.html (accessed April 17, 2009). The employee never contributes to this plan. The prevalence of this plan is on the decline in the new millennium. The PBGC protects 44 million workers and retirees in about 30,000 private-sector defined benefit pension plans.

Another trend that became prevalent and has received congressional attention is the move from the traditional defined benefit plans to cash balance plans, a transition that has slowed down in the first decade of the 2000s due to legal implications. Cash balance plans are defined benefit plans, though they are in a way a hybrid between defined benefit and defined contribution plans. More on cash balance plans, and all other plans, will be explained in this chapter and in the box “Cash Balance Conversions: Who Gets Hurt?”

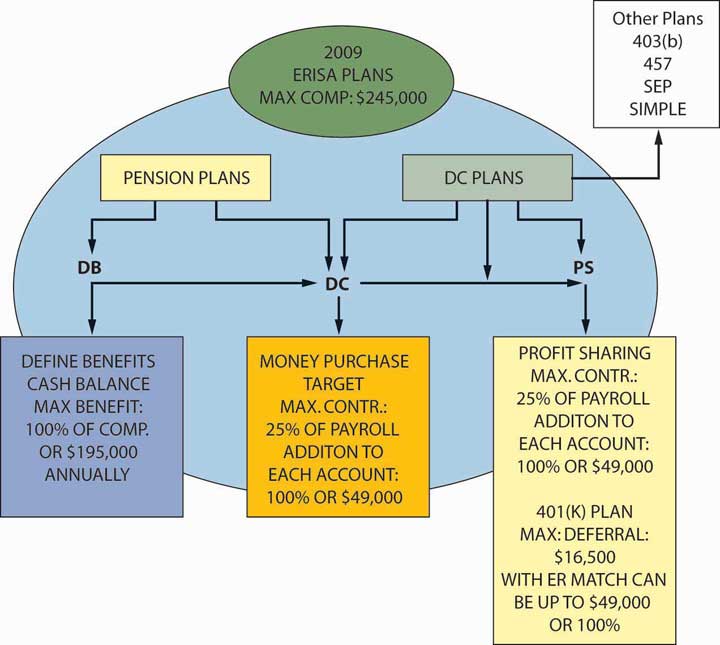

The most common plans are the defined contribution pension plans. As noted above, under this type of plan, the employer provides employees with the money and the employees invest the funds. If the employees do well with their investments, they may be able to enjoy a prosperous retirement. Under defined contribution plans, in most cases, employees have some choices for investments. Plans such as money purchase, profit sharing, and target plans are funded by employers. In another type of defined contribution plan, employees contribute toward their retirement by forgoing their income or deferring it on a pretax basis, such as into 401(k), 403(b), or 457 plans. There are also Roth 401(k) and 403(b) plans, where employees contribute to the plans on an after-tax basis and never pay taxes on the earnings. These plans are sponsored by employers, and an employer may match some portion of an employee’s contribution in some of these deferred compensation plans. Because it is the employees’ savings, they can say that it belongs in the third step of Figure \(\PageIndex{1}\. However, because it is done through the employer, it is also part of the second step. The pension plans discussed in this chapter are featured in Figure \(\PageIndex{2}\.

As you can see, we need to know what we are doing when we invest our defined contribution retirement funds. During the stock market boom of the late 1990s, many small investors put most of their retirement funds in stocks. By the summer of 2002, the stock market saw some of the worst declines in its history, with a rebound by 2006. Among the reasons for the decline were the downturn in the economy; the terrorist attacks of September 11, 2001; and investors’ loss of trust in the integrity of the accounting numbers of many corporations. The fraudulent behavior of executives in companies such as Enron, WorldCom, and others led investors to consider their funds not just lost but stolen.Kara Scannell, “Public Pensions Come Up Short as Stocks’ Swoon Drains Funds,” Wall Street Journal, August 16, 2002. On July 29, 2002, President George W. Bush signed a bill for corporate governance or corporate responsibility to rebuild the trust in corporate America and punish fraudulent executives.Elisabeth Bumiller, “Bush Signs Bill Aimed at Fraud in Corporations,” New York Times, July 30, 2002. “The legislation, among other things, brought the accounting industry under federal supervision and stiffened penalties for corporate executives who misrepresent company finances.”Greg Hitt, “Bush Signs Sweeping Legislation Aimed at Curbing Business Fraud,” Wall Street Journal, July 21, 2002. Congress also worked on legislation to safeguard employee 401(k)s in an effort to prevent future disasters like the one suffered by Enron employees, who were not allowed (under the blackout period) to diversify their 401(k) investments and lost the funds when Enron declared bankruptcy. In May 2005, lawyers filed suits on behalf of AIG 401(k) participants, alleging that AIG violated the Employee Retirement Income Security Act by failing to disclose improper business practices and by disseminating false and misleading financial statements to investors that led to reductions in AIG stock prices.Jerry Geisel, “Senate Finance Committee Passes 401(k) Safeguards,” Business Insurance, July 11, 2002; “401(k) Participants File Class-Action Suit Against AIG,” BestWire, May 13, 2005; “Lawyers File Suit on Behalf of AIG Plan Members,” National Underwriter Online News Service, May 13, 2005. The reform objective is intended to give more oversight and safety measures to defined contribution plans because these plans do not enjoy the oversight and protection of the PBGC. The 2007–2008 economic recession has brought about a plethora of new problems and questions regarding the merits of defined contribution plans, which will be the subject of the box, “Retirement Savings and the Recession.”

In this chapter, we drill down into the specific pieces of the puzzle that bring us into many challenging areas. But we do need to complete the holistic risk management process we have started. This chapter delivers only a brief insight into the very broad and challenging area of pensions. Pensions are also featured as part of Case 2 in "23: Cases in Holistic Risk Management".