9.1: Introduction

- Page ID

- 24521

The insurance contract (or policy) we receive when we transfer risk to the insurance company is the only physical product we receive at the time of the transaction. As described in the Risk Ball Game in "1: The Nature of Risk - Losses and Opportunities", the contract makes the exchange tangible. Now that we have some understanding of the nature of risk and insurance, insurance company operations, markets, and regulation, it is time to move into understanding the contracts and the legal doctrines that influence insurance policies. Because contracts are subject to disputes, understanding their nature and complexities will make our risk management activities more efficient. Some contracts explicitly spell out every detail, while other contracts are considered incomplete and their interpretations are subject to arguments.The origin of the analysis of the type of contracts is founded in transaction cost economics (TCE) theory. TCE was first introduced by R. H. Coase in “The Nature of the Firm,” Economica, November 1937, 386–405, reprinted in Oliver E. Williamson, ed., Industrial Organization (Northampton, MA: Edward Elgar Publishing, 1996); Oliver E. Williamson, The Economic Institution of Capitalism (New York: Free Press, 1985); application to insurance contracts developed by Etti G. Baranoff and Thomas W. Sager, “The Relationship Among Asset Risk, Product Risk, and Capital in the Life Insurance Industry,” Journal of Banking and Finance 26, no. 6 (2002): 1181–97. For example, in a health contract, the insurer promises to pay for medicines. However, as new drugs come to market every day, insurers can refuse to pay for an expensive new medication that was not on the market when the contract was signed. An example is Celebrex, exalted for being easier on the stomach than other anti-inflammatory drugs and a major favorite of the “young at heart” fifty-plus generation. Many insurers require preauthorization to verify that the patient has no other choices of other, less expensive drugs.Testimonials and author’s personal experience. The evolution of medical technology and court decisions makes the health policy highly relational to the changes and dynamics in the marketplace. Relational contracts, we can say, are contracts whose provisions are dynamic with respect to the environment in which they are executed. Some contracts are known as incomplete contracts because they contain terms that are implicit, rather than explicit. In the previous example, the dynamic nature of the product that is covered by the health insurance policy makes the policy “incomplete” and open to disputes. Fallen Celebrex rival, Vioxx, is a noted example. New Jersey–based Merck & Co., Inc., faces more than 7,000 lawsuits claiming that its blockbuster drug knowingly increased risk of heart attack and stroke. This chapter also delves into the structure of insurance contracts in general and insurance regulations as they all tie together. We will explore the following:

- Links

- Agency law, especially as applied to insurance

- Basic contractual requirements

- Important distinguishing characteristics of insurance contracts

Links

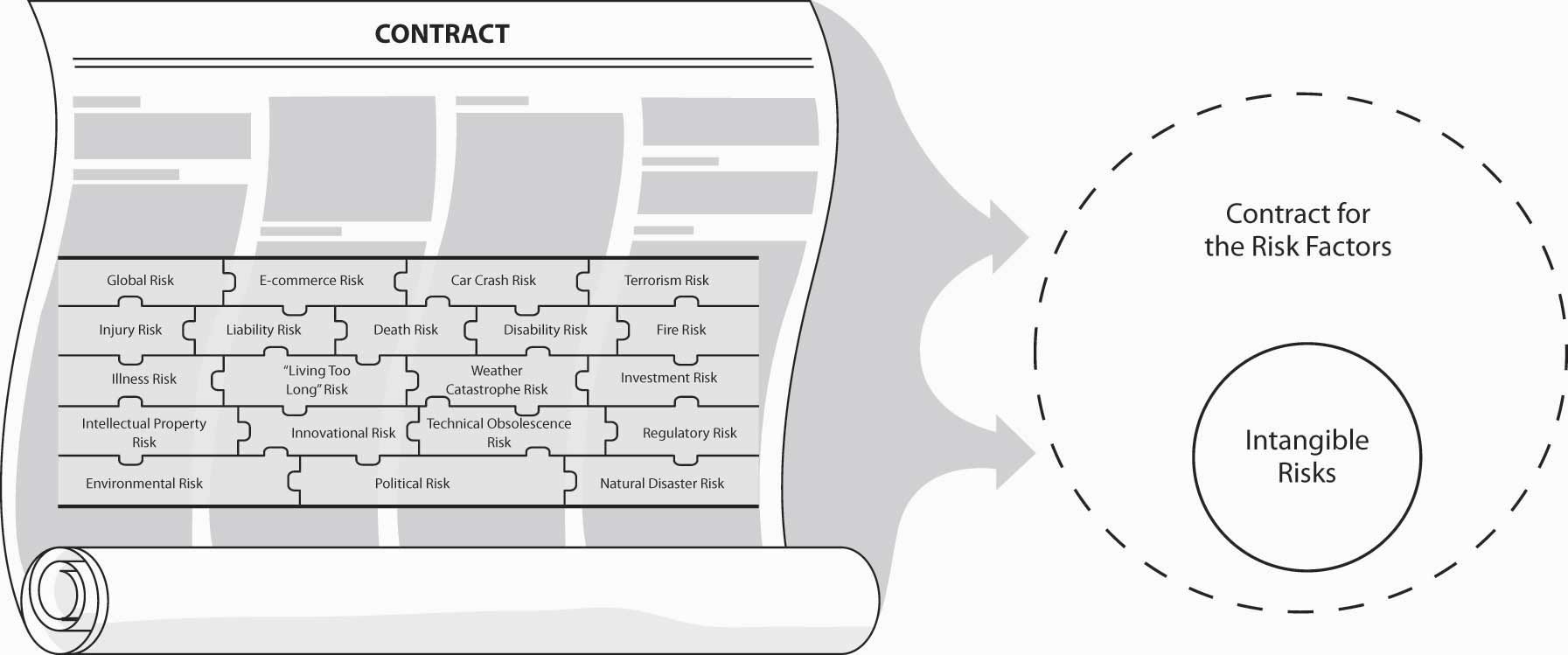

At this point in the text, we are still focused on broad subject matters that connect us to our holistic risk and risk management puzzle. We are not yet drilling down into specific topics such as homeowner’s insurance or automobile insurance. We are still in the big picture of understanding the importance of clarity in insurance contracts and the legal doctrines that influence those contracts, and the agents or brokers who deliver the contracts to us. If you think about the contracts like the layers of an onion that cover the core of the risk, you can apply your imagination to Figure \(\PageIndex{1}\).The idea of using Risk Balls occurred to me while searching for ways to apply transaction costs economic theory to insurance products. I began thinking about the risk embedded in insurance products as an intangible item separate from the contract that completes the exchange of that risk. The abstract notion of risk became the intangible core and the contract became the tangible part that wraps itself around the core or risk. We know now that each risk can be mitigated by various methods, as discussed in prior chapters. The important point here is that each activity is associated with legal doctrines culminating in the contracts themselves. The field of risk and insurance is intertwined with law and legal implications and regulation. No wonder the legal field is so connected to the insurance field as well as many pieces of legislation.

You, the student, will learn in this text that the field of insurance encompasses many roles and careers, including legal ones. As the nature of the contract, described above, becomes more incomplete (less clear or explicit), more legal battles are fought. These legal battles are not limited to disputes between insurers and insureds. In many cases, the agents or brokers are also involved. This point is emphasized in relation to the dispute over the final settlement regarding the World Trade Center (WTC) catastrophe of September 11, 2001.This issue was discussed at length in all financial magazines and newspapers since September 11, 2001. The case at hand was whether the collapse of the two towers should be counted as one insured event (because the damage was caused by a united group of terrorists) or two insured events (because the damage was caused by two separate planes some fifteen minutes apart). Why is this distinction important? Because Swiss Re, one of the principal reinsurers of the World Trade Center, is obligated to pay damages up to $3.5 billion per insured event. The root of the dispute involves explicit versus incomplete contracts, as described above. The leaseholder, Silverstein Properties, claimed that the broker, Willis Group Holdings, Ltd., promised a final contract that would interpret the attack as two events. The insurer, Swiss Re, maintained that it and Willis had agreed to a type of policy that would explicitly define the attack as one event. Willis was caught in the middle and, as you remember, brokers represent the insured. Therefore, a federal judge had to choose an appropriate way to handle the case. The final outcome was that for some insurers, the event was to be counted as two events.The December 9, 2004, BestWire article, “Tale of Two Trials: Contract Language Underlies Contradictory World Trade Center Verdicts,” explains that “the seemingly contradictory jury verdicts from two trials as to whether the Sept. 11, 2001, destruction of the World Trade Center was one event or two for insurance purposes is not so surprising when the central question in both trials is considered: Did the language in the insurance agreements adequately define what an occurrence is?” www3.ambest.com/Frames/FrameServer.asp?AltSrc =23&Tab=1&Site=news&refnum=70605 (accessed March 7, 2009). This story is only one of many illustrations of the complexities of relationships and the legal doctrines that are so important in insurance transactions.