8.1: Introduction

- Page ID

- 24514

The insurance industry, in fact, is one of the largest global financial industries, helping to propel the global economy. “In 2007, world insurance premium volume, for [property/casualty and life/health] combined, totaled $4.06 trillion, up 10.5 percent from $3.67 trillion in 2006,” according to international reinsurer Swiss Re. The United States led the world in total insurance premiums, as shown in Table 8.1.

| Total Premiums | ||||||

|---|---|---|---|---|---|---|

| Rank | Country | Nonlife PremiumsIncludes accident and health insurance. | Life Premiums | Amount | Percentage Change from Prior Year | Percentage of Total World Premiums |

| 1 | United StatesNonlife premiums include state funds; life premiums include an estimate of group pension business. | $578,357 | $651,311 | $1,229,668 | 4.69% | 30.28% |

| 2 | United Kingdom | 349,740 | 113,946 | 463,686 | 28.16 | 11.42 |

| 3 | JapanApril 1, 2007–March 31, 2008. | 330,651 | 94,182 | 424,832 | −3.31 | 10.46 |

| 4 | France | 186,993 | 81,907 | 268,900 | 7.47 | 6.62 |

| 5 | Germany | 102,419 | 120,407 | 222,825 | 10.09 | 5.49 |

| 6 | Italy | 88,215 | 54,112 | 142,328 | 1.27 | 3.50 |

| 7 | South KoreaApril 1, 2007–March 31, 2008. | 81,298 | 35,692 | 116,990 | 16.28 | 2.88 |

| 8 | The Netherlands | 35,998 | 66,834 | 102,831 | 11.98 | 2.53 |

| 9 | CanadaLife business expressed in net premiums. | 45,593 | 54,805 | 100,398 | 14.74 | 2.47 |

| 10 | PR China | 58,677 | 33,810 | 92,487 | 30.75 | 2.28 |

| * Before reinsurance transactions. | ||||||

Source: Insurance Information Institute (III), accessed March 6, 2009, www.iii.org/media/facts/statsbyissue/international/.

The large size of the global insurance markets is demonstrated by the written premiums shown in Table 8.1. The institutions making the market were described in "6:The Insurance Solution and Institutions". In this chapter we cover the following:

- Links

- Markets conditions: underwriting cycles, availability and affordability, insurance and reinsurance markets

- Regulation of insurance

Links

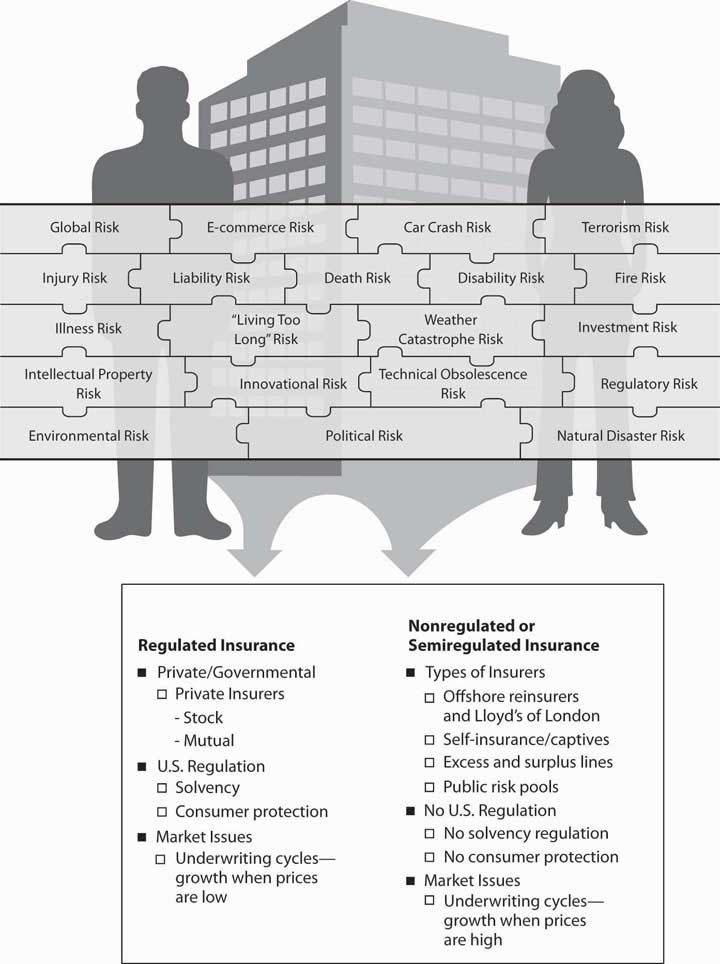

As we have done in the prior chapters, we begin with connecting the importance of this chapter to the complete picture of holistic risk management. We will become savvy consumers only when we understand the insurance marketplace and the conditions under which insurance institutions operate. When we make the selection of an insurer, we need to understand not only the organizational structure of that insurance firm, but we also need to be able to benefit from the regulatory safety net available to protect us. Also important is our clear understanding of insurance market conditions affecting the products and their pricing. Major rate increases for coverage do not happen in a vacuum. As you saw in "4: Evolving Risk Management - Fundamental Tools", past losses are the most important factor in setting rates. Market conditions, availability, and affordability of products are very important factors in the risk management decision, as you saw in "3: Risk Attitudes - Expected Utility Theory and Demand for Hedging". In "2: Risk Measurement and Metrics", you learned that an insurable risk must have the characteristic of being affordable. Because of underwriting cycles—the movement of insurance prices through time (explained next in this chapter)—insurance rates are considered dynamic. In a hard market, when rates are high and insurance capacity, the quantity of coverage that is available in terms of limits of coverage, is low, we may choose to self-insure. Insurance capacity relates to the level of insurers’ capital (net worth). If capital levels are low, insurers cannot provide a lot of coverage. In a soft market, when insurance capacity is high, we may select to insure for the same level of severity and frequency of losses. So our decisions are truly related to external market conditions, as indicated in "3: Risk Attitudes - Expected Utility Theory and Demand for Hedging".

The regulatory oversight of insurers is another important issue in our strategy. If we care to have a safety net of guarantee funds, which act as deposit insurance in case of insolvency of an insurer, we will work with a regulated insurer. In case of insolvency, a portion of the claims will be paid by the guarantee funds. We also need to understand the benefits of selecting a regulated entity as opposed to nonregulated one for other consumer protection actions such as the resolution of complaints. If we are unhappy with our insurer’s claims settlement process and if the insurer is under the state’s regulatory jurisdiction, the regulator in our state may help us resolve disputes.

As you can see, understanding insurance institutions, markets, and insurance regulation are critical to our ability to complete the picture of holistic risk management. Figure \(\PageIndex{1}\) provides the line of connection between our holistic risk picture (or a business holistic risk) and the big picture of the insurance industry and markets. Figure \(\PageIndex{1}\) separates the industry’s institutions into those that are government-regulated and those that are non- or semiregulated. Regardless of regulation, insurers are subject to market conditions and are structured along the same lines as any corporation. However, some insurance structures, such as governmental risk pools or Lloyd’s of London, do have a specialized organizational structure.