1.2: How We Pay for the Public Sector

- Page ID

- 9066

Managers need to know where public money comes from, and where it goes. That information can answer important questions like:

- What revenue options are available to governments? Non-profits?

- What are the advantages and disadvantages of various revenue sources with respect to efficiency, equity, fairness, and other goals?

- How will the US federal government’s financial challenges shape the financial future of state governments, local governments, non-profits, and other public organizations?

- What is the optimal “capital structure” for a non-profit?

- How, if at all, can governments address the challenges of entitlements and legacy costs?

In January of 2010 the United States Department of Justice (DOJ) received a formal civil rights complaint from a local community organization in the City of Ferguson, MO. In their complaint they accused the Ferguson Police Department of aggressive and biased policing tactics, including large numbers of traffic stops, searches, seizures, and arrests in the city’s African-American communities. DOJ officials corroborated the report with the Missouri Attorney General’s office, who had also received several similar complaints throughout the previous five years. Both offices agreed to monitor the situation.

On August 9, 2014, Michael Brown, a teenager and resident of Ferguson, was shot and killed by a Ferguson police officer who was investigating a nearby robbery. Ferguson police officials drew sharp criticism for the incident and for their management of the subsequent investigation into potential police misconduct. Several weeks later a grand jury later declined to indict the police officer. In their view the evidence suggested the police officer had reason enough to consider Brown a potentially dangerous suspect.

The shooting sparked violent protests across the US. Ferguson residents said the shooting was just the most recent example of the racist policing they had pointed out to federal and state officials years earlier. They implored Attorney General Eric Holder to immediately open a DOJ civil rights investigation into the Ferguson Police Department. Holder said his office would gather as much information as possible, but cautioned everyone that anecdotes and demographics are not sufficient to prove an accusation of biased policing. For several weeks, the country anxiously awaited word on what DOJ would do next.

On September 20, 2014 DOJ opened a formal civil rights investigation. The report from that investigation was released in March 2015. It excoriated the Ferguson Police Department and the Ferguson City Council for encouraging, both actively and passively, the sort of aggressive policing that Ferguson residents had decried. But perhaps even more important, it explained that the most compelling evidence of biased policing was not arrest records or police reports. It was Ferguson’s budget. The report said “Ferguson’s law enforcement practices are shaped by the City’s focus on revenue rather than on public safety needs.” It documented a recent trend toward raising new city revenues through aggressive enforcement of fines and fees. Ferguson generated more than $2.5 million in municipal court revenue in fiscal year 2013, an 80 percent increase from only two years prior. In all, fines and forfeitures comprised 20 percent of the city’s operating revenue in fiscal year 2013, up from about 13 percent in 2011. By comparison, other St. Louis suburbs relied on fines and fees for no more than six percent of operating revenue. This budget strategy legitimized and even encouraged Ferguson’s law enforcement and court officials, most of whom were not racists, to pursue such aggressive policing against Ferguson’s majority African-American community.

The take away here is clear: Where a public organization gets its money says a lot about its priorities. In Ferguson’s case, choices about where to get revenue led to a nationwide social movement.

After reading this chapter you should be able to:

- Identify the revenue sources used by the federal, state, and local governments.

- Contrast government revenue sources with non-profit revenue sources like donations and earned income.

- Identify public organizations’ main spending areas, and the division of that spending across the government, non-profit, and for-profit sector.

- Show how similar governments pay for similar services in quite different ways.

- Identify some of the “macro-challenges” that will shape public organizations’ finances well into the future.

Governments across the United States do the same basic things. Cities and towns mostly maintain roads, plow snow, keep neighborhoods safe, prevent and fight fires, and educate children. County governments run elections, care for the mentally ill, and prevent infectious diseases. State governments coordinate health care for the poor, incarcerate prisoners, and operate universities. The national – or “federal” – government regulates trade and commerce, defends our borders, and pays for health care for the elderly.

At the same time, governments are remarkably dis-similar in how they pay for and deliver these services. Some rely on a single tax source for most or all of their revenue. Others draw on many different revenue sources. Some deliver their services with the help of non-profits, health care organizations, private sector contractors, and other stakeholders. Others engage outside entities infrequently, if at all. Some citizens want their government to deliver many different high-quality services. Others want their government to do as little as possible.

These choices, about how governments pay for their services, how much they provide, and how they ultimately deliver those services, matter a lot to citizens. For instance, if a city government depends mostly on property taxes, its leaders might have an incentive to emphasize services that benefit property owners, such as public safety and sidewalks, and to worry less about services more likely to benefit those who do not own property, like public parks or housing the homeless. In some regions governments pay non-profit organizations to deliver most or all of the basic services in areas like foster care, child immunizations, and assisted living for seniors. For those who use those services, the quality of service they receive can depend a lot on which non-profit manages their case.

So at a high level, governments look the same. But if we examine them more carefully, we see they vary a lot on where their money comes from, and where it goes. That variation, and its implications for citizens, is a key part of the study of public finance. This chapter is a basic overview of where governments get their money, where they spend it, and some of the financial challenges they’re likely to face in the future.

The Federal Government

The national government – also known as the “federal government” – is one of the largest and most important employers in the United States. Every soldier in the military, customs agent at an airport, and astronaut at NASA (the “National Aeronautics and Space Administration”) works for the federal government. And so do many, many others. In 2015 the federal government spent just under $4 trillion and employed an estimated five million people, both directly and as contractors. For the past decade or so, federal government spending has accounted for roughly one-quarter of the entire economic output of the US.

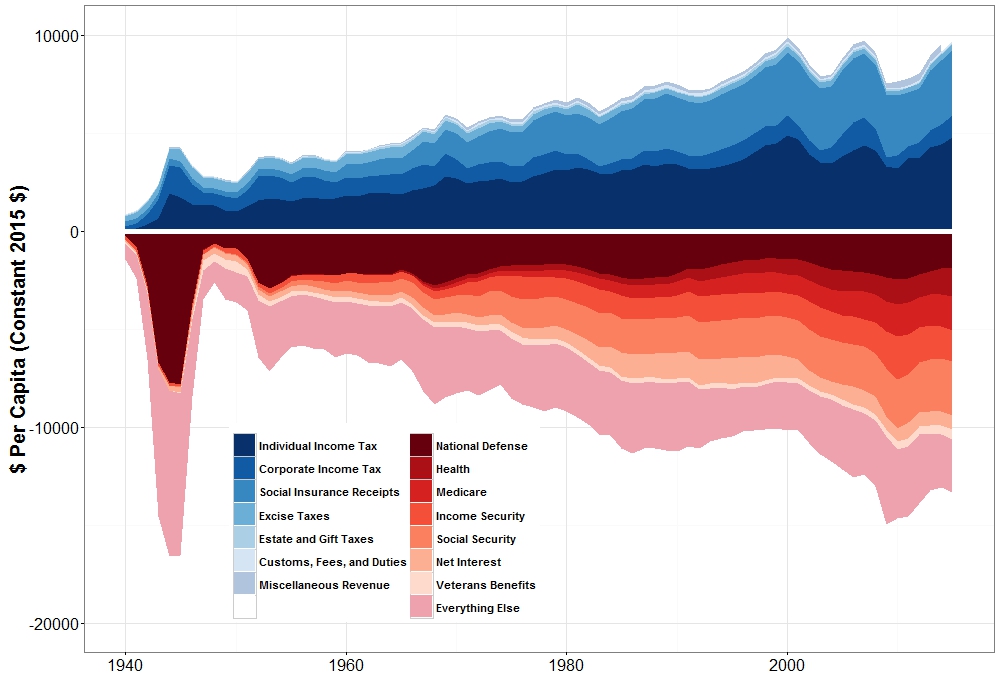

The chart below shows where the federal government has received and spent its money since just before World War II. Areas shaded blue represent revenue, or money that comes into the government. Areas shaded red are spending items. Spending is called many different things in public finance, including expenses, expenditures, and outlays. These different labels have slightly different meanings that you’ll learn throughout this text. All the figures shown here are in per capita constant 2015 dollars. In other words, they’ve been adjusted for inflation, and they’re expressed as an amount for every person in the US.

Roughly 80% of the federal government’s revenue is from two sources: the individual income tax and social insurance receipts.[1]

- In 2015 the federal government collected just over $3,500 per capita from individual income taxes. The income tax an individual pays is determined by their taxable, tax rate, and any applicable tax preferences. Taxable income is an individual’s income minus any tax preferences. The federal government offers a standard exemption, or a reduction of an individual’s taxable income, that all taxpayers can claim. Beyond that standard deduction, eligible taxpayers can claim hundreds of other exemptions and other tax benefits related to home ownership, retirement savings, health insurance, investments in equipment and technology, and dozens of other areas. Why does the federal government offer these preferences? To encourage taxpayers to save for retirement, buy a home, invest in a business, or participate in many other types of economic activity. Whether tax preferences actually encourage those behaviors is the subject of substantial debate and analysis (see the discussion later on tax efficiency and market distortions). The tax rate is the amount of tax paid per dollar of taxable income. In 2015 the federal tax code had seven different rates that applied across levels of taxable income (also known as “tax brackets”). Those statutory rates ranged from a 10% on individual annual income up to $9,225, to 39.6% on annual income over $413,201. An individual’s effective tax rate is their tax liability divided by their taxable income. If an individual claims a variety of tax preferences, their effective tax rate might be much lower than the statutory tax rate listed here.

- Social insurance receipts are taxes levied on individuals’ wages. Employers take these taxes out of workers’ wages and send them to the federal government on their behalf. That’s why they’re often called payroll taxes or withholding taxes. Social insurance receipts are the main funding source for social insurance programs like Social Security and Medicare (see below).

- The remaining 20% or so of federal revenue is from a variety of sources including the corporate income tax (taxes on business income, rather than individual income), excise taxes (taxes on the purchase of specific goods like gasoline, cigarettes, airline tickets, etc.), and estate taxes (a tax imposed when a family’s wealth is transferred from one generation to the next). As shown in the figure, these revenues as a share of total revenues have not changed much in the past several decades.

Tax preferences – sometimes called tax expenditures – are provisions in tax law that allow preferential treatment for certain taxpayers. They include credits, waivers, exemptions, deductions, differential rates, and anything else to reduce a person’s or business’ tax liability. Many are quite specific. For example, some states have reduced tax rates that apply only to particular employers, industries, or geographic areas. Tax expenditures are, in effect, a form of spending. They require the government to collect less revenue than it would otherwise collect. Some think they’re unfair because they offer targeted benefits but without the transparency of the traditional budget process. Proponents say that despite these drawbacks, tax preferences are essential to promote important behaviors, like buying a home or starting a business. At the state and local level they’re an especially important tool to attract and retain businesses in today’s competitive economic development environment.

Federal government spending is divided roughly equally across six main areas:

- National defense includes pay and benefits for all members of the US Army, Navy, Air Force, and Marines, and all civilian support services. It also includes capital outlays – or spending on items with long useful lives – for military bases, planes, tanks, and other military hardware. Note the large spike in national defense spending during World War II (1939-1945) and the Korean War (1950-1953).

- Medicare is the federal government’s health insurance program for the elderly. It was established in 1965. By some estimates, Medicare paid for nearly one-quarter of all the health care delivered in the US, a total of nearly $750 billion in 2015. Medicare has three main components. “Part A” pays for hospital stays, surgery, and other medical procedures that require admission to a hospital. “Part B” covers supplementary medical services like physician visits and procedures that do not require hospital admission. “Part D” pays for prescription drugs. Part A is funded through payroll taxes and through premiums paid by individual beneficiaries. Part B and Part D are funded mostly through payroll taxes. Medicare does not employ physicians or other health care providers. It is, in effect, a health insurance company funded by the federal government. In 2015 it served more than 55 million beneficiaries and spent an average of $18,500 per beneficiary.

- Health is a broad category that covers health-related spending outside of Medicare. The largest segment of this spending is the federal government’s contribution to state Medicaid programs. It includes funding for public health and population health agencies like the National Institutes of Health (NIH) and the Centers for Disease Control and Prevention, and for health-focused regulatory agencies like the Food and Drug Administration.

- Social Security is an income assistance program for retirees. In 2015, over 59 million Americans received nearly $900 billion in Social Security benefits. Social Security is simple. Individuals contribute payroll taxes while they are working, those taxes are deposited into a fund, and when they retire, they are paid from that fund. In 2015, the average Social Security benefit was around $1,300 per month. Social Security also distributes benefits to disabled individuals who are not able to work.

- Income security is cash and cash-like assistance programs outside of Social Security. Most of these programs help individuals pay for specific, basic necessities. It includes unemployment insurance, food stamps, foster care etc.

- The federal government borrows a lot of money. Some of that borrowing is to pay for “big ticket” or capital outlays like aircraft carriers or refurbishing national parks. Like most consumers, the federal government does not have the money “saved up” to purchase these items, so it borrows money and pays it back over time. It also borrows when revenue collections fall short of spending needs. This is known as deficit spending. The federal government borrows money by issuing three types of Treasury Obligations: Treasury bills, Treasury notes, and Treasury bonds. Much like loans, obligations are bought by investors and the government agrees to pay them back, with interest, over time. Treasury bills come due – i.e. they have a maturity – of three months to one year. Treasury notes have maturities of two years to ten years. Treasury bonds mature in ten years upto 30 years. Each year the government pays the annual portion of the interest it owes on its Treasury obligations, and that payment is known as net interest.

- “Everything Else” is just as it sounds. This includes federal government programs for transportation, student loans, affordable housing, the arts and humanities, and thousands of other programs.

At the end of 2015, the US Treasury had $19 trillion of outstanding Treasury bonds. About $12 trillion is owned by US investors. The remaining $7 trillion are held by investors outside the US, including nearly $1.5 trillion in China, and just over $1 trillion in Japan. The remaining $3.8 trillion is held by nearly 100 other countries. Why are US Treasury bonds so attractive to foreign investors? Because the US government is seen as the safest investment in the world. Investors across the globe believe the US government will pay back those bonds, with interest, no matter what.

We often divide federal government spending into two categories: discretionary spending and non-discretionary or mandatory spending. Non-discretionary spending is controlled by law. Social Security is a good example. A person becomes eligible for “full” Social Security benefits once they are over age 65 and have paid payroll taxes for almost four years. Once they become eligible, the benefit they receive is determined by a formula that is linked to the total wages they earned during their last 35 years of working. That formula is written into the law that created Social Security. Once a person becomes eligible they are “entitled” to the benefits determined by that formula. Other federal programs like Medicare, food stamps, Supplemental Security Income, and many others follow a formula-based structure. If Congress and the President want to change how much is spent on these programs, they must change the relevant laws. By some estimates, non-discretionary spending is more than 65% of all federal spending. Add to that the roughly 7-8% for interest on the debt, and we see that nearly three-quarters of federal spending is “locked in.”

The remaining one-quarter is discretionary spending. This is spending that Congress and the President can adjust in the annual budget. It includes national defense, most of the “health” spending category, and virtually all of the “everything else” category. There is considerable debate on whether national defense is, in fact, discretionary spending. Legislators are not eager to cut funding to troops in harm’s way. So keep in mind that when Congress debates its annual budget, in effect, it’s debating about 10-25% of what it will eventually spend. The vast majority of federal spending is driven by laws, rules, and priorities that originate outside the budget.

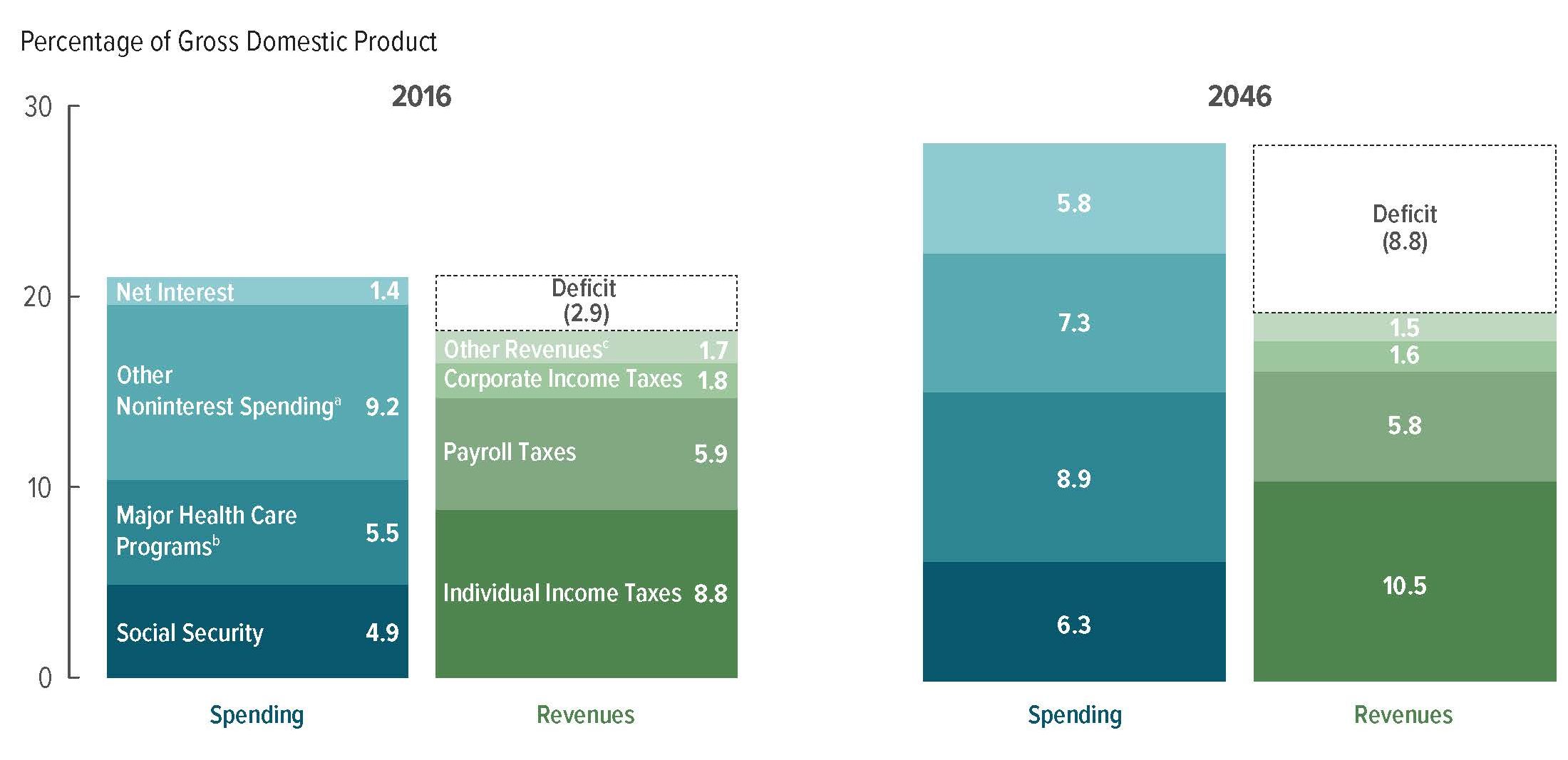

This discussion about entitlements raises another absolutely essential point: the Federal Government has a substantial structural deficit. A structural deficit is when a government’s long-term spending exceeds its long-term revenues. The figure below illustrates this point. It shows that in 2016, the federal government has a projected budget deficit of 2.9% of the US Gross Domestic Product (GDP; the county’s total economic output), or around $1.5 trillion. By the year 2046, assuming no major changes in spending or revenue policies, that annual budget deficit will grow to 8.8% of GDP. Why is the deficit expected to grow so quickly? In part because federal non-discretionary spending is going to grow. More and more of the “Baby Boomer” population will become eligible for Medicare, Social Security, and other programs. As the eligible population grows, so too will spending. Moreover, the cost of health care services has increased three to four times faster than all other costs across the economy. That’s why health-related non-discretionary spending is the proverbial “double whammy” – the number of people who need those services will increase, and so will the rate of spending per person to deliver those services. At the same time, most economists are projecting slower economic growth for the next several decades. Given the federal government’s current revenue policies, that will mean slower revenue growth over time. Those two main factors, growth in non-discretionary spending and slower revenue growth, will lead to much larger deficits over time.

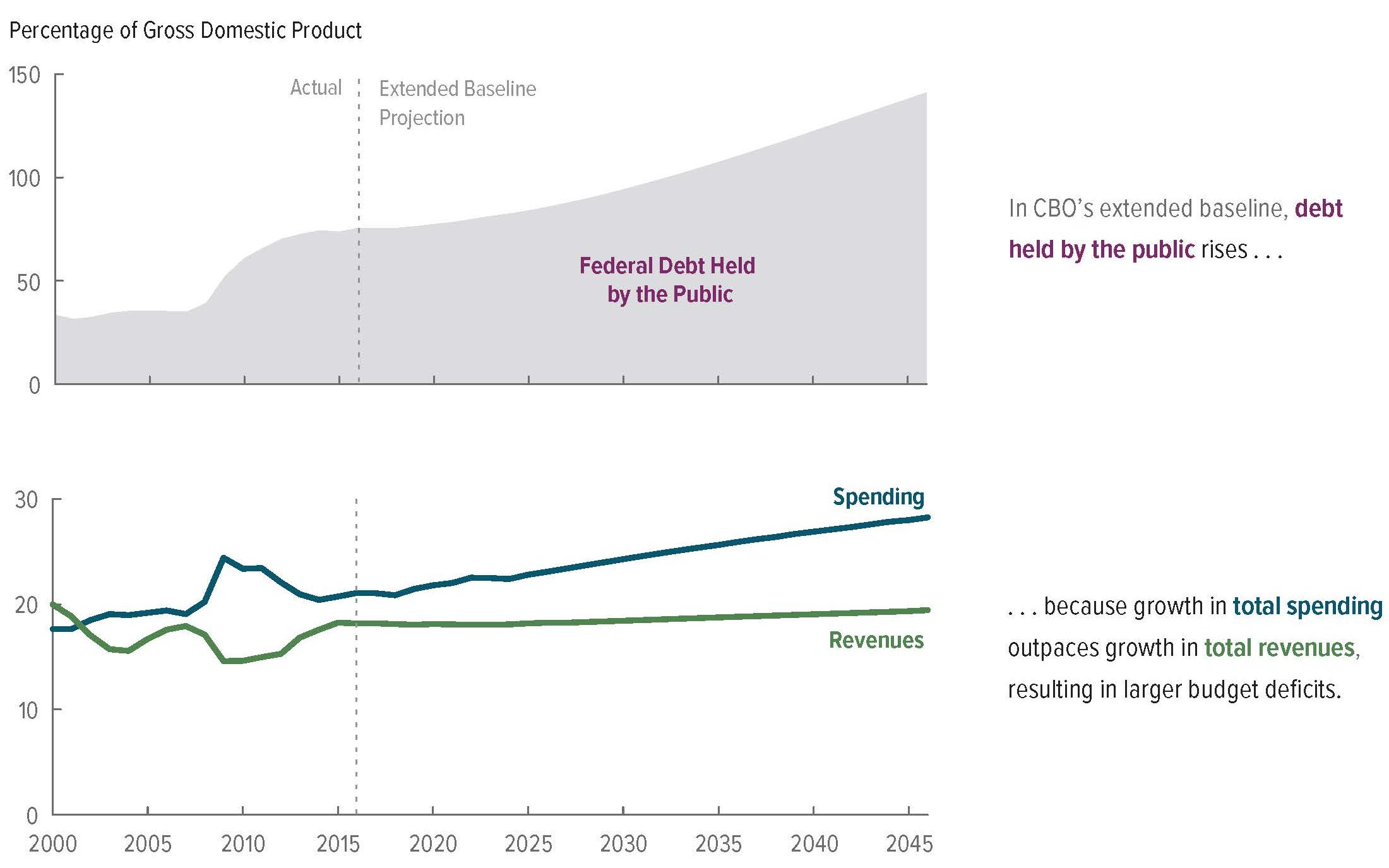

You’re probably asking yourself how will the federal government finance those deficits? If it does not collect enough revenue to cover its spending needs, it will borrow. The figure below shows how the federal government’s debt will increase in response. In 2016, federal government debt was around 72% of GDP. The Congressional Budget Office estimates it will grow to just under 150% of GDP by 2046. For context, consider that in 2015 Greece, long considered the “fiscal problem child” of the European Union, had a debt-to-GDP ratio of 158%.

This rapid growth in debt is concerning for many reasons. First, federal government borrowing “crowds out” borrowing by small businesses, homeowners, state and local governments, and others who need to borrow to invest in their own projects. Since there are only so many investors with money to invest, if the federal government takes a larger share of that money, there’s less for everyone else. Many economists and finance experts have also warned that if the federal government’s debt grows too high, then investors might be less willing to loan it money in the future. If investors are less willing to loan the government money, the government must offer higher interest rates to increase investors’ return on investment. As the federal government’s interest rates rise, interest rates rise for everyone else. Occasional increases to interest rates are not necessarily a bad thing, but prolonged high interest rates mean less investment by people and business, and that leads to lower productivity and slower economic growth.

The federal government’s structural deficit is the single most important trend in public budgeting and finance today. Without major changes in federal government policy, especially in areas like Medicare and Social Security, the federal government will have no choice but to run enormous deficits and cut non-discretionary spending. Those cuts will mean less money for many of the key programs that you probably care about the most: basic scientific research, student loans, highways, transit systems, national parks, and every other discretionary program. In fact, some cynics have said that in the future, “the federal government will be an army with a health care system.” State and local governments will be forced to take on many of the services the federal government used to provide in areas like affordable housing, environmental protection, international trade promotion etc. At the same time, some optimists say this is a welcome change. Without the rigidity and uniformity of the federal government, local communities will have the latitude and flexibility to experiment with new approaches to social problems. What’s not debatable is that absent major changes in policy, especially for non-discretionary spending, federal government spending will look quite different in the not-too-distant future.

Interest rates are one of the most important numbers in public budgeting and finance. Interest is what it costs to use someone else’s money. Banks and other financial institutions lend consumers and governments money at “market interest rates” like the annual percentage rate (APR). Small changes in interest rates can mean big differences in the cost to deliver public projects. That’s why it behooves public managers to know what drives interest rates.

Interest rates fluctuate for a variety of macroeconomic reasons. If inflation is on the rise, then businesses will be less willing to spend money on new buildings, equipment, and other capital investments. If demand for capital investments is down, then so is demand for borrowed money to finance those investments. In those market conditions banks and other financial institutions will lower the interest rates they offer on loans to entice businesses to make those investments. The opposite is also true. Businesses will seek to invest during periods of low inflation, and that drives up demand for borrowed money, and that drives interest rates up. Government borrowing and capital investment can also drive demand for borrowed money. Macroeconomists have complex models that explain and predict these interrelationships between consumer spending, investments, and government spending.

The Federal Reserve Bank of the US – i.e. “The Fed” – is also a crucial and closely-watched player. The Fed is the central bank. It lends money to banks and holds deposits from banks throughout the US. Its mission is to fight inflation and keep unemployment to a minimum. In finance circles, this is called the Dual Mandate.

The Fed has many tools to achieve that mission, and most of those tools involve interest rates. It can raise or lower the Federal Funds Rate, or the interest rates at which banks lend money to each other. It can demand that banks keep more money on deposit at the Fed. Increases in either will reduce the amount of money banks have available to lend, and that drives up interest rates. It’s most powerful tool is called open market operations (OMO). If the Fed wishes to lower interest rates it buys short-term Treasury bonds and other financial securities from investors. This increases the money available for lending and reduces interest rates. When it wishes to raise rates it sells securities to banks. When banks buy those securities they have less money available to lend, and that increases interest rates.

State Governments

There’s an old adage that state governments are in charge of “medication, education, and incarceration.” That saying is both pithy and true. In 2015 state governments spent $1.6 trillion, and most of it was spent on schools, Medicaid, and corrections. That said, they vary a lot in how much of those services they deliver, and how they pay for those services. In some regions, the state is one of the largest employers. This is especially true in rural areas with state universities or state prisons. In other regions state government has a limited presence.

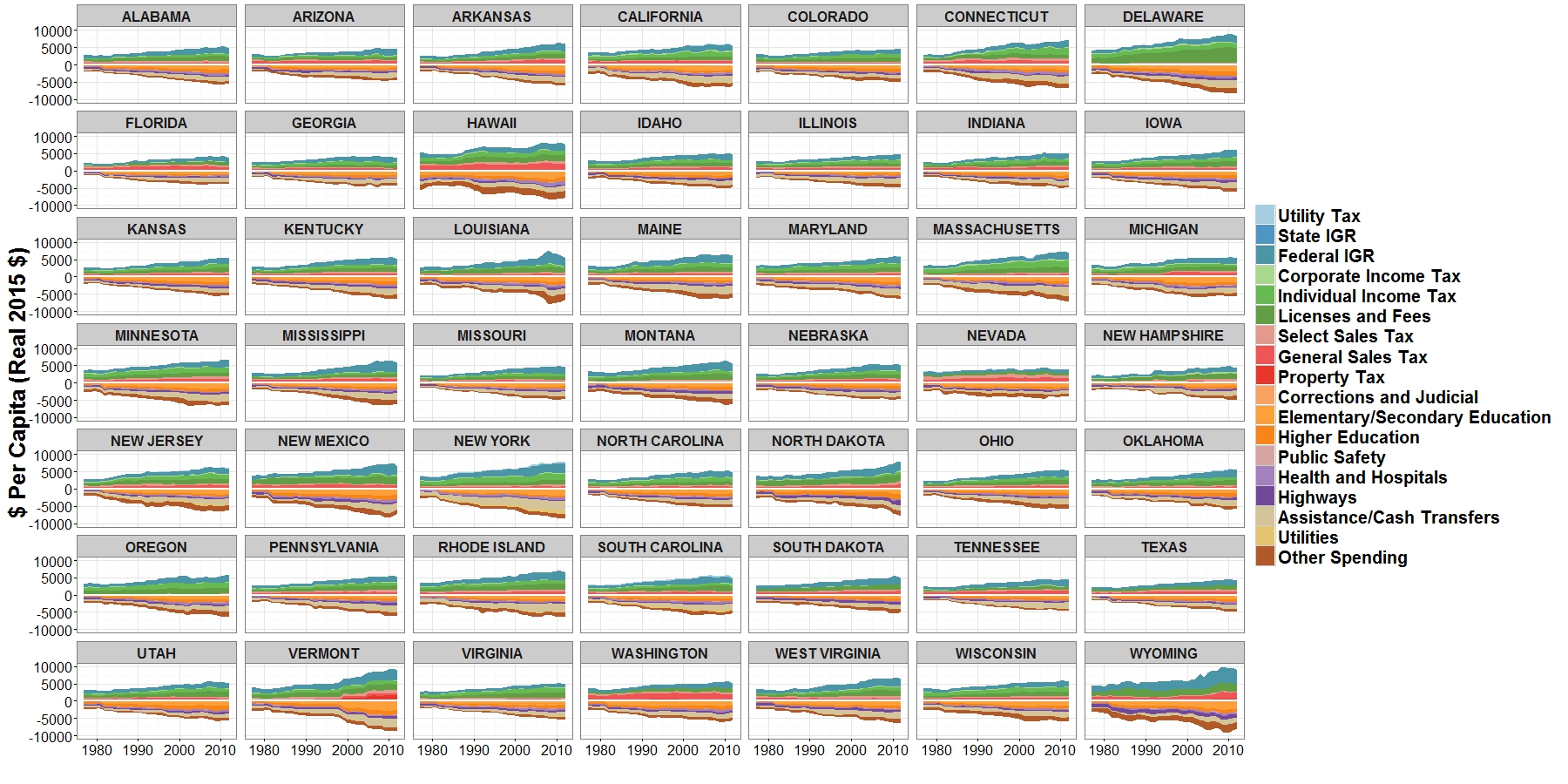

The figure below shows the trends in state government revenues and spending since the late 1970s. All the shaded areas above 0 are revenues, and all the area below 0 is spending. All figures are expressed in 2015 per capita dollars.

Three trends stand out from this chart. First, the size and scope of state governments varies a lot. Today Nevada, for example, spends just under $5,000 per capita. On a per capita basis it’s one of the smallest state governments. Vermont, by contrast, spends more than $9,000. Both states have roughly the same population, but one state’s government spends almost twice as much per capita. There are several reasons for this. One is that much of Nevada’s land is managed by the federal Department of Interior and by Native American Tribes. Those governments deliver many of the basic services that state governments deliver in other states. Citizens in Nevada have also historically preferred less government overall. In Vermont, the state government is largely responsible for roads, public health, primary and secondary education, and many other services that local governments deliver in most other states. That’s why state government spending in Vermont is roughly equivalent to state government spending plus total local government spending in most other states.

A second key trend is that overall state spending grew substantially over the past few decades. In 1977, the average state per capita spending was around $2,800. In 2012 it was $5,100. Revenues have grown on a similar trajectory. But note that growth was not uniform. Spending in states like Arizona, California, Colorado, and Washington grew far slower than the average. This is not a coincidence. These states have passed strict laws, broadly known as tax and expenditure limitations, that restrict how quickly their revenues and spending can grow. States without those limits, like Connecticut, Delaware, New York, and Massachusetts, have seen much faster growth in both revenues and spending. North Dakota, Wyoming, and New Mexico saw large jumps in revenues and spending in the past decade or so, due mostly to growth of their respective shale oil industries (more commonly known as fracking).

Tax and expenditure limits (or TELs) restrict the growth of government revenues or spending. While there are no two TELs that are alike, they all share key elements. At the state-level, TELs are either dollar limits on tax revenues or procedural limits that mandate either voter approval or a legislative super-majority vote for new or higher taxes. In estimating the dollar limits, the state is required to establish base year revenues or appropriations subject to the limit and adjust for a factor of growth that is equal to changes in population, inflation, or personal income. States can only exceed the TEL revenue or appropriation caps if they exercise their override provision (e.g., legislative majority or super-majority vote). Funds in excess of the limitation are refunded to taxpayers, deposited in a reserve fund (commonly referred to as a rainy day fund), or used for purposes as provided by law (e.g., capital improvements, K-12 spending). Procedural limits are unique in that they are not part of the budgeting processes and apply only if the Governor seeks to levy new or higher taxes.

At the local level, TELs are either a limit on property tax rates, the taxable base (or assessed value of taxable property), property tax levy, or on the aggregate of local government taxing or spending authority. The limits on tax rates apply to either all municipal governments (an overall property tax rate limit) or specific municipalities (e.g., city, county, or a school district). Limits on assessed valuation are limits on annual growth in the valuation of property (e.g., 2 percent) while limits on property tax revenues are dollar limits on the total amount of revenue that can be raised from the property tax. Caps on the aggregate of local government taxing or spending authority are dollar limits on overall spending authority.

While these revenue suppression measures remain popular, they have had unintended and perhaps detrimental effects, especially at the local level. For example, data from 1977 through 2007 shows the precipitous decline in property tax revenues as a share of own-source revenues. In California, Massachusetts, and Oregon, revenues from the property tax revenues fell more than 15 percent. In response, local governments have come to rely more on intergovernmental transfers and user charges and fees. They have also adopted local-option sales and/or income taxes to make up for lost property tax revenues. As a result of changes, revenues are more volatile and local governments have less control over their budgets than they did prior to the tax-revolt movement. TELs have also altered how local governments are willing to borrow, market perceptions of their credit quality (or default risk), and their ability to manage their other long-term obligations and legacy costs.

A third important trend is that state revenues roughly equal state spending. Virtually every state’s constitution requires that its legislature and governor pass a balanced budget. As you’ll see later, “balanced budget” can mean rather different things in different places. But overall, states don’t spend more money than they collect. This is in sharp contrast to the federal government. As you saw above, throughout the past several decades the federal government’s spending has routinely exceeded its revenues. Unlike the federal government, the states cannot borrow money to finance budget deficit. In a number of states, restrictions on deficit spending are enshrined in law.

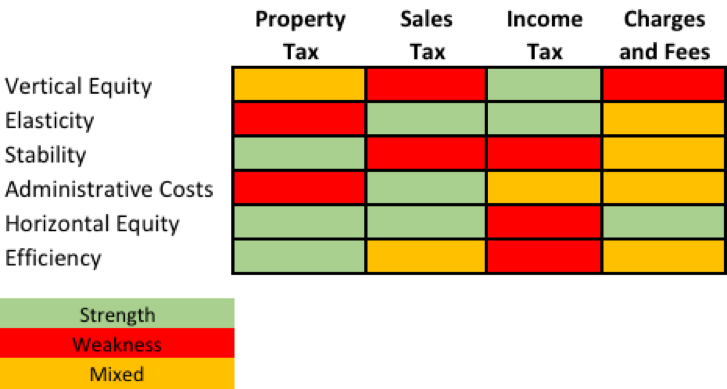

Governments tax many different types of activity with many different types of revenue instruments (i.e. taxes, fees, charges, etc.). Each instrument is fair in some ways, but less fair in other ways. In public finance we typically define fairness along several dimensions:

- Efficiency. Basic economics tells us that if a good or service is taxed, then consumers will purchase or produce less of it. An efficient tax minimizes these market distortions. For instance, most tax experts agree the corporate income tax is one of the least efficient. Most large corporations are willing and able to move to the state or country where they face the lowest possible corporate income tax burden. When they move they take jobs, capital investments, and tax revenue with them. Property taxes, by contrast, are one of the most efficient. The quantity of land available for purchase is fixed, so taxing it cannot distort supply the same way that taxing income might discourage work, or that taxing investment might encourage near-term consumption.

- Vertical Equity. Vertical equity means the amount of tax someone pays increases with their ability to pay. Most income tax systems impose higher tax rates on individuals and businesses with higher incomes. This is meant to ensure taxpayers who have greater ability to pay will contribute a higher share of their income through taxes. A tax with a high degree of vertical equity, like the income tax, is known as a progressive tax. A regressive tax is a tax where those who have less ability to pay ultimately pay a higher share of their income in taxes.

- Horizontal Equity. Horizontal equity – sometimes called “tax neutrality” – means that people with similar ability to pay contribute a similar amount of taxes. The property tax is a good example of a tax that promotes horizontal equity. With a properly administered property tax system, homeowners or business owners with similar properties will pay similar amounts of property taxes. Income taxes are quite different. Because of tax preferences, it’s entirely possible for two people with the same income to pay very different amounts of income tax.Elasticity. An elastic tax responds quickly to changes in the broader economy. If the economy is growing and consumers are spending money, collections of elastic taxes increase and overall revenue grows. This is quite attractive to policymakers. With elastic taxes, they can see growth in tax collections without increasing the tax rate. Of course, the opposite is also true. If the economy is in recession, consumer spending decreases, and so do revenue collections. Sales taxes and income taxes are the most elastic revenues.

- Stability. A stable – or “inelastic” – tax does not respond quickly to changes in the economy. Property taxes are among the most inelastic taxes. Property values don’t typically fluctuate as much as prices of other goods, so property tax collections don’t increase or decrease nearly as fast as sales or income taxes. They’re more predictable, but they can only grow so fast.

- Administrative Costs. Some taxes require a lot of time and resources to administer. Property taxes are a good example. Tax assessors go to great lengths to make certain the appraised value they assign to a home or business is as close as possible to its actual market value. To do this they perform a lot of spatial analysis. That analysis demands time and expertise.

The chart below illustrates a basic fact about taxation: all taxes come with trade-offs. For instance, the property tax is stable and promotes horizontal equity, but it’s costly to administer and generally non-responsive to broader trends in the economy. The sales tax is cheap to administer and produces more revenue during good economic times, but it’s also quite regressive. Also note that for many of these instruments the evidence is mixed. That is, tax policy experts disagree on whether that characteristic is a strength or weakness for that particular revenue instrument.