19.1: Introduction

- Page ID

- 24591

Following Social Security as a foundation to managing the life cycle risks of old age, sickness, accidents, and death, we begin our expedition into the products that help in solving these risks. In this chapter we delve into the life insurance products and the life insurance industry as one separate from the property/casualty insurance industry. As you saw in "7: Insurance Operations", the accumulation of a reserve and the pricing of life insurance and annuities are based on mortality tables and life expectancy tables. The health insurance products use morbidity tables and loss data for calculating health and disability rates. In this chapter we will learn about the different life insurance products available—term life, whole life, universal life, variable life, and universal variable life products. The way these products fit into the risk management portfolio of the Smith family is featured in Case 1 of "23: Cases in Holistic Risk Management". This chapter concentrates on the life products themselves.

While mortality rates keep improving (as we discussed in "17: Life Cycle Financial Risks"), extreme health catastrophes can reverse the trend for brief periods. At various points in human history, mortality rates worsened as extreme health catastrophes occurred. For example, the mortality rate changed dramatically in 1918 when millions of people died from the flu pandemic. The potential for an avian flu pandemic in 2006 led to estimated life insurance claims of up to $133 billion under the most extreme scenario. The young and the elderly are those affected most by the flu. Because these age cohorts usually have less life insurance coverage, the general mortality impact may be even greater than the life claims estimates.Insurance Information Institute (III), “Moderate Avian Flu Pandemic Similar to 1957 and 1968 Outbreaks Could Cost U.S. Life Insurers $31 Billion in Additional Claims,” Press Release, January 17, 2006, www.iii.org/media/updates/press.748721/ (accessed April 10, 2009).

Life insurance can be thought of as a contract providing a hedge against an untimely death. When purchasing life insurance, the policyowner buys a contract for the future delivery of dollars. This also provides liquidity. The death, whenever it occurs, will create , such as funeral costs and debt payment, and estate taxes if the estate is large enough, that must be paid immediately. Most people, no matter how wealthy, will not have this much cash on hand. Life insurance provides the necessary liquidity because its payment is triggered by death. Smart decisions about life insurance require understanding both the nature of life insurance and the different types of products available. In this chapter we cover the most widely used products.

The topics covered in this chapter include the following:

- Links

- How life insurance works

- Life insurance products: term insurance, universal life, variable life, variable universal life, and current assumption whole life

- Taxation, major policy provisions, riders, and adjusting life insurance for inflation

- Group life insurance

Links

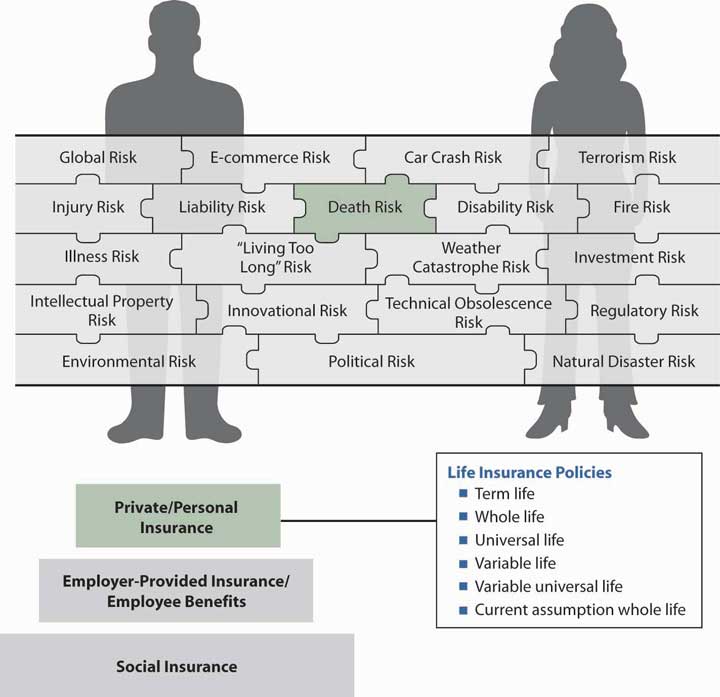

For our holistic risk management, we need to look at all sources of coverages available. Understanding each type of coverage will complete our ability to manage our risk. In this chapter we delve into the various types of life insurance coverage that are available in the market. Some focus on covering the risk of mortality alone, while others also offer a savings element along with covering the risk of dying. This means that at any point in time, there is a cash value to the policy. This savings element is critical to the choices we make among policies such as whole life, universal life, or universal variable life policies. Our savings with insurance companies, via life products or annuities, makes this industry one of the largest financial intermediaries globally. As explained in "7: Insurance Operations", the investment part of the operation of an insurer is as important as the underwriting part. Investments allow insurance companies to postprofits even when underwriting at a loss. In the life/health industry, investments are crucial to both financial performance and solvency. (Read how the industry is affected by poor investment returns in the box “The Life/Health Industry in the Economic Recession of 2008–2009” which appears later in this chapter.)

In this chapter, we drill down into the life insurance policies, but this is just a piece of the products puzzle that helps us complete the bigger picture of our risks. All of the steps of the three-step structure in Figure \(\PageIndex{1}\) include some elements of death benefits coverage. In this chapter we delve into the top step for the different types of individual life coverage. Figure \(\PageIndex{1}\) provides us with the connection between the life policies of this chapter and the holistic risk picture.