10.1: Introduction

- Page ID

- 24528

As discussed in "9: Fundamental Doctrines Affecting Insurance Contracts", an insurance policy is a contractual agreement subject to rules governing contracts. Understanding those rules is necessary for comprehending an insurance policy. It is not enough, however. We will be spending quite a bit of time in the following chapters discussing the specific provisions of various insurance contracts. These provisions add substance to the general rules of contracts already presented and should give you the skills needed to comprehend any policy.

In "10: Structure and Analysis of Insurance Contracts", we offer a general framework of insurance contracts, called policies. Because most policies are somewhat standardized, it is possible to present a framework applicable to almost all insurance contracts. As an analogy, think about grammar. In most cases, you can follow the rules almost implicitly, except when you have exceptions to the rules. Similarly, insurance policies follow comparable rules in most cases. Knowing the format and general content of insurance policies will help later in understanding the specific details of each type of coverage for each distinct risk. This chapter covers the following:

- Links

- Entering into the contract: applications, binders, and conditional and binding receipts

- The contract: declarations, insuring clauses, exclusions and exceptions, conditions, and endorsements and riders

Links

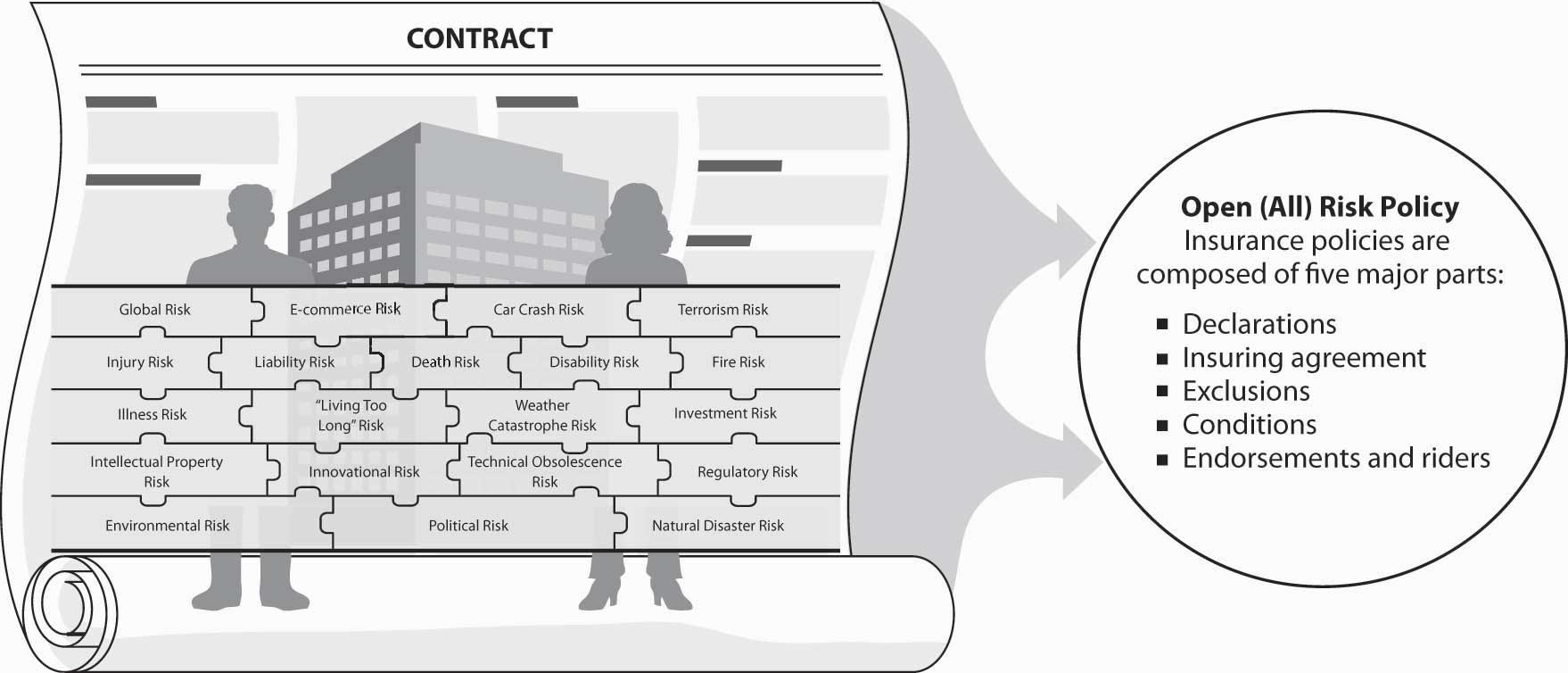

By now, we assume you are accustomed to connecting the specific topics of each chapter to the big picture of your holistic risk. This chapter is wider in scope. We are not yet delving into the specifics of each risk and its insurance programs. However, compared with "9: Fundamental Doctrines Affecting Insurance Contracts", we are drilling down a step further into the world of insurance legal documents. We focus on the open-peril type of policy, which covers all risks. This means that everything is covered unless specifically excluded, as shown in Figure \(\PageIndex{1}\). Nevertheless, the open-peril policy has many exclusions and more are added as new risks appear on the horizon. For the student who is first introduced to this field, this unique element is an important one to understand. Most insurance contracts in use today do not list the risks that are covered; rather, the policy lets you know that everything is covered, even new, unanticipated risks such as anthrax (described in the box “How to Handle the Risk Management of a Low-Frequency but Scary Risk Exposure: The Anthrax Scare?” in "4: Evolving Risk Management - Fundamental Tools"). When the industry realizes that a new peril is too catastrophic, it then exerts efforts to exclude such risks from the standardized, regulated policies. Such efforts are not easy and are met with resistance in many cases. As you learned in "6: The Insurance Solution and Institutions", catastrophic risks are not insurable by private insurers; therefore, they are excluded from the policies. In 2005, the topic of wind versus water was of concern as a result of hurricanes Katrina and Rita. Despite the devastation, all damages caused by flood water were excluded from the policies because floods are considered catastrophic. Another case in point is the terrorism exclusion that became moot after President Bush signed the Terrorism Risk Insurance Act (TRIA) in 2002.

Another important element achieved by exclusions, in addition to excluding the uninsurable risk of catastrophes, is duplication of coverage. Each policy is designed not to overlap with another policy. Such duplication would violate the contract of indemnity principal of insurance contracts. The homeowner’s liability coverage excludes automobile liability, workers’ compensation liability, and other such exposures that are nonstandard to home and personal activities. These specifics will be discussed in later chapters, but for now, it is important to emphasize that exclusions are used to reduce the moral hazard of allowing insureds to be paid twice for the same loss.

Thus, while each insurance policy has the components outlined in Figure \(\PageIndex{1}\), the exclusions are the part that requires in-depth study. Exclusions within exclusions in some policies are like a maze. We not only must ensure that we are covered for each risk in our holistic risk picture, we must also make sure no areas are left uncovered by exclusions. At this point, you should begin to appreciate the complexity of putting the risk management puzzle together to ensure completeness.