4.4: Financial Markets and Business

- Page ID

- 3612

What you’ll learn to do: describe common ways in which businesses obtain financial capital (money) to fund operations

In this section you will learn about some of the options businesses have to obtain capital and how they decide which form of capital best meets their needs.

Learning Objectives

- Distinguish between bonds and bank loans as methods of borrowing

- Define “stock”

How Businesses Raise Financial Capital

Firms often make decisions that involve spending money in the present and expecting to earn profits in the future. Some examples are: when a firm buys a machine that will last ten years, or builds a new plant that will last for thirty years, or starts a research and development project. They need economic resources—also known as financial capital—to do this. Firms can raise the financial capital they need to pay for such projects in four main ways: (1) from early-stage investors; (2) by reinvesting profits; (3) by borrowing through banks or bonds; and (4) by selling stock. As you’ll see, each financial option has different implications for the business in terms of operations and profits.

Firms often make decisions that involve spending money in the present and expecting to earn profits in the future. Some examples are: when a firm buys a machine that will last ten years, or builds a new plant that will last for thirty years, or starts a research and development project. They need economic resources—also known as financial capital—to do this. Firms can raise the financial capital they need to pay for such projects in four main ways: (1) from early-stage investors; (2) by reinvesting profits; (3) by borrowing through banks or bonds; and (4) by selling stock. As you’ll see, each financial option has different implications for the business in terms of operations and profits.

Early-Stage Financial Capital

Firms that are just beginning often have an idea or a prototype for a product or service to sell, but they have few customers, or even no customers at all, and thus are not earning profits. Banks are often unwilling to loan money to start-up businesses because they’re seen as too risky. Such firms face a difficult problem when it comes to raising financial capital: How can a firm that has not yet demonstrated any ability to earn profits pay a rate of return to financial investors?

For many small businesses, the original source of money is the owner of the business. Someone who decides to start a restaurant or a gas station, for instance, might cover the start-up costs by dipping into his or her own bank account or by borrowing money (perhaps using a home as collateral). Alternatively, many cities have a network of well-to-do individuals, known as “angel investors,” who will put their own money into small new companies at an early stage of development, in exchange for owning some portion of the firm.

Venture capital firms make financial investments in new companies that are still relatively small in size but have substantial growth potential. These firms gather money from a variety of individual or institutional investors, including banks, institutions like college endowments, insurance companies that hold financial reserves, and corporate pension funds. Venture capital firms do more than just supply money to small start-ups. They also provide advice on potential products, customers, and key employees. Typically, a venture capital fund invests in a number of firms, and then investors in that fund receive returns according to how the fund performs as a whole.

The amount of money invested in venture capital fluctuates substantially from year to year: As one example, venture capital firms invested more than $48.3 billion in 2014, according to the National Venture Capital Association. All early-stage investors realize that the majority of small start-up businesses will never hit it big; indeed, many of them will go out of business within a few months or years. They also know that getting in on the ground floor of a few huge successes like a Netflix or an Amazon.com can make up for a lot of failures. Early-stage investors are therefore willing to take large risks in order to be in a position to gain substantial returns on their investment.

Profits As a Source of Financial Capital

If firms are earning profits (their revenues are greater than costs), they can choose to reinvest some of these profits in equipment, structures, and research and development. For many established companies, reinvesting their own profits is one primary source of financial capital. Companies and firms just getting started may have numerous attractive investment opportunities but few current profits to invest. Even large firms can experience a year or two of earning low profits or even suffering losses, but unless the firm can find a steady and reliable source of financial capital so that it can continue making real investments in tough times, the firm may not survive until better times arrive. Firms often need to find sources of financial capital other than profits.

Borrowing: Banks and Bonds

When a firm has a record of at least earning significant revenues or, better still, of earning profits, the firm can make a credible promise to pay interest, and so it becomes possible for the firm to borrow money. Firms have two main methods of borrowing: banks and bonds.

A bank loan for a firm works in much the same way as a loan for an individual who is buying a car or a house. The firm borrows an amount of money and then promises to repay it, including some rate of interest, over a predetermined period of time. If the firm fails to make its loan payments, the bank (or banks) can often take the firm to court and require it to sell its buildings or equipment to make the loan payments.

Another source of financial capital is a bond. A bond is a financial contract: A borrower agrees to repay the amount that was borrowed and also a rate of interest over a period of time in the future. A corporate bond is issued by firms, but bonds are also issued by various levels of government. For example, a municipal bond is issued by cities, a state bond by U.S. states, and a Treasury bond (T-bond) by the federal government through the U.S. Department of the Treasury. A bond specifies an amount that will be borrowed, the interest rate that will be paid, and the time until repayment.

A large company, for example, might issue bonds for $10 million; the firm promises to make interest payments at an annual rate of 8 percent ($800,000 per year), and then, after ten years, it will repay the $10 million it originally borrowed. When a firm issues bonds, the total amount that is borrowed is divided up. A firm that seeks to borrow $50 million by issuing bonds might actually issue 10,000 bonds of $5,000 each. In this way, an individual investor could, in effect, loan the firm $5,000, or any multiple of that amount. Anyone who owns a bond and receives the interest payments is called a bondholder. If a firm issues bonds and fails to make the promised interest payments, the bondholders can take the firm to court and require it to pay, even if the firm needs to raise the money by selling buildings or equipment. However, there is no guarantee that the firm will have sufficient assets to pay off the bonds. The bondholders may get back only a portion of what they loaned the firm.

Bank borrowing is more customized than issuing bonds, so it often works better for relatively small firms. The bank can get to know the firm extremely well—often because the bank can monitor sales and expenses quite accurately by looking at deposits and withdrawals. Relatively large and well-known firms often issue bonds instead. They use bonds to raise new financial capital that pays for investments, or to raise capital to pay off old bonds, or to buy other firms. However, the idea that banks are usually used for relatively smaller loans and bonds for larger loans is not an ironclad rule: Sometimes groups of banks make large loans, and sometimes relatively small and lesser-known firms issue bonds.

Corporate Stock and Public Companies

A corporation is a business that “incorporates”—it is owned by shareholders that have limited liability for the debt of the company but share in its profits (and losses). Corporations may be private or public and may or may not have stock that is publicly traded. They may raise funds to finance their operations or new investments by raising capital through the sale of stock or the issuance of bonds.

Those who buy the stock become the owners, or shareholders, of the firm. Stock represents ownership of a firm; that is, a person who owns 100 percent of a company’s stock, by definition, owns the entire company. The stock of a company is divided into shares. Corporate giants like IBM, AT&T, Ford, General Electric, Microsoft, Merck, and Exxon all have millions of shares of stock. In most large and well-known firms, no individual owns a majority of the shares of the stock. Instead, large numbers of shareholders—even those who hold thousands of shares—each have only a small slice of the overall ownership of the firm.

When a company is owned by a large number of shareholders, three important questions emerge:

- How and when does the company get money from the sale of its stock?

- What rate of return does the company promise to pay when it sells stock?

- Who makes decisions in a company owned by a large number of shareholders?

First, a firm receives money from the sale of its stock only when the company sells its own stock to the public (the public includes individuals, mutual funds, insurance companies, and pension funds). A firm’s first sale of stock to the public is called an initial public offering (IPO). The IPO is important for two reasons. For one, the IPO, and any stock issued thereafter, such as stock held as treasury stock (shares that a company keeps in their own treasury) or new stock issued later as a secondary offering, provides the funds to repay the early-stage investors, like the angel investors and the venture capital firms. A venture capital firm may have a 40 percent ownership in the firm. When the firm sells stock, the venture capital firm sells its part ownership of the firm to the public. A second reason for the importance of the IPO is that it provides the established company with financial capital for a substantial expansion of its operations.

Most of the time when corporate stock is bought and sold, however, the firm receives no financial return at all. If you buy shares of stock in General Motors, you almost certainly buy them from the current owner of those shares, and General Motors does not receive any of your money. This pattern should not seem particularly odd. After all, if you buy a house, the current owner gets your money, not the original builder of the house. Similarly, when you buy shares of stock, you are buying a small slice of ownership of the firm from the existing owner—and the firm that originally issued the stock is not a part of this transaction.

Second, when a firm decides to issue stock, it must recognize that investors will expect to receive a rate of return. That rate of return can come in two forms. A firm can make a direct payment to its shareholders, called a dividend. Alternatively, a financial investor might buy a share of stock in Walmart for $45 and then later sell that share of stock to someone else for $60, for a gain of $15. The increase in the value of the stock (or of any asset) between when it is bought and when it is sold is called a capital gain.

Third: Who makes the decisions about when a firm will issue stock, or pay dividends, or reinvest profits? To understand the answers to these questions, it is useful to separate firms into two groups: private and public.

A private company is owned by the people who run it on a day-to-day basis. A private company can be run by individuals, in which case it is called a sole proprietorship, or it can be run by a group, in which case it is a partnership. A private company can also be a corporation, but the stock is not sold to the public. Instead, the company’s stock is offered, owned, and traded or exchanged privately. A small law firm run by one person, even if it employs some other lawyers, would be a sole proprietorship. A larger law firm may be owned jointly by its partners. Most private companies are relatively small, but there are some large private corporations, with tens of billions of dollars in annual sales, that do not have publicly issued stock, such as farm-products dealer Cargill, the Mars candy company, and the Bechtel engineering and construction firm.

When a firm decides to sell stock, which in turn can be bought and sold by financial investors, it is called a public company. Shareholders own a public company. Since the shareholders are a very broad group, often consisting of thousands or even millions of investors, the shareholders vote for a board of directors, who in turn hire top executives to run the firm on a day-to-day basis. The more shares of stock a shareholder owns, the more votes that shareholder is entitled to cast for the company’s board of directors.

In theory, the board of directors helps to ensure that the firm is run in the interests of the true owners—the shareholders. However, the top executives who run the firm have a strong voice in choosing the candidates who will be on their board of directors. After all, few shareholders are knowledgeable enough or have enough of a personal incentive to spend energy and money nominating alternative members of the board.

How Firms Choose between Sources of Financial Capital

There are clear patterns in how businesses raise financial capital. These patterns can be explained partly by the fact that buyers and sellers in a market do not both have complete and identical information. Those who are actually running a firm will almost always have more information about whether the firm is likely to earn profits in the future than outside investors who provide financial capital.

Any young start-up firm is a risk; indeed, some start-up firms are only a little more than an idea on paper. The firm’s founders inevitably have better information about how hard they are willing to work, and whether the firm is likely to succeed, than anyone else. When the founders put their own money into the firm, they demonstrate a belief in its prospects. At this early stage, angel investors and venture capitalists try to get all the information they need, partly by getting to know the managers and their business plan personally and by giving them advice.

As a firm becomes at least somewhat established and its strategy appears likely to lead to profits in the near future, knowing the individual managers and their business plans on a personal basis becomes less important, because information has become more widely available regarding the company’s products, revenues, costs, and profits. As a result, other outside investors who do not know the managers personally, like bondholders and shareholders, are more willing to provide financial capital to the firm.

At this point, a firm must often choose how to access financial capital. It may choose to borrow from a bank, issue bonds, or issue stock. The great disadvantage of borrowing money from a bank or issuing bonds is that the firm commits to scheduled interest payments, whether or not it has sufficient income. The great advantage of borrowing money is that the firm maintains control of its operations and is not subject to shareholders. Issuing stock involves selling off ownership of the company to the public and becoming responsible to a board of directors and the shareholders.

The benefit of issuing stock is that a small and growing firm increases its visibility in the financial markets and can access large amounts of financial capital for expansion, without worrying about paying this money back. If the firm is successful and profitable, the board of directors will need to decide upon a dividend payout or how to reinvest profits to further grow the company. Issuing and placing stock is expensive, requires the expertise of investment bankers and attorneys, and entails compliance with reporting requirements to shareholders and government agencies, such as the federal Securities and Exchange Commission.

Financial Markets

In 2006, housing equity in the United States peaked at $13 trillion. That means that the market prices of homes, less what was still owed on the loans used to buy these houses, equaled $13 trillion. This was a very good number, since the equity represented the value of the financial asset most U.S. citizens owned.

In 2006, housing equity in the United States peaked at $13 trillion. That means that the market prices of homes, less what was still owed on the loans used to buy these houses, equaled $13 trillion. This was a very good number, since the equity represented the value of the financial asset most U.S. citizens owned.

However, by 2008 this number had gone down to $8.8 trillion, and it declined further still in 2009. Combined with the decline in value of other financial assets held by U.S. citizens, by 2010, U.S. homeowners’ wealth had declined by $14 trillion! This is a staggering loss, and it affected millions of lives: people had to alter their retirement decisions, housing decisions, and other important consumption decisions. Just about every other large economy in the world suffered a decline in the market value of financial assets, as a result of the global financial crisis of 2008–2009.

This section will explain why people buy houses (other than as a place to live), why they buy other types of financial assets, and why businesses sell those financial assets in the first place. The section will also give us insight into why financial markets and assets go through boom-and-bust cycles like the one described here.

When a firm needs to buy new equipment or build a new facility, it often must go to the financial market to raise funds. Usually firms will add capacity during an economic expansion when profits are on the rise and consumer demand is high. Business investment is one of the critical ingredients needed to sustain economic growth. Even in the sluggish economy of 2009, U.S. firms invested $1.4 trillion in new equipment and structures, in the hope that those investments would generate profits in the years ahead.

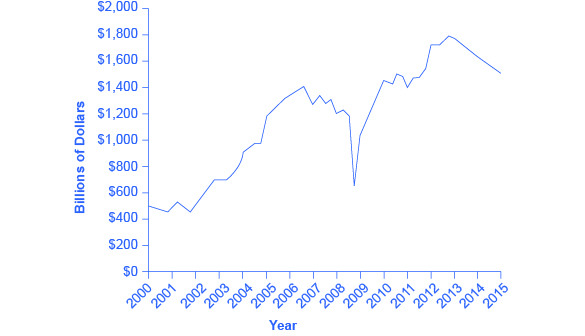

Between the end of the recession in 2009 through the second quarter 2013, profits for the S&P 500 companies grew to 9.7 percent despite the weak economy, with much of that amount driven by cost cutting and reductions in input costs, according to the Wall Street Journal. Figure \(\PageIndex{1}\), below, shows corporate profits after taxes (adjusted for inventory and capital consumption). Despite the steep decline in quarterly net profit in 2008, profits have recovered and surpassed pre-Recession levels.

Many firms, from huge companies like General Motors to start-up firms writing computer software, do not have the financial resources within the firm to make all the investments they want. These firms need financial capital from outside investors, and they are willing to pay interest for the opportunity to get a rate of return on the investment for that financial capital.

On the other side of the financial capital market, suppliers of financial capital, like households, wish to use their savings in a way that will provide a return. Individuals cannot, however, take the few thousand dollars that they save in any given year, write a letter to General Motors or some other firm, and negotiate to invest their money with that firm. Financial capital markets bridge this gap: That is, they find ways to take the inflow of funds from many separate suppliers of financial capital and transform it into the funds desired by demanders of financial capital. Such financial markets include stocks, bonds, bank loans, and other financial investments.