9.4: The Master Budget (Part 1)

- Page ID

- 889

- Develop the components of a master budget.

Question: Developing a master budget is a lengthy process. Where do companies start when preparing a master budget?

- Answer

-

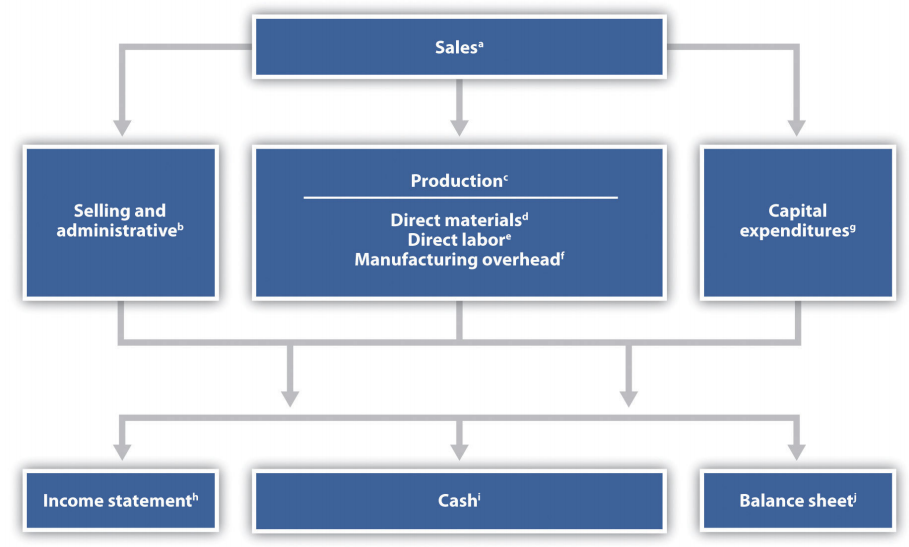

Study Figure 9.1 carefully, as it serves as the road map for the master budget presented throughout this chapter for Jerry’s Ice Cream. Notice that the budgeting process starts with the sales budget. Also, note that the budgets described next are for a manufacturing company. Manufacturing companies tend to have more budget schedules than other types of organizations because their operations are more complex. Once you understand budgeting in a manufacturing environment, you can easily modify the process to perform budgeting in other organizations, as discussed later in the chapter. As we work through the master budget for Jerry’s Ice Cream, assume the company prepares quarterly budgets.

Sales Budget

Question: The sales budget is the starting point for the master budget, as shown in Figure 9.1. What is a sales budget, and how is it prepared?

{kind=link}

- Answer

-

The sales budget5 is an estimate of units of product the organization expects to sell times the expected sales price per unit. This is perhaps the most important budget as it drives most of the other budgets. For example, the production budget and related materials, labor, and overhead budgets are based on expected sales.

Forecasting sales often involves extensive research and numerous sources. Companies, such as Jerry’s Ice Cream, typically start with their sales staff since salespeople have daily contact with customers and direct information about customer demand. Some companies pay for market trend data to learn about industry and product trends. Many organizations hire market research consultants to obtain and review industry data and ultimately to predict customer demand. Larger companies sometimes employ economists to develop sophisticated models used to project sales. Smaller, less sophisticated organizations simply base their estimates on past trends. Figure 9.2 shows how companies obtain sales information from sales people, market research consultants, and economists.

Figure \(\PageIndex{2}\): - Estimating Sales, © Thinkstock

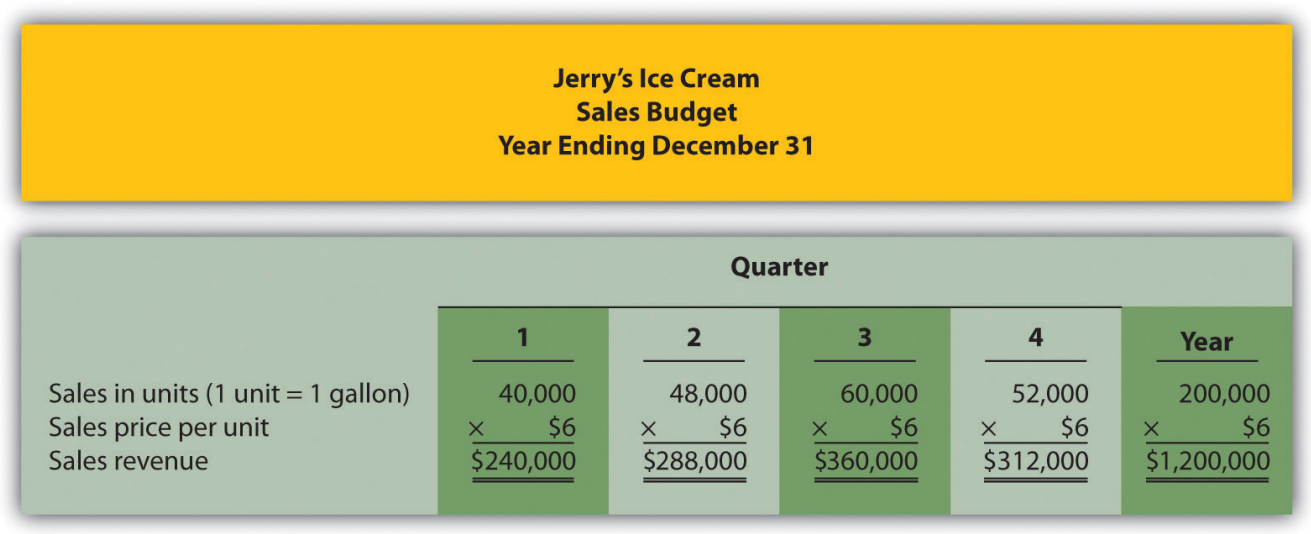

Tom Benson, sales manager at Jerry’s Ice Cream, talked with his salespeople and reviewed market trends for ice cream using data obtained from a market research firm. His estimate, shown in Figure 9.3, assumes the company will increase sales 15 percent this coming year. Thus, to get projected sales for quarter 1, Tom simply multiplied last year’s first quarter sales by 1.15. The average price per unit last year was $6 (1 unit = 1 gallon), and Tom does not expect any change in this price. The sales budget is presented in Figure 9.3.

Production Budget

Question: The production budget is developed next and is based on sales budget projections. What is a production budget, and how is it prepared?

- Answer

-

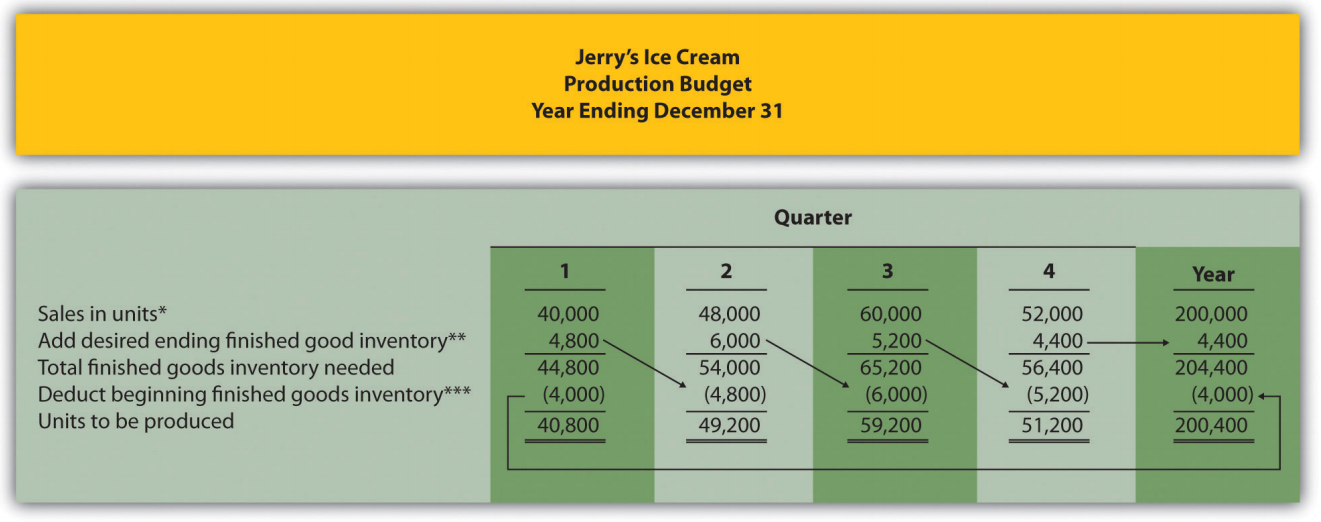

If the organization uses a just-in-time production system, where production occurs just in time to ship the products to the customer, units produced each quarter would be exactly the same as projected sales. However, most companies, including Jerry’s Ice Cream, maintain a certain level of finished goods inventory. Thus production is typically not the same as projected sales. The production budget6 is an estimate of units to be produced and is based on sales projections plus an estimate of desired ending finished goods inventory less beginning finished goods inventory, as summarized in the following:

\[\text{Units to be produced = Expected sales in units + Desired units of ending inventory - Units in beginning inventory}\]

Jerry’s Ice Cream plans to sell 40,000 units in the first quarter, as shown in Figure 9.3. For the sake of simplicity, assume work-in-process inventory is insignificant, and therefore beginning and ending work-in-process inventory is zero. (We assume beginning and ending work-in-process inventory is zero throughout this chapter.) The management prefers to maintain 10 percent of next quarter’s sales in ending inventory. Thus 4,800 units will be in inventory at the end of the first quarter (= 48,000 unit sales in second quarter × 10 percent). Units needed for the first quarter total 44,800 (= 40,000 unit sales + 4,800 units desired ending inventory). However, Jerry’s will not produce 44,800 units because inventory will be left over from the fourth quarter of last year. This beginning inventory will be 4,000 units (= 40,000 unit sales in first quarter × 10 percent). Thus actual production will total 40,800 units:

\[\begin{split} \text{Units to be produced} &= \text{Expected sales in units + Desired units of ending inventory - Units in beginning inventory} \\ 40,800 &= 40,000 + 4,800 - 4,000 \end{split}\]

Figure 9.4 presents the production budget for each of the 4 quarters of the coming year. Examine this figure carefully, particularly the last line labeled units to be produced. Lynn Young, the production manager, will be concerned about the spike in production during the third quarter of 59,200 units. The third quarter, from July 1 through September 30, is the peak sales season for ice cream. It will be difficult for Lynn to plan for this increase in production from the first and second quarters to the third quarter. However, this is exactly why companies prepare budgets—to plan for the future!

*Information from Figure 9.3.

**Desired ending inventory = 10 percent × Next quarter sales; for the first quarter, 4,800 = 0.10 × 48,000. Fourth quarter desired ending inventory of 4,400 units is based on an estimate of sales in the first quarter of next year.

***Beginning inventory = Inventory at end of previous quarter; for example, second quarter beginning inventory = First quarter ending inventory.

Once Jerry’s Ice Cream knows how many units it must produce each quarter, budgets are established for the individual components of production: direct materials, direct labor, and manufacturing overhead. We present these budgets next.

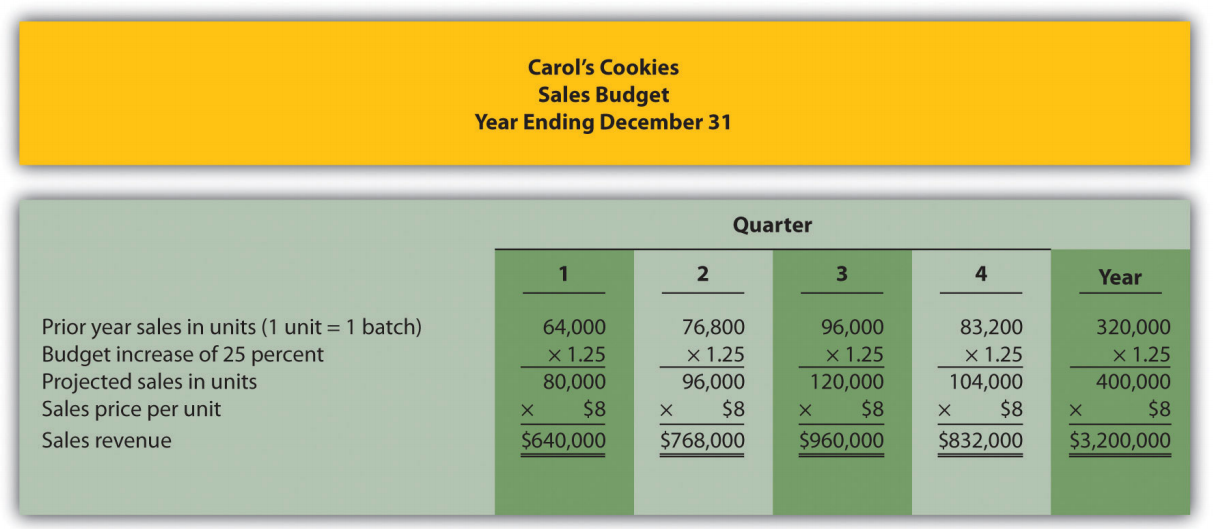

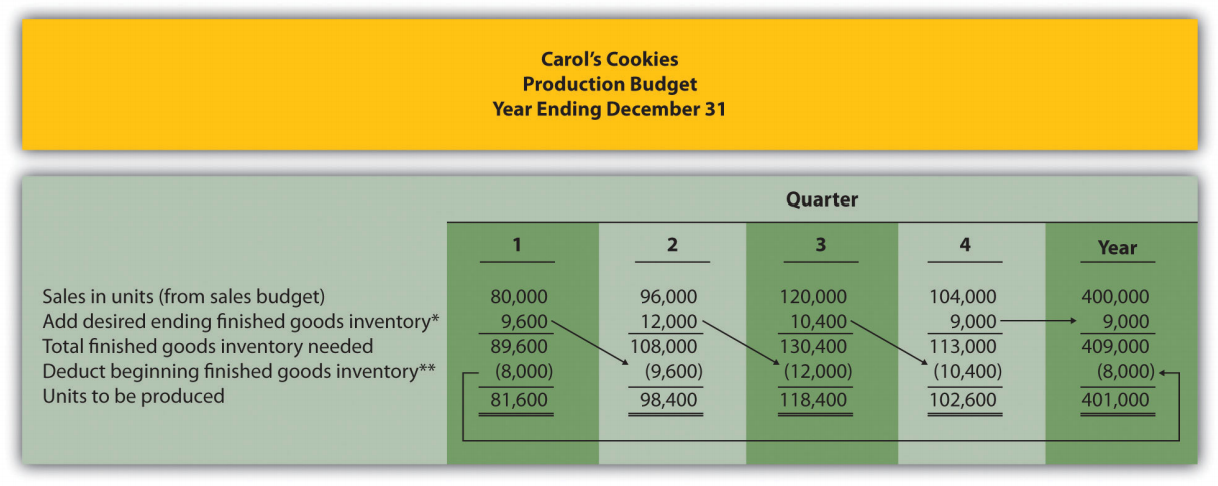

Carol’s Cookies produces cookies for resale at grocery stores throughout North America. The company is currently in the process of establishing a master budget on a quarterly basis for this coming fiscal year, which ends December 31. Prior year quarterly sales were as follows (1 unit = 1 batch):

| First quarter | 64,000 units |

| Second quarter | 76,800 units |

| Third quarter | 96,000 units |

| Fourth quarter | 83,200 units |

Unit sales are expected to increase 25 percent, and each unit is expected to sell for $8. The management prefers to maintain ending finished goods inventory equal to 10 percent of next quarter’s sales. Assume finished goods inventory at the end of the fourth quarter budget period is estimated to be 9,000 units.

- Prepare a sales budget for Carol’s Cookies using a format similar to Figure 9.3. (Hint: be sure to increase last year’s unit sales by 25 percent.)

- Prepare a production budget for Carol’s Cookies using the format shown in Figure 9.4.

- Answer

-

- The following is a sales budget:

- The following is a production budget:

*Desired ending inventory = 10 percent × Next quarter sales; for the first quarter, 9,600 = 0.10 × 96,000. Fourth quarter desired ending inventory of 9,000 units is given.

**Beginning inventory = Inventory at end of previous quarter; for example, Second quarter beginning inventory = First quarter ending inventory.

- The following is a sales budget:

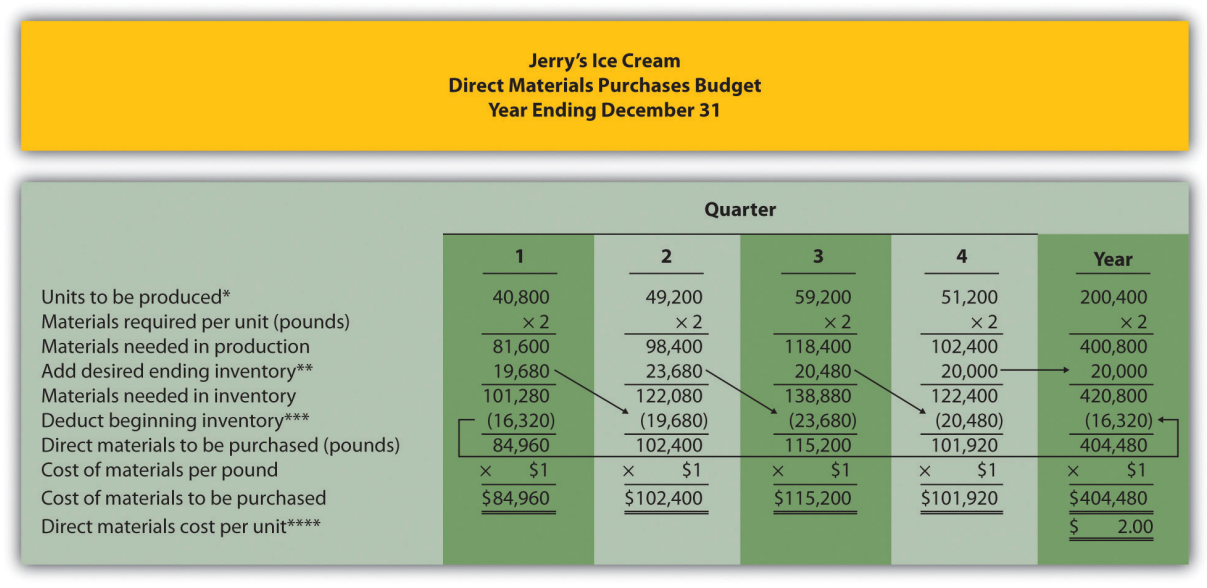

Direct Materials Purchases Budget

Question: The number of units of finished goods to be produced each quarter from the production budget is the starting point for the direct materials purchases budget. What is a direct materials purchases budget, and how is it prepared?

- Answer

-

The direct materials purchases budget7 is an estimate of raw materials needed to achieve a desired level of production. Figure 9.4, the production budget, shows that 40,800 finished units will be produced in the first quarter. We will now establish a direct materials purchases budget that answers the questions: how many pounds of material must be purchased during the first quarter to achieve this production, and what is the cost of these materials?

Assume two pounds of material are required to produce one unit of product. Thus the amount of materials required to produce 40,800 units of ice cream is 81,600 pounds (= 40,800 units × 2 pounds per unit). This amount is labeled as materials needed in production in the direct materials purchases budget shown in Figure 9.5. (To simplify this example, assume sugar is the only material used. However, other materials, such as cream and vanilla, are typically required to produce ice cream.)

Figure \(\PageIndex{5}\): - Direct Materials Purchases Budget for Jerry’s Ice Cream *Information from Figure 9.4.

**Desired ending inventory = 20 percent × Next quarter production needs; for the first quarter, 19,680 = 0.20 × 98,400. Fourth quarter desired ending inventory of 20,000 pounds is based on an estimate of materials needed in production first quarter of next year.

***Beginning inventory = Inventory at end of previous quarter; for example, Second quarter beginning inventory = First quarter ending inventory.

****$2 direct materials cost per unit = 2 pounds of materials required per unit × $1 per pound.

Will the company buy 81,600 pounds of material in the first quarter? Probably not. Jerry’s will have materials in beginning raw materials inventory and prefers to maintain a certain level of ending raw materials inventory. Thus direct materials purchased is based on materials needed in production plus an estimate of desired ending raw materials inventory less beginning raw materials inventory. We summarize this in the following equation. Notice the similarity of this equation to the inventory equation presented earlier for the production budget.

\[\text{Materials to be purchased = Materials needed in production + Desired materials in ending inventory - Materials in beginning inventory}\]

Assume the management prefers to maintain raw materials ending inventory equal to 20 percent of next quarter’s materials needed in production. Thus 19,680 pounds of material will be in inventory at the end of the first quarter (= 98,400 pounds of materials needed in production in second quarter × 20 percent). Materials needed in inventory total 101,280 pounds (= 81,600 pounds of materials needed in production + 19,680 pounds of material in desired ending inventory). However, Jerry’s will not purchase 101,280 pounds of materials because inventory will be left over from the fourth quarter of last year. This beginning inventory will be 16,320 pounds (= 81,600 pounds of material needed in production in first quarter × 20 percent). Thus direct materials purchased in the first quarter will total 84,960 pounds:

\[\begin{split} \text{Materials} &= \text{Materials needed in production + Desired materials in ending inventory - Materials in beginning inventory} \\ 84,960 &= 81,600 + 19,680 - 16,320 \end{split}\]

To estimate the cost of purchasing 84,960 pounds of material, multiply the number of pounds to be purchased by the cost per pound. Assume the cost per pound of material for Jerry’s is $1. This results in a cost of $84,960 for materials to be purchased during the first quarter, as shown at the bottom of Figure 9.5 (= 84,960 pounds to be purchased × $1 per pound).

Review the direct materials purchases budget shown in Figure 9.5 carefully, particularly the line labeled direct materials to be purchased. The purchasing manager at Jerry’s Ice Cream uses this information, along with the price per pound, to negotiate the purchase of materials with suppliers.

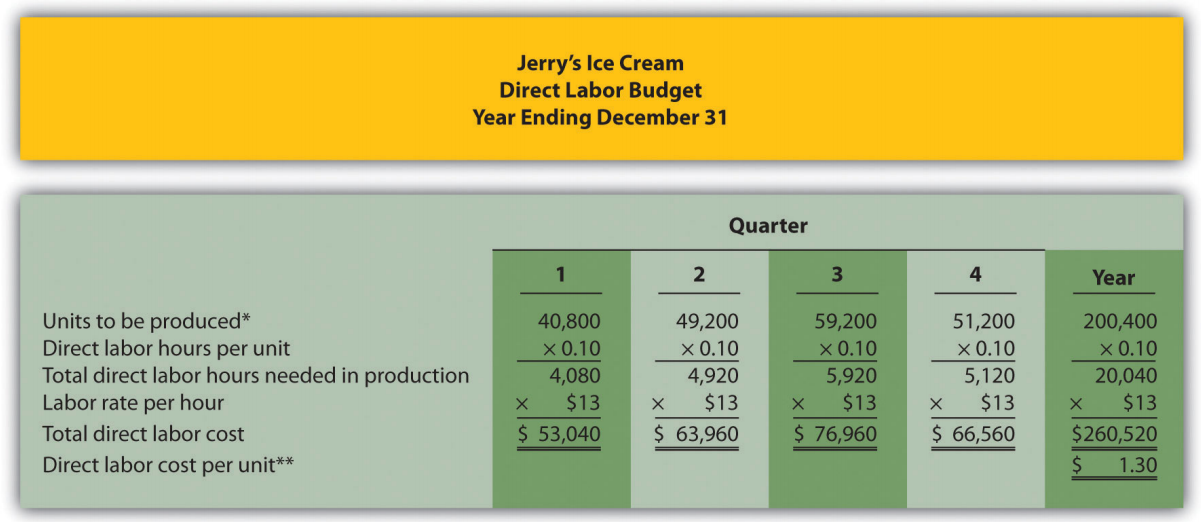

Direct Labor Budget

Question: The direct materials purchases budget is the first of three supporting budgets for production. The second is the direct labor budget. What is the direct labor budget, and how is it prepared?

- Answer

-

The direct labor budget8 is an estimate of direct labor hours, and related costs, necessary to achieve a desired level of production. Knowing Jerry’s Ice Cream plans to produce 40,800 units of ice cream during the first quarter, this budget answers the questions: how many direct labor hours will be necessary to achieve this production, and what will this labor cost?

Assume it takes 0.10 direct labor hours (or 6 minutes) to produce 1 unit of product. Thus 4,080 hours of direct labor will be required to produce 40,800 units of product (= 40,800 finished units produced × 0.10 direct labor hours per unit). Given an average hourly rate of $13, the direct labor cost for the first quarter totals $53,040 (= 4,080 hours × $13 per hour). This information is shown in the direct labor budget presented in Figure 9.6.

Figure \(\PageIndex{6}\): - Direct Labor Budget for Jerry’s Ice Cream *From Figure 9.4.

**$1.30 direct labor cost per unit = 0.10 direct labor hours per unit × $13 per hour.

Carefully review the direct labor budget shown in Figure 9.6. The production manager at Jerry’s Ice Cream, Lynn Young, uses this information to ensure the appropriate number of employees is available to meet production goals. Notice that the number of direct labor hours needed in production for the third quarter is significantly higher than each of the two previous quarters. Again, this is why organizations prepare budgets: to plan for these types of events. Lynn will have to start planning for this spike in direct labor hours, either by asking employees to work overtime or by hiring additional employees.

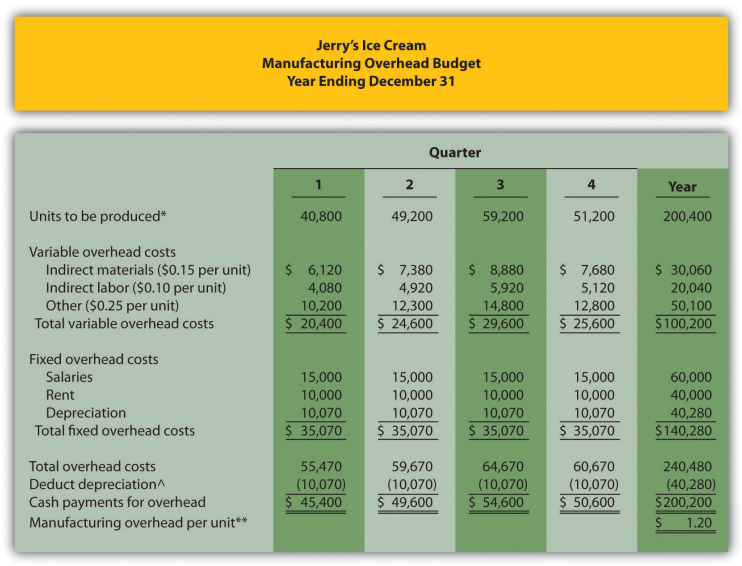

Manufacturing Overhead Budget

Question: The manufacturing overhead budget is the third of three supporting production budgets. What is a manufacturing overhead budget, and how is it prepared?

- Answer

-

The manufacturing overhead budget9 is an estimate of all production costs, other than direct materials and direct labor, necessary to achieve a desired level of production. This budget is presented in Figure 9.7. Notice that overhead costs are separated into variable and fixed components.

Figure \(\PageIndex{7}\): - Manufacturing Overhead Budget for Jerry’s Ice Cream *From Figure 9.4.

**$1.20 = $240,480 total overhead cost ÷ 200,400 units to be produced for the year.

^Deduct depreciation to get the actual cash payment for overhead. This information is needed for the cash budget presented in Figure 9.11.

By definition, total variable overhead costs change with changes in production and are calculated by multiplying units to be produced by the cost per unit. For example, indirect materials cost for the first quarter of $6,120 is calculated by taking 40,800 units to be produced × $0.15 cost per unit. Fixed costs generally do not change with changes in production and therefore remain the same each quarter. (Note: In some situations, fixed overhead costs can change from one quarter to the next. For example, hiring additional salaried personnel during the year would increase fixed overhead costs, and purchasing equipment during the year would increase depreciation costs. In this example, we assume fixed overhead costs do not change during the year.)

Depreciation is deducted at the bottom of the manufacturing overhead budget to determine cash payments for overhead because depreciation is not a cash transaction. We use this information later in the chapter for the cash budget.

Carol’s Cookies, the company featured in the last review problem and in the next three, is now preparing the budget for direct materials purchases, direct labor, and manufacturing overhead.

Direct Materials Purchases Budget Information

Each unit of product requires 1.5 pounds of direct materials per unit, and the cost of direct materials is $2 per pound. Management prefers to maintain ending raw materials inventory equal to 30 percent of next quarter’s materials needed in production. Assume raw materials inventory at the end of the fourth quarter budget period is estimated to be 41,000 pounds.

Direct Labor Budget Information

Each unit of product requires 0.20 direct labor hours at a cost of $12 per hour.

Manufacturing Overhead Budget Information

Variable overhead costs are:

| Indirect materials | $0.20 per unit |

| Indirect labor | $0.15 per unit |

| Other | $0.35 per unit |

Fixed overhead costs each quarter are:

| Salaries | $28,000 |

| Rent | $22,000 |

| Depreciation | $16,165 |

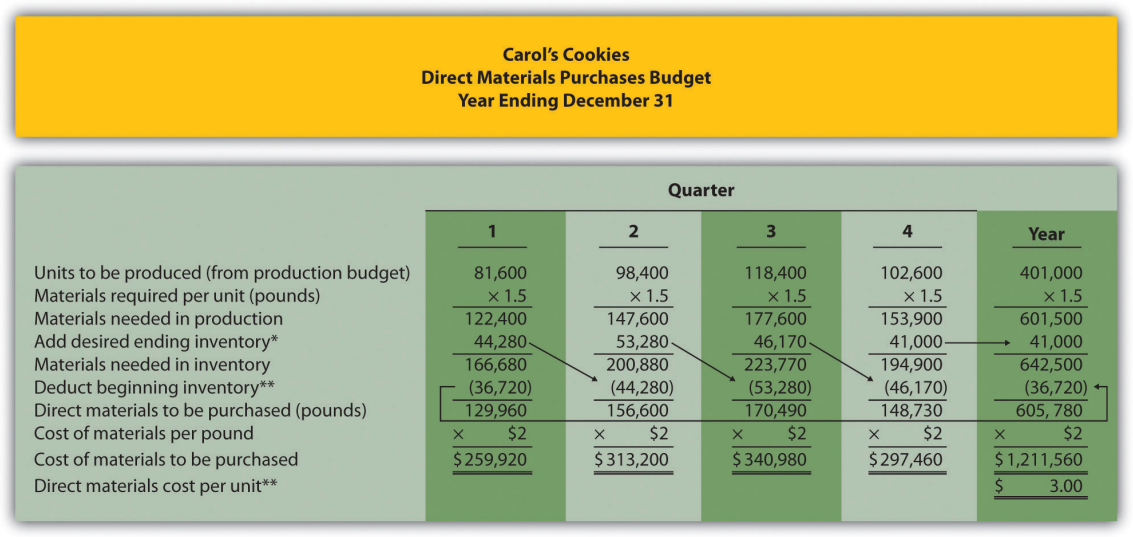

- Prepare a direct materials purchases budget for Carol’s Cookies using the format shown in Figure 9.5.

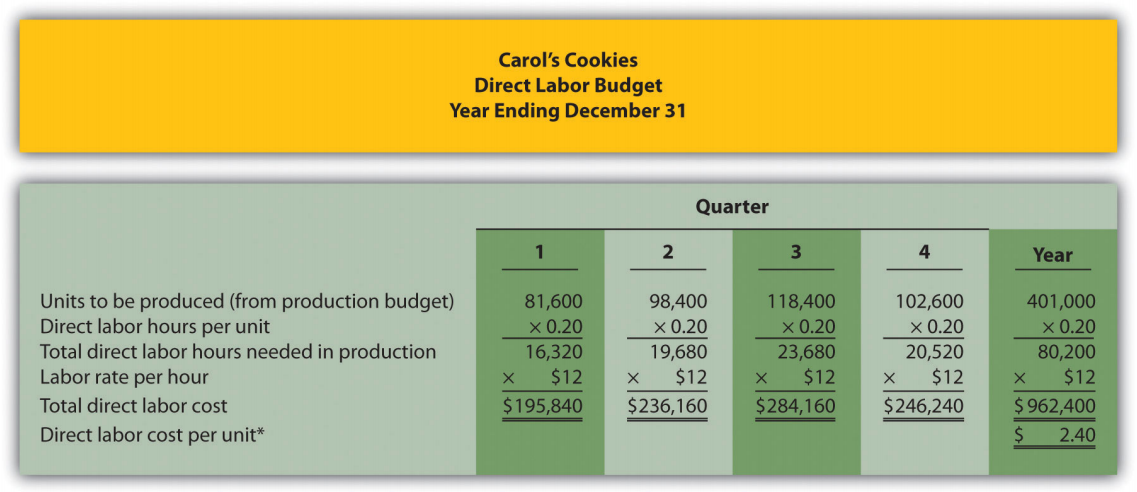

- Prepare a direct labor budget for Carol’s Cookies using the format shown in Figure 9.6.

- Prepare a manufacturing overhead budget for Carol’s Cookies using the format shown in Figure 9.7.

- Answer

-

*Desired ending inventory = 30 percent × Next quarter production needs; for the first quarter, 44,280 = 0.30 × 147,600 pounds. Fourth quarter desired ending inventory of 41,000 pounds is given.

**Beginning inventory = Inventory at end of previous quarter; for example, Second quarter beginning inventory = First quarter ending inventory.

***$3 direct materials cost per unit = 1.5 pounds of materials required per unit × $2 per pound.

*$2.40 direct labor cost per unit = 0.20 direct labor hours per unit × $12 per hour.

*$1.36 = $545,360 total overhead cost ÷ 401,000 units to be produced for the year.

^Deduct depreciation to get the actual cash payment for overhead. This information is needed for the cash budget prepared later.

Definitions

- An estimate of units of product the organization expects to sell times the expected sales price per unit.

- An estimate of units to be produced, and it is based on sales projections plus an estimate of desired ending finished goods inventory less beginning finished goods inventory.

- An estimate of raw materials needed to achieve a desired level of production.

- An estimate of direct labor hours, and related cost, necessary to achieve a desired level of production.

- An estimate of all production costs, other than direct materials and direct labor, necessary to achieve a desired level of production.