3.2: Process Costing Transactions for a Manufacturing Company

- Page ID

- 44213

Cost accumulation in each department and the transfer from one department to the next is recorded using the following series of journal entries.

Mixing Department

A batch begins in the Mixing Department when materials are added.

- Direct materials - ingredients such as flour, eggs, sugar, and (of course) chocolate chips - that cost $4,600 and indirect materials that cost $400 are requisitioned.

Account

Debit

Credit

Work in Process – Mixing Dept.

4,600

▲ Work in Process is an asset (inventory) account that is increasing

Factory Overhead – Mixing Dept.

400

▲ Factory Overhead is an expense account that is increasing

Materials

5,000

▼ Materials is an asset (inventory) account that is decreasing

- Direct labor - workers combining ingredients, hand stirring the batter, and operating the mixers - costs $2,100 and indirect labor for general factory use costs $200.

Account

Debit

Credit

Work in Process – Mixing Dept.

2,100

▲ Work in Process is an asset (inventory) account that is increasing

Factory Overhead – Mixing Dept.

200

▲ Factory Overhead is an expense account that is increasing

Wages Payable

2,300

▲ Wages Payable is a liability account that is increasing

- Factory overhead of $1,000 is applied on an estimated basis so that the batch absorbs a proportionate share of the department’s general factory costs, such as utilities, insurance, and supervisor salary.

Account

Debit

Credit

Work in Process – Mixing Dept.

1,000

▲ Work in Process is an asset (inventory) account that is increasing

Factory Overhead – Mixing Dept.

1,000

▼ Factory Overhead is an expense account that is decreasing

Notice there are three debits to Work in Process - Mixing for the three costs of manufacturing in Mixing. These three debits total $7,700 ($4,600 + $2,100 + $1,000).

Once the batch is mixed, there is nothing more the Mixing Department can do; in terms of mixing, the product is complete. The mixed batch is then sent off to the Baking Department by crediting Work in Process - Mixing (decreasing that asset account) and debiting Work in Process - Baking (increasing that asset account) for $7,700.

- Transfer from the Mixing Department to the Baking Department, $7,700

Account

Debit

Credit

Work in Process – Baking Dept.

7,700

▲ Work in Process is an asset (inventory) account that is increasing

Work in Process – Mixing Dept.

7,700

▼ Work in Process is an asset (inventory) account that is decreasing

(Although not illustrated here because our journal entries are only tracking the first batch, as the work in process is transferred from Mixing to Baking, a new batch of materials may be introduced into the Mixing Department to keep the flow of production continuous.)

Baking Department

The batch is now in production in the Baking Department.

- Direct materials - spray oil used to keep the cookies from sticking to the pans - that costs $600 and indirect materials that cost $300 are requisitioned.

Account

Debit

Credit

Work in Process – Baking Dept.

600

▲ Work in Process is an asset (inventory) account that is increasing

Factory Overhead – Baking Dept.

300

▲ Factory Overhead is an expense account that is increasing

Materials

900

▼ Materials is an asset (inventory) account that is decreasing

- Direct labor - workers pressing the cookies onto sheets and operating machinery - costs $1,400 and indirect labor for general factory use costs $100.

Account

Debit

Credit

Work in Process – Baking Dept.

1,400

▲ Work in Process is an asset (inventory) account that is increasing

Factory Overhead – Baking Dept.

100

▲ Factory Overhead is an expense account that is increasing

Wages Payable

1,500

▲ Wages Payable is a liability account that is increasing

- Factory overhead of $500 is applied on an estimated basis so that the batch absorbs a proportionate share of the department’s general factory costs, such as utilities, insurance, and supervisor salary.

Account

Debit

Credit

Work in Process – Baking Dept.

500

▲ Work in Process is an asset (inventory) account that is increasing

Factory Overhead – Mixing Dept.

500

▼ Factory Overhead is an expense account that is decreasing

Notice there are four debits to Work in Process – Baking. One is for the cost transferred in from the Mixing Department; the others are the three costs of manufacturing added in the Baking Department. These four debits total $10,200 ($7,700 + $600 + $1,400 + $500).

Once the batch is baked, there is nothing more the Baking Department can do; as far as what it is set up to do, the product is complete. So, it transfers the baked batch to the Packaging Department by crediting Work in Process - Baking (decreasing that asset account) and debiting Work in Process - Packaging (increasing that asset account) for $10,200.

- Transfer from the Baking Department to the Packaging Department, $10,200

Account

Debit

Credit

Work in Process – Packaging Dept.

10,200

▲ Work in Process is an asset (inventory) account that is increasing

Work in Process – Baking Dept.

10,200

▼ Work in Process is an asset (inventory) account that is decreasing

Packaging Department

The batch is now in production in the Packaging Department.

- Direct materials - boxes and packing materials - that cost $1,100 and indirect materials that cost $900 are requisitioned.

Account

Debit

Credit

Work in Process – Packaging Dept.

1,100

▲ Work in Process is an asset (inventory) account that is increasing

Factory Overhead – Packaging Dept.

900

▲ Factory Overhead is an expense account that is increasing

Materials

2,000

▼ Materials is an asset (inventory) account that is decreasing

- Direct labor - workers hand packing and sealing shipping boxes - costs $3,000 and indirect labor for general factory use costs $700.

Account

Debit

Credit

Work in Process – Packaging Dept.

3,000

▲ Work in Process is an asset (inventory) account that is increasing

Factory Overhead – Packaging Dept.

700

▲ Factory Overhead is an expense account that is increasing

Wages Payable

3,700

▲ Wages Payable is a liability account that is increasing

- Factory overhead of $900 is applied on an estimated basis so that the batch absorbs a proportionate share of the department’s general factory costs, such as utilities, insurance, and supervisor salary.

Account

Debit

Credit

Work in Process – Packaging Dept.

900

▲ Work in Process is an asset (inventory) account that is increasing

Factory Overhead – Packaging Dept.

900

▼ Factory Overhead is an expense account that is decreasing

Notice there are four debits to Work in Process – Packaging. One is for the cost transferred in from the Baking Department; the others are the three costs of manufacturing in Packaging. These four debits total $15,200 ($10,200 + $1,100 + $3,000 + $900).

Transfer from Packaging Department to finished Goods

Once the batch is packed in boxes, there is nothing more the Packaging Department can do; the product is entirely complete. The packaged batch is transferred to Finished Goods at the overall accumulated cost of $15,200.

- Transfer from the Packaging Department to Finished Goods, $15,200

Account

Debit

Credit

Finished Goods

15,200

▲ Finished Goods is an asset (inventory) account that is increasing

Work in Process – Packaging Dept.

15,200

▼ Work in Process is an asset (inventory) account that is decreasing

The manufactured goods accumulate costs all throughout the production process. Each batch picks up materials cost, direct labor cost, and factory overhead cost in each of the three departments. The total of all these costs equals the total cost of producing the batch. Determining the cost of the batch and the cost of each unit in the batch is the goal of process costing.

The process costing journal entries illustrate the cost accumulation process through the three Work in Process accounts all the way through to Finished Goods. There are other process costing transactions that are similar to those for job order costing. A process costing manufacturer would also purchase materials on account, record numerous factory expenses by debiting Factory Overhead (in a specific department), sell goods on account and recognize a corresponding reduction of finished goods inventory, and account for over applied and under applied factory overhead amounts. Examples of these transactions are shown under the Job Order Costing topic and will not be repeated here. The only difference between the two methods is that under process costing the department name must be included whenever a Factory Overhead account is used.

Tracking Product Costs

There are three departments in the cookie factory example, and each one operates independently and does its own accounting. Assuming the company prepares monthly financial statements, each department must provide monthly information about its inventory for the balance sheet. We will now just look at the recordkeeping that occurs in a single department for a one-month period.

We will now focus only on the Packaging Department in the month of May. Assume you are the Packaging Department manager. You are responsible for keeping track of the cost of every unit that has been started and passes through your department during the month, whether the units have been finished by the end of May or not. For those units that have been completed, you must figure the total cost of each batch and the cost of each unit in the batch. For those units that are in production but not yet completed by the end of the month, you must determine the cost to date of that batch and each unit in the batch.

We will make two assumptions: (1) All materials that are needed to work on a batch of items in a department are added when the batch is started; (2) When a batch is started in the department, it will either be completed in the same month or completed in the following month.

Remember that there are three costs of a manufactured item: direct materials, direct labor, and factory overhead. Conversion costs are simply direct labor PLUS factory overhead. For process costing, the two costs of a manufactured item will be referred to as direct materials and conversion costs.

There are three departments in this factory. If you are the manager of the Packaging Department, your responsibility is limited to tracking the costs of the units in your department, but not in any of the other departments. The other departments have their own managers to take care of accounting for their costs. You don’t have to keep track of the cost of every item in EVERY department - just your own.

Similarly, as a university professor, I have to report final course grades for the 160 students in my four classes. During the semester I record exam, homework, and project grades for my students, and from those I mathematically calculate each student’s final course grade. It is my responsibility to do this for every student in my classes, but I do not have to calculate the final course grades for all students in all classes at the university!

In a process costing system, both the cost of units transferred out of each department and the cost of any partially completed units remaining in the department must be determined.

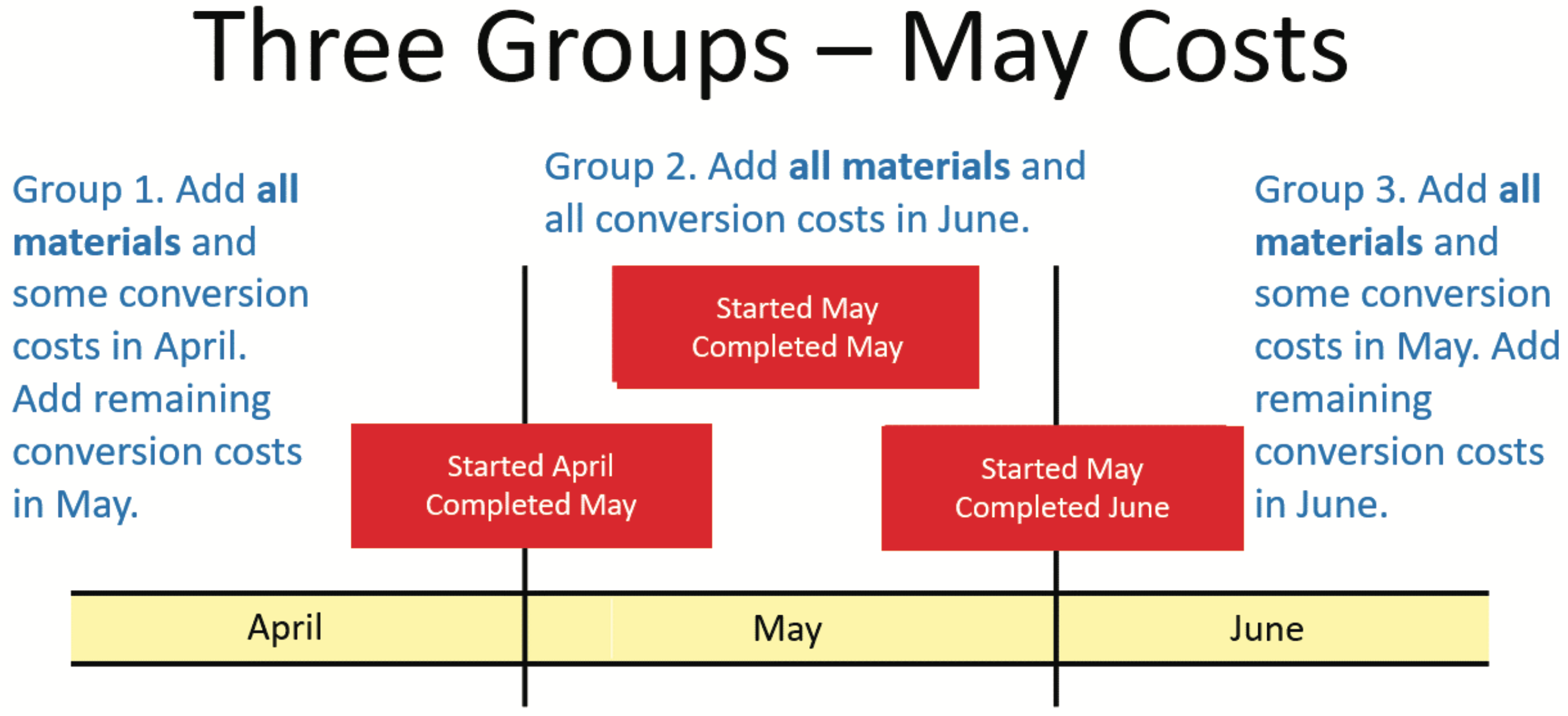

In each department, we determine both the total and per-unit costs of the products that were completed in a given month. These completed units are classified into two groups: those started in the previous month and those started in the current month. The per-unit cost is not necessarily the same in the two groups, and any difference may be analyzed to see if unit cost is decreasing (typically favorable) or increasing (unfavorable) over time.

We also accumulate costs for a third group of products: those started in the current month but not completed by the end of the month. Their costs include 100% of the materials cost and a percentage below 100% of the conversion costsbased on how complete they are to date. This third group, not finished by the end of the current month, becomes the beginning work in process for the next month, when the remaining conversion will take place to complete them.

The following timeline illustrates the flow of product from month to month.