7.2: Statement of Cash Flows

- Page ID

- 43112

Managers, investors, and lenders are particularly interested in the availability of cash, where it comes from, and what it is used for in a business. However, the income statement, retained earnings statement, and balance sheet do not directly track or report the flow of cash. Therefore, businesses prepare a fourth financial statement, the statement of cash flows, to clearly provide information about the sources and uses of cash.

The statement of cash flows is based on information from the income statement, retained earnings statement, and balance sheet. Therefore, it is prepared last.

7.2.1 Types of Business Activities

All business transactions can be classified as one of three types of activities: operating, investing, or financing.

Operating activities are those involved in the day-to-day running of the business. Accounts used for operating activities include all those on the income statement as well as current assets and current liabilities on the balance sheet. (Current assets and liabilities are those that are expected to be converted to cash within one year.) Most of a business’ transactions are operating activities.

Investment activities involve fixed or long-term assets that are found on the balance sheet. These are assets that are expected to last more than one year. Investment activities include buying and/or selling any of the following: equipment, vehicles, buildings, land, patents, investments in stock, and investments in bonds.

Financing activities involve raising funds for a business and may include long-term debt or equity accounts found on the balance sheet. These include transactions involving the following: issuing common or preferred stock, issuingor redeeming bonds payable, and paying off a mortgage note payable. Buying or selling treasury stock and paying dividends are related to stock and are also financing activities.

7.2.2 Cash Inflows and Outflows

The statement of cash flows reports cash inflows and/or cash outflows in each of three sections: cash flows from operating activities, cash flows from investing activities, and cash flows from financing activities. An inflow occurs when cash is paid to a business. An outflow is when a business makes a cash payment.

Each of the three sections is summarized by one number, which is the net cash flows amount. If the summary number is positive, it means that more cash was received than was paid out for that activity during the accounting period. If the summary number is negative, more cash was paid out than was received for that activity during the period.

You receive and cash your paycheck for the week for $400. This is a cash inflow. On the same day you pay your cell phone bill and car insurance payment for a total of $210. You then go out for dinner and pay $30 cash with tip. These three payments are cash outflows. The net cash inflow on that day is $160; that is, $160 more came in than went out.

The following sample journal entries are reminders of transactions that involve cash. The Cash account is either debited or credited, to indicate a cash inflow or cash outflow, respectively.

When Cash is debited, there is a cash inflow. Here is an example of an investing activity that results in a cash inflow: selling equipment.

| Account | Debit | Credit | ||

| ▲ | Cash | 50,000 | ||

| ▼ | Accumulated Depreciation | 1,000 | ||

| ▼ | Equipment | 48,000 | ||

| ▲ | Gain on Sale of Equipment | 3,000 |

Cash inflow: $50,000. Notice there is a gain on this transaction.

When Cash is credited, there is a cash outflow. Here is an example of a financing activity that results in a cash outflow: calling bonds.

| Account | Debit | Credit | |

| ▼ | Bonds Payable | 100,000 | |

| ▲ | Loss on Redemption of Bonds | 5,000 | |

| ▼ | Discount on Bonds Payable | 3,000 | |

| ▼ | Cash | 102,000 |

Cash outflow: $102,000. Notice there is a loss on this transaction.

When Cash is debited, here is a cash inflow. Here is an example of a financing activity that results in a cash inflow: issuing common stock.

| Account | Debit | Credit | |

| ▲ | Cash | 180,000 | |

| ▲ | Common Stock | 150,000 | |

| ▲ | Paid-in Capital in Excess of Par - Common Stock | 30,000 |

Cash inflow: $180,000. Notice there is no gain or loss on this transaction.

The operating activities section of the statement of cash flows appears first. It may be prepared in one of two ways, using either the indirect or the direct method. The indirect method begins with net income from the income statement and mathematically backs out non-cash transactions to arrive at cash flows from operating activities.The direct method itemizes all of the operating cash inflows, or receipts, followed by a list of the operating cash ouflows, or payments. Although information presented in the operating activities section is different, both methods yield the same cash flows from operating activities amount. The indirect method is more popular because the information needed to prepare the section is readily available on the income statement and balance sheet. The choice of methods pertains only to the operating activities section. The investing and financing section both are prepared using a direct method.

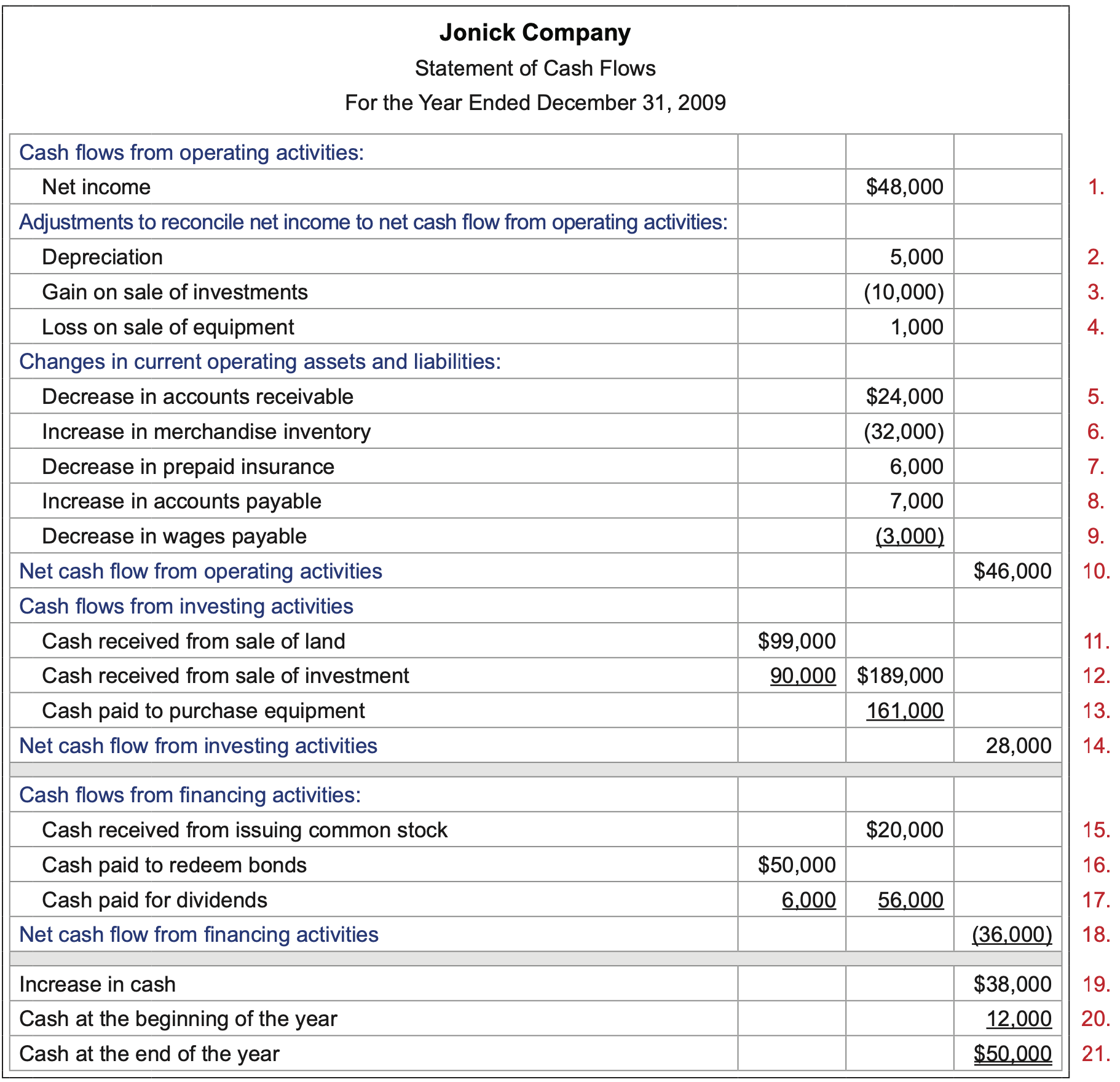

The following is a sample statement of cash flows that has been prepared based on the financial statements presented on page 255. The operating activities section uses the indirect method.

- From the income statement.

- Depreciation expense amount from the income statement.

- Other revenues and expenses section of the income statement - deduct gains included in net income.

- Other revenues and expenses section of the income statement - add back losses included in net income.

- Difference between beginning-of-year and end-of-year amounts on the balance sheet: 58,000 - 34,000. Add decreases in current assets.

- Difference between beginning-of-year and end-of-year amounts on the balance sheet: 80,000 - 112,000. Deduct increases in current assets.

- Difference between beginning-of-year and end-of-year amounts on the balance sheet: 15,000 - 9,000. Add decreases in current assets.

- Difference between beginning-of-year and end-of-year amounts on the balance sheet: 22,000 - 29,000. Add increases in current liabilities.

- Difference between beginning-of-year and end-of-year amounts on the balance sheet: 17,000 - 14,000. Deduct decreases in current liabilities.

- Total of all of the amounts in the operating activities section.

- Cost of $100,000 given on the balance sheet minus the $1,000 loss shown on the income statement = the amount of cash received.

- Cost of $80,000 given on the balance sheet plus the $10,000 gain shown on the income statement = the amount of cash received.

- Increase in Equipment on the balance sheet from 60,000 to 221,000 is the cash paid for new equipment since there were no sales of equipment.

- Total of all the cash inflows (added) and cash outflows (deducted) equals net cash flows from investing activities.

- Increases in Common Stock and Paid-in Capital accounts on the balance sheet (140,000 - 125,000) + (30,000 - 25,000).

- Decrease in Bonds Payable on the balance sheet from 50,000 to 0.

- Beginning Cash Dividends Payable balance of 8,000 + cash dividends declared on the retained earnings statement of 3,000 - ending Cash Dividends Payable balance of 5,000.

- Total of all the cash inflows (added) and cash outflows (deducted) equals net cash flows from financing activities.

- The difference between the beginning and ending Cash balances.

- From the balance sheet, beginning Cash balance.

- From the balance sheet, ending Cash balance.

The following section will show you how to prepare the statement of cash flows (indirect method for operating activities section) on page 259 from the financial statements on page 255.

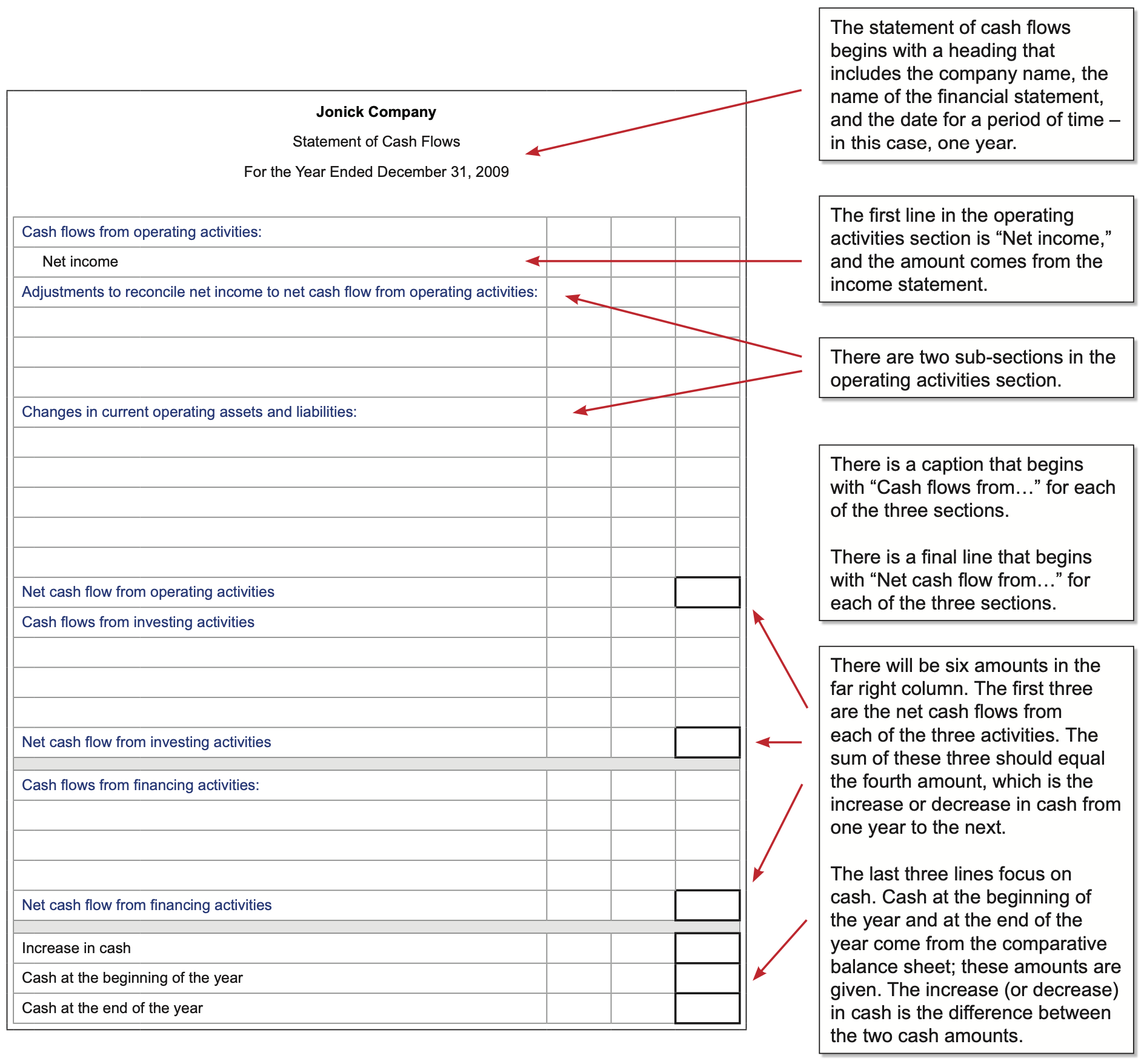

7.2.3 Basic Shell of the Statement of Cash Flows (indirect method)

Steps in Preparing the Statement of Cash Flows

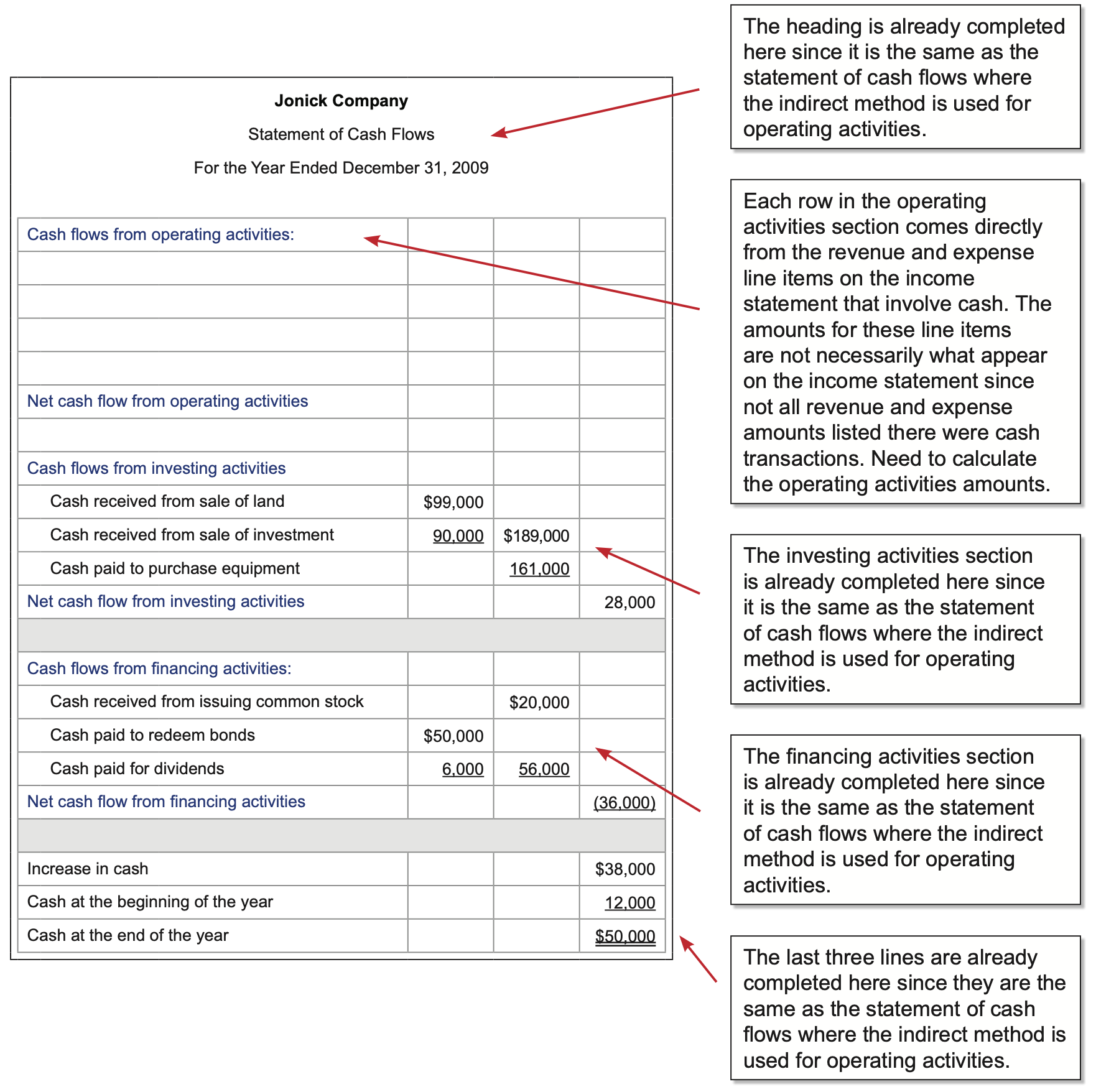

Using the basic shell that includes the heading and formatting captions, complete the statement of cash flows.

Operating activities section (indirect method)

Most of a business’ transactions are operating activities. Some of these involve cash; some do not. There are too many transactions to make it practical to look at each one individually to determine its impact on cash flow. Therefore, the income statement and comparative balance sheet numbers will be used to efficiently remove non-cash transactions in order to arrive at the net cash flow from operating activities number. The process is described next.

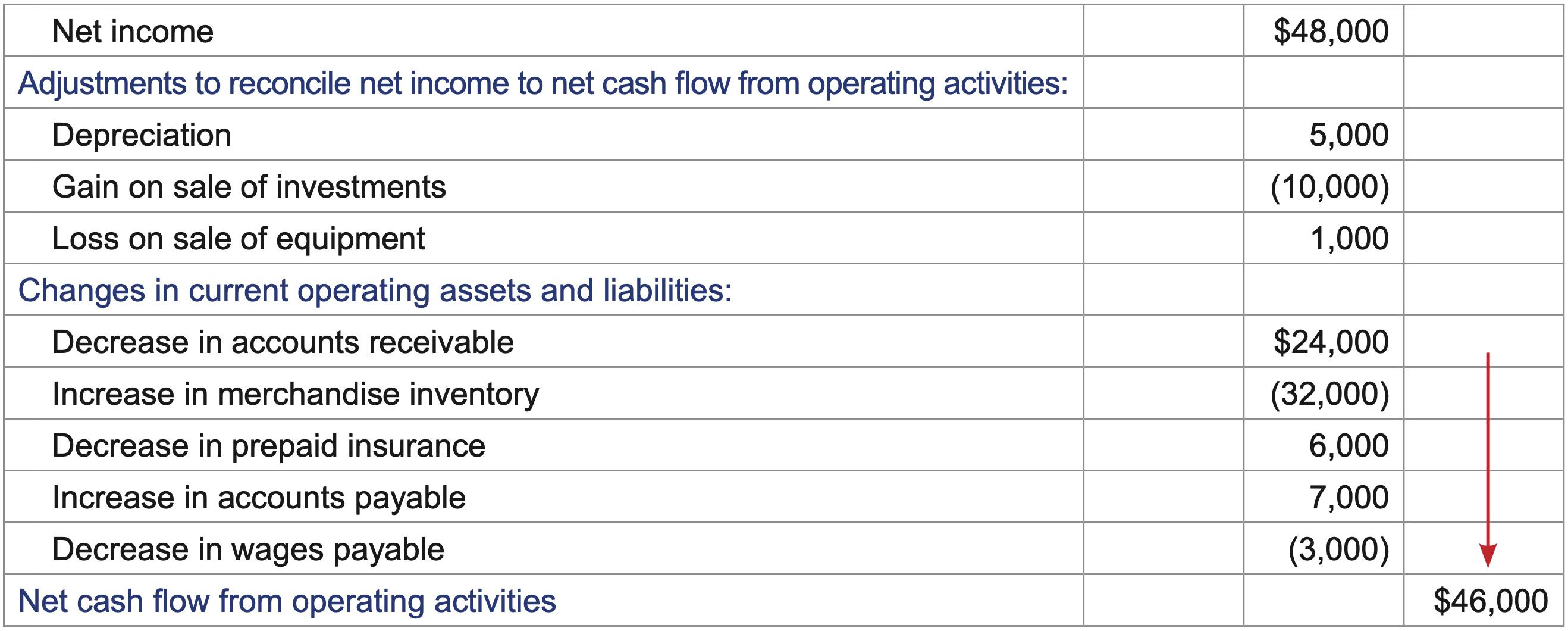

- Enter the net income amount, which is the final number on the income statement that is given.

Cash flows from operating activities: Net income $48,000 - Adjust the net income amount to remove non-cash expenses such depreciation expense and interest expense on the amortization of a bond discount. Also add back losses and deduct gains shown on the income statement since they do not pertain to operating activities and therefore do not belong in the operating activities section.

Adjustments to reconcile net income to net cash flow from operating activities: Depreciation 5,000 Gain on sale of investments (10,000) Loss on sale of equipment 1,000 - Current assets and liabilities are used in the operation of the business and are relatively short term; less than one year before used or converted to cash. Identify the CURRENT assets (except Cash) and CURRENT liabilities on the comparative balance sheet. Calculate the amount of increase or decrease in each one between the previous year and the current year (shown in red in the far right column below.)

Comparative Balance Sheet December 31, 2019 and 2018

End 2019 End 2018 Assets Accounts receivable 34,000 58,000 24,000 decrease Merchandise inventory 112,000 80,000 32,000 increase Prepaid insurance 9,000 15,000 6,000 decrease Liabilities Accounts payable 29,000 22,000 7,000 increase Wages payable 14,000 17,000 3,000 decrease To remove non-cash operating transactions, the difference in the amount from one year and the next for each of these accounts is reported in the operating activities section of the statement of cash flows using the following rules:

Add the following to net income:

- Decreases in current assets (accounts receivable, inventory, prepaid insurance, prepaid expenses, etc.)

- Increases in current liabilities (accounts payable, wages payable, accrued expenses, etc.)

Deduct the following from net income:

- Increases in current assets (accounts receivable, inventory, prepaid insurance, prepaid expenses, etc.)

- Decreases in current liabilities (accounts payable, wages payable, accrued expenses, etc.)

Changes in current operating assets and liabilities: Decrease in accounts receivable $24,000 Increase in merchandise inventory (32,000) Decrease in prepaid insurance 6,000 Increase in accounts payable 7,000 Decrease in wages payable (3,000) List these current operating assets and liabilities in the order in which they appear on the balance sheet. Be sure any deductions in the operating activities section are in parenthesis to indicate they are amounts to be subtracted.

- Calculate net cash flows from operating activities amount by adding to and/or subtracting from net income.

The final summary amount indicates that $46,000 more “came in” than was paid out during this year for operating activities. (If it were a net cash outflow, use parenthesis on the number to indicate this.) This is the first of six numbers in the right-hand column.

Investing Activities Section

There are relatively few items in the investing activities section, so it is reasonable to look at them one by one to determine if there is a cash inflow or outflow and, if so, its amount.

Identify the investing activities on the comparative balance sheet. These are any fixed, long-term, or intangible assets

| End 2019 | End 2018 | |

| Investment in ABC Co. Stock | 0 | 80,000 |

| Equipment | 221,000 | 60,000 |

| Accumulated depreciation | (50,000) | (45,000) |

| Land | 0 | 100,000 |

- All investing and financing activities were for cash.

- No additional investments were purchased.

- No additional land was purchased.

- No equipment was sold or otherwise disposed of.

If a fixed asset’s balance increases from one year to the next, it means that more must have been purchased and there was a cash outflow. Similarly, if a fixed asset’s balance decreases from one year to the next, it means that some or all of it was sold and there was a cash inflow. To help determine the amount of cash received or paid, refer to the journal entry for each transaction to see if Cash was debited or credited.

IMPORTANT: It is possible for one fixed asset, such as equipment, to have both a sale and a purchase of two different pieces of equipment for cash. This would have to be explained in a separate note in order to properly prepare the statement of cash flows.

When a long-term or fixed asset is sold, there may be a gain or loss. This information would be found on the income statement.

| Other revenue and expenses | |||

| Gain on sale of investments | 10,000 | ||

| Loss on sale of land | (1,000) | 9,000 | |

| Net income | 48,000 |

The land cost $100,000 (given on the balance sheet) and there was a loss of $1,000 when it was sold (given on the income statement). That would mean there was a $99,000 cash inflow ($100,000 - $1,000).

The investments cost $80,000 (given on the balance sheet) and there was a gain of $10,000 when they were sold (given on the income statement). That would mean there was a $90,000 cash inflow ($80,000 + $10,000).

The Equipment balance on the balance sheet at the beginning of the year was $60,000 and at the end of the year was $221,000, an increase of $161,000. Since it was noted that no equipment was sold, this is the amount of the cash outflow for equipment.

Each investing activity transaction is listed on its own line on the statement of cash flows. Cash inflows are listed first and each begins with “Cash received from...” Cash outflows follow and each begins with “Cash paid for...” If there is more than one inflow, they are subtotaled in the middle column. The same is true for more than one outflow.

| Cash flows from investing activities | |||

| Cash received from sale of land | $99,000 | ||

| Cash received from sale of investment | 90,000 | $189,000 | |

| Cash paid to purchase equipment | 161,000 | ||

| Net cash flow from investing activities | 28,000 |

Calculate net cash flows from investing activities amount by deducting cash outflows from cash inflows. This final summary amount indicates that $28,000 more “came in” than was paid out during this year for investing activities. (If it were a net cash outflow, use parenthesis to indicate this.) This is the second of six numbers in the right-hand column.

As a different possibility, an asset account such as Equipment may have experienced more than one transaction rather than just a single purchase. Using the same comparative balance sheet information as in the previous example, note that the information to its right in item d. shows that some of the equipment was also sold.

| End 2019 | End 2018 | |

| Investment in ABC Co. Stock | 0 | 80,000 |

| Equipment | 221,000 | 60,000 |

| Accumulated depreciation | (50,000) | (45,000) |

| Land | 0 | 100,000 |

- All investing and financing activities were for cash.

- No additional investments were purchased.

- No additional land was purchased.

- Equipment that cost $15,000 was sold for its current book value of $10,000 (therefore, no gain or loss on the sale.)

This would impact the cash flows from investing activities section since there would be an additional cash receipt.

| Cash flows from investing activities | |||

| Cash received from sale of equipment | $10,000 | ||

| Cash received from sale of land | 99,000 | ||

| Cash received from sale of investment | 90,000 | $199,000 | |

| Cash paid to purchase equipment | 171,000 | ||

| Net cash flow from investing activities | 28,000 |

Additional equipment still had to have been purchased since the overall Equipment balance on the balance sheet increased from year to year. The calculation to determine the amount of the purchase is as follows:

$221,000 ending balance - ($60,000 beginning balance - $10,000 cost of equipment sold given) = $171,000 purchased The same information about the equipment that was sold could have been

provided in the form of a ledger account, such as the one that follows for Equipment:

| Date | Item | Debit | Credit | Debit | Credit |

| 1/1/2012 | Balance | 60,000 | |||

| 4/3/2012 | 10,000 | 50,000 | |||

| 9/12/2012 | 171,000 | 221,000 |

The beginning and ending balances that appear on the comparative balance sheet are the same as those in the Equipment ledger’s debit balance column on January 1 and September 12, respectively. The $10,000 credit entry is the cost of the equipment that was sold on April 3. The $171,000 debit entry in the debit column is the cost of the equipment that was purchased on September 12. The sale results in a cash inflow, and the purchase results in a cash outflow.

Financing Activities Section

There are relatively few items in the financing activities section, so it is reasonable to look at them one by one to determine if there is a cash inflow or outflow and, if so, its amount.

- Identify the financing activities on the comparative balance sheet. These are found in the long-term liabilities or stockholders’ equity sections of the balance sheet.

Jonick Company Comparative Balance Sheet

December 31, 2019 and 2018

End 2019 End 2018 Liabilities Cash dividends payable 5,000 8,000 Bonds payable 0 50,000 Stockholders’ Equity Common stock 140,000 125,000 Paid-in capital in excess of par 30,000 25,000 Retained earnings158,000113,000If a long-term liability or stockholders’ equity account balance increases from one year to the next, it means that more must have been borrowed or received from investors and there may have been a cash inflow. Similarly, if a long-term liability account balance decreases from one year to the next, it means that it was repaid and there was a cash outflow. To help determine the amount of cash received or paid, refer to the journal entry for each transaction.

Cash flows from financing activities: Cash received from issuing common stock $20,000 Cash paid to redeem bonds $50,000 Cash paid for dividends 6,000 56,000 Net cash flow from financing activities (36,000) - For stock issuances, add the increase in Common Stock + the increase in Paid- in Capital in Excess of Par to determine the amount of cash inflow [($140,000 - $125,000) + ($30,000 - $25,000)].

- Cash paid for dividends is calculated as follows:

Beginning Cash Dividends Payable balance + Cash dividends declared – ending Cash Dividends Payable balance

Cash dividends declared is found on the retained earnings statement. In this case the calculation is $8,000 + $3,000 - $5,000 = $6,000.

Each financing activity transaction is listed on its own line on the statement of cash flows. Cash inflows are listed first and each begins with “Cash received from...” Cash outflows follow and each begins with “Cash paid for...” If there is more than one inflow, they are subtotaled in the middle column. The same is true for more than one outflow.

- Calculate net cash flows used for financing activities amount by deducting cash outflows from cash inflows. Use parenthesis since it is a net cash outflow. This final summary amount indicates that $36,000 more was paid out than “came in” during this year for financing activities. This is the third of six numbers in the right-hand column.

- Add the three numbers for cash flows from/used for operating, investing, and financing activities and label it as “Increase in cash” if it is positive or “Decrease in cash” if it is negative.”

- Add the net cash flows amounts from the three types of activities. The sum should equal the increase (or decrease) in cash amount.

- List the amounts of cash at the beginning and the end of the year that are given on the balance sheet. The difference should equal the sum of the cash flows amounts from the three types of activities.

Net cash flow from operating activities $46,000 Net cash flow from investing activities 28,000 Net cash flow from financing activities (36,000) Increase in cash $38,000 Cash at the beginning of the year 12,000 Cash at the end of the year $50,000 The statement of cash flows used in this example is a relatively simple one. There may be additional accounts that impact cash and therefore would also need to be included in other situations. Conversely, not all of the items on this sample statement of cash flows must be included on other statements. Only include those that are relevant to the problem or business you are working on and omit all others.

Analogy – Cash paid for dividends is calculated as follows:

Beginning Cash Dividends Payable balance + Cash dividends declared – ending Cash Dividends Payable balanceThe beginning Cash Dividends Payable balance is what the company already owed stockholders from dividends it declared the previous year but did not yet pay. Cash dividends declared is additional amounts promised and owed to stockholders for the current year. Those two combined represent the total owed. The Cash Dividends Payable balance at the end of the year is what has not yet been paid. The difference between the total owed and the total not yet paid is what must have been paid out in cash.

Think of it this way. I borrowed $50 from a student last week. On the way to class today, I borrowed another $10 from him. I owe a total of $60 to this student. If we leave class today and I owe him $20, there is only one explanation: I must have paid him $40 while we were in class. That was my cash outflow during the period.

Final Formatting Note for the Investing and Financing Sections

In the investing and financing sections, there may be cash receipts and/or cash payments. In each section, if there is more than one cash receipt, enter their amounts in the left column and a subtotal in the middle column. If there is only one receipt, enter it directly in the middle column. The same holds true for cash payments. See the examples below.

| Three receipts; one payment example with one subtotal | |||

| Cash flows from . . . activities: | |||

| Cash received from . . . | $1,000 | ||

| Cash received from . . . | 2,000 | ||

| Cash received from . . . | 3,000 | $6,000 | |

| Cash paid for . . . | 4,000 | ||

| Net cash from from . . . activities | $2,000 | ||

| Two receipts; two payments example with two subtotals | |||

| Cash flows from . . . activities: | |||

| Cash received from . . . | $1,000 | ||

| Cash received from . . . | 2,000 | $3,000 | |

| Cash paid for . . . | $4,000 | ||

| Cash paid for . . . | 5,000 | 9,000 | |

| Net cash flow from activities | (6,000) | ||

The following is a sample statement of cash flows that has been prepared based on the financial statements presented on page 255. The operating activities section uses the direct method in the operating activities section.

Two-step calculation to determine cash paid for inventory

First determine the cost of inventory purchases. The determine how much of those purchases was paid in cash.

- Beginning Inventory balance + purchases - cost of merchandise sold = ending inventory balance: solve for purchases, the unknown

80,000 + ? - 94,000 = 112,000; therefore? = 112,00 - 80,000 + 94,000 = 126,000 - Beginning Accounts Payable + purchases - ending Accounts Payable = cash paid for purchases

22,000 + 126,000 - 29,000 = 119,000

- Beginning Accounts Receivable balance from balance sheet + Sales from income statement - ending Accounts Receivable balance from the balance sheet.

- See two-step calculation above.

- Beginning Wages Payable balance from balance sheet + Wages Expense from income statement - ending Wages Payable balance from the balance sheet.

- Rent Expense amount from the income statement since it is a cash payment.

- Total of all of the amounts in the operating acivities section.

- The remainder of the statement of cash flows if the same as the example that used the indirect method for the operating activities section.

The following section will show you how to prepare the statement of cash flows (direct method for operating activities section) on page 270 from the financial statements on page 255.

7.2.4 Basic Shell of the Statement of Cash Flows (direct method)

Steps in Preparing the Statement of Cash Flows

Using the basic shell that includes the heading and formatting captions, complete the statement of cash flows.

Operating activities section (direct method)

The operating activities section using the line items on the income statement that (1) relate to operations and (2) that involve cash transactions. In the sample income statement below, there are six operational accounts: Sales, Cost of Merchandise Sold, and four expense accounts that might possibly be listed on the statement of cash flows if they involve cash. The gain and loss that is listed on the income statement are the result of transactions that do not relate to the normal operations of the business, so they will not appear in the operating activities section on the statement of cash flows when using the direct method. Balance sheet accounts are needed as well to mathematically determine how much of some of the amounts are cash transactions.

| Sales | $174,000 | ||

| Gain on sale of investments | 94,000 | ||

| Gross Profit | $80,000 | ||

| Operating Expenses | |||

| Wages expense | $20,000 | ||

| Rent expense | 10,000 | ||

| Insurance expense | 6,000 | ||

| Depreciation expense | 5,000 | ||

| Total operating expenses | 41,000 | ||

| 39,000 | |||

| Other revenue and expenses | |||

| Gain on sale of investments | 10,000 | ||

| Loss on sale of equipment | (1,000) | 9,000 | |

| Net income | 48,000 |

| End 2019 | End 2018 | |

| Assets | ||

| Cash | $50,000 | $12,000 |

| Accounts receivable | 34,000 | 58,000 |

| Merchandise Inventory | 112,000 | 80,000 |

| Prepaid insurance | 9,000 | 15,000 |

| Liabilities | ||

| Accounts payable | $29,000 | $22,000 |

| Wages payable | 14,000 | 17,000 |

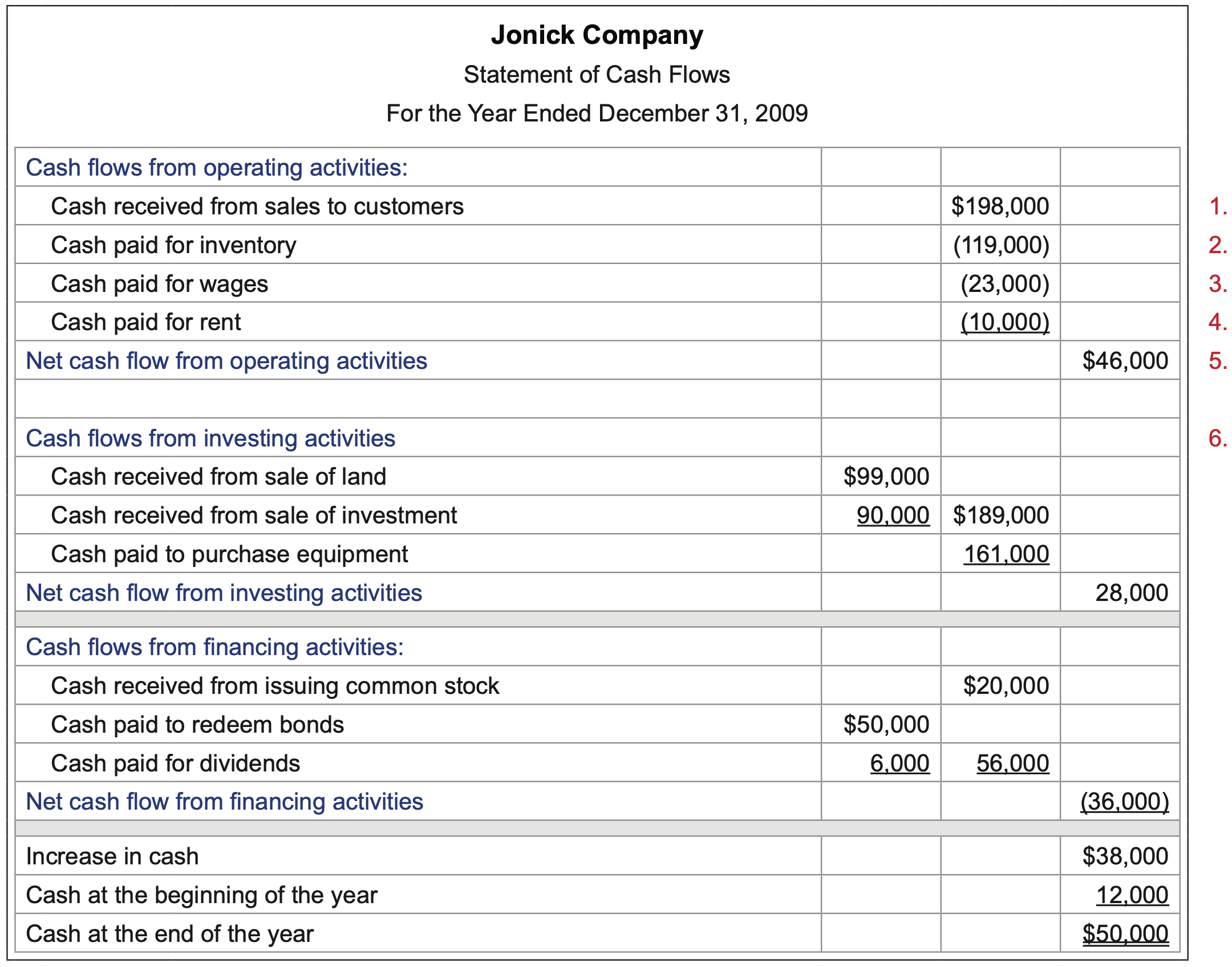

- The first line item listed in the operating activities section is Cash received from sales to customers. The amount of $198,000 is determined by using the Sales amount from the income statement and the Accounts Receivable amounts on the comparative balance sheet (partial), as follows:

Beginning Accounts Receivable + Sales – Ending Accounts Receivable = cash received from sales to customers

58,000 + 174,000 – 34,000 = 198,000Jonick Company Statement of Cash

Flows For the Year Ended December 31, 2009

Cash flows from operating activities: Cash received from sales to customers $198,000 Net cash flow from operating activities - The second line item relates to cash paid for inventory. The calculation is a two-step process. The amount of $119,000 is determined by using the Cost of Merchandise Sold amount from the income statement and the Merchandise Inventory AND Accounts Payable amounts on the comparative balance sheet (partial), as follows:

(1) Beginning Inventory + Purchases (unknown) – Cost of Merchandise Sold = Ending Inventory

80,000 + x – 94,000 = 112,000

x = 112,000 – 80,000 + 94,000 = 126,000 in purchases(2) Beginning Accounts Payable + Purchases – Ending Accounts Payable = cash paid for inventory

22,000 + 126,000 – 29,000 = 119,000The $119,000 is a deduction in the operating activities section.

Jonick Company Statement of Cash Flows

For the Year Ended December 31, 2009

Cash flows from operating activities: Cash received from sales to customers $198,000 Cash paid for inventory (119,000) Net cash flow from operating activities - The third line item relates to cash paid for wages. The amount of $23,000 is determined by using the Wages Expense amount from the income statement and the Wages Payable amounts on the comparative balance sheet (partial), as follows:

Beginning Wages Payable + Wages Expense – Ending Wages Payable = cash paid to employees

17,000 + 20,000 – 14,000 = 23,000Jonick Company Statement of Cash Flows

For the Year Ended December 31, 2009

Cash flows from operating activities: Cash received from sales to customers $198,000 Cash paid for inventory (119,000) Cash paid for wages (23,000) Net cash flow from operating activities - The fourth line item relates to cash paid for rent. Since Rent Expense is a cash transaction, the amount of $10,000 from the income statement is deducted in the operating activities section.

Cash flows from operating activities: Cash received from sales to customers $198,000 Cash paid for inventory (119,000) Cash paid for wages (23,000) Cash paid for rent (10,000) Net cash flow from operating activities $46,000 Insurance Expense and Depreciation Expense are non-cash items on the income statement and are therefore not included in the operating activities section. The difference in the Prepaid Insurance amounts on the balance sheets is $3,000 ($9,000 - $6,000), and that is the amount of Insurance Expense on the income statement. Therefore there was no net cash expenditure for insurance this period.

7.2.5 Comparative Operating Activities Sections – Statement of Cash Flows

Indirect Method

| Cash flows from operating activities: | |||

| Net income | $48,000 | ||

| Adjustments to reconcile net income to net cash flow from operating activities: | |||

| Depreciation | 5,000 | ||

| Gain on sale of investments | (10,000) | ||

| Loss on sale of equipment | 1,000 | ||

| Changes in current operating assets and liabilities: | |||

| Decrease in accounts receivable | 24,000 | ||

| Increase in merchandise inventory | (32,000) | ||

| Decrease in prepaid insurance | 6,000 | ||

| Increase in accounts payable | 7,000 | ||

| Decrease in wages payable | (3,000) | ||

| Net cash flow from operating activities | $46,000 |

Direct Method

| Cash flows from operating activities: | |||

| Cash received from sales to customers | $198,000 | ||

| Cash paid for inventory | (119,000) | ||

| Cash paid for wages | (23,000) | ||

| Cash paid for rent | (10,000) | ||

| Net cash flow from operating activities | $46,000 |

Notice that for both methods, the net cash flow from operating activities amount is the same: $46,000.