6.2: Corporations and Stockholders’ Equity

- Page ID

- 43093

A corporation is a form of business organization that is a separate legal entity; it is distinct from the people who own it. The corporation can own property, enter into contracts, borrow money, conduct business, earn profit, pay taxes, and make investments similar to the way individuals can.

The owners of a corporation are called stockholders. These are people who have invested cash or contributed other assets to the business. In return, they receive shares of stock, which are transferable units of ownership in a corporation. Stock can also be thought of as a receipt to acknowledge ownership in the company. The value of the stock that a stockholder receives equals the value of the asset(s) that were contributed.

A corporation may be owned by one stockholder or by millions. Very small companies can incorporate by filing articles of incorporation with a state in the U.S. and being granted corporate status.

Corporations are ongoing. Stockholders can buy and sell their shares of stock without interrupting the operation of the company. Another characteristic of a corporation is limited liability. Stockholders can lose no more than the amount they invested in the corporation. If the corporation fails, the individuals who own it do not personally have to cover the corporation’s liabilities.

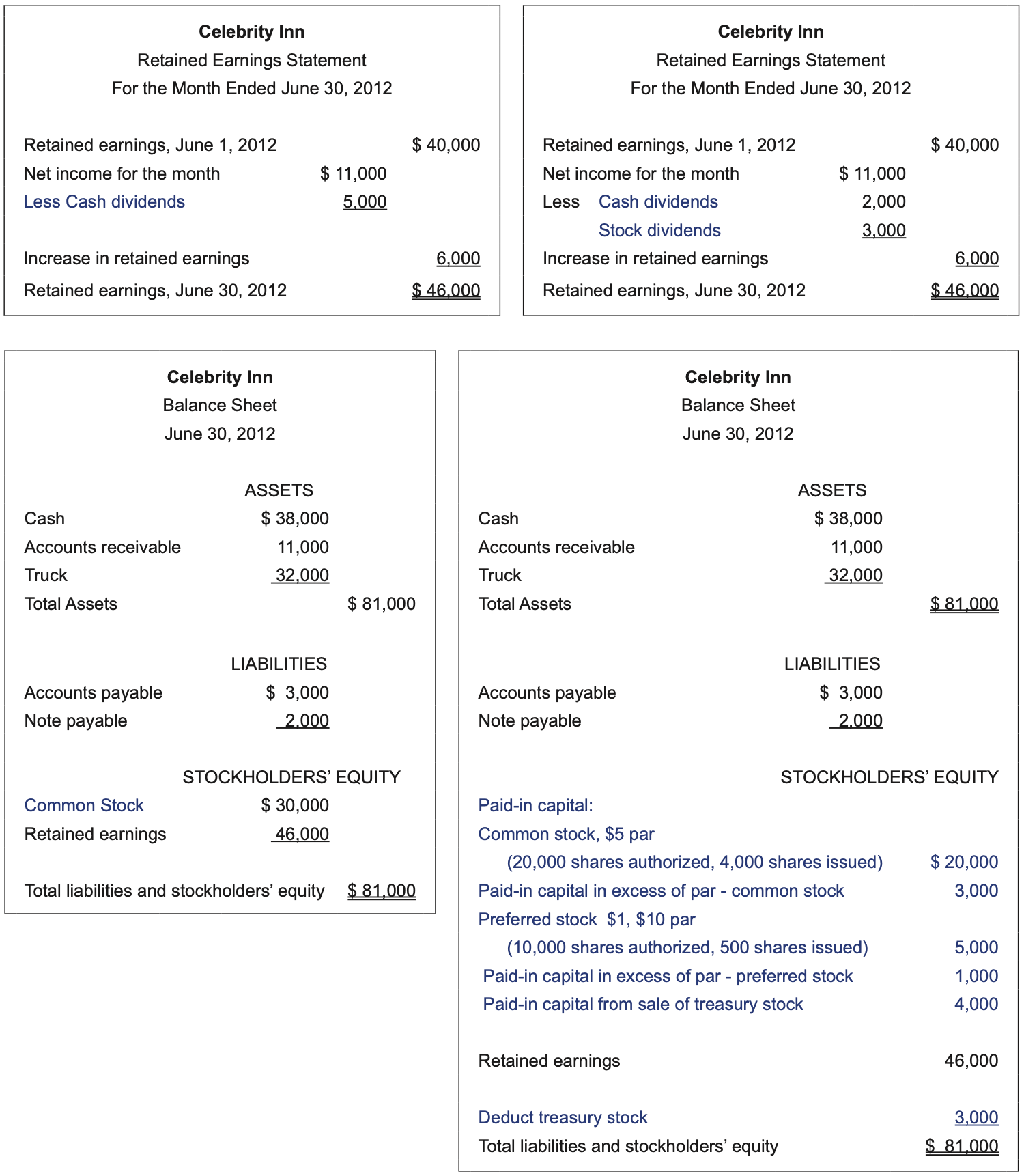

Up to this point, the stockholders’ equity section of the balance sheet has included two accounts: Common Stock and Retained Earnings. Common Stock is value that the owners have in the business because they have contributed their own personal assets. Retained earnings is value the owners have in the corporation because the business has been operating – doing what it was set up to do - and as a result it has generated a profit that the owners share. It is preferable, of course, for stockholder wealth to increase due to net income over time. That earnings potential is, in fact, what attracts stockholders to invest their own money into a business in the first place.

The following Accounts Summary Table summarizes the accounts relevant to issuing stock.

| ACCOUNT TYPE | ACCOUNTS | TO INCREASE | TO DECREASE | NORMAL BALANCE | FINANCIAL STATEMENT | CLOSE OUT? |

| Asset | Organization Costs | debit | credit | debit | Balance Sheet | NO |

| Liability | Cash Dividends Payable | credit | debit | credit | Balance Sheet | NO |

| Stockholders’ Equity |

Common Stock (CS) |

credit | debit | credit | Balance Sheet | NO |

| Contra Stockholders’ Equity | Treasury Stock | debit | credit | debit | Balance Sheet | NO |

| Contra Stockholders’ Equity |

Cash Dividends |

debit | credit | debit | Retained Earnings Statement | YES |

Common Stock, Preferred Stock, and Stock Dividends Distributable amounts can only be in multiples of par value. Use Paid-In Capital in Excess of Par for any differences between issue price and par value.

We will be using the accounts above in numerous journal entries. The point of these journal entries is to ultimately arrive at one number: total stockholders’ equity. Owners of a business are very interested in knowing what they are worth, and that final result is the answer to that question.

The new material we will cover next involves the stockholders’ equity section of the balance sheet. The generic Common Stock account will no longer be the only account used for owner investments: six new accounts will be added that describe a corporation’s equity in more specific detail. In addition, a second type of dividends will be covered: Stock Dividends.

The income statement is not affected by these new accounts. The retained earnings and balance sheet are. The statements on the left show account names in blue that you learned previously. The statements on the right show account names in blue that will replace those on the left as we take a more detailed look at stockholders’ equity.

The first five stockholders’ equity accounts shown on the balance sheet above track owner investments. The total value of these seven account balances is called paid-in capital. Total paid-in capital plus Retained Earnings, which is still used to keep a running balance of a company’s accumulated profit on hand, equals total stockholders’ equity.

Shares authorized is the number of shares a corporation is allowed to issue (sell). For a large corporation this is based on a decision by its Board of Directors, a group elected to represent and serve the interest of the stockholders. Authorization is just permission to sell shares of stock; no action has actually taken place yet. Therefore, there is no journal entry for a stock authorization.

Shares issued is the number of shares a corporation has sold to stockholders for the first time. The number of shares issued cannot exceed the number of shares authorized.

The terms above may be better understood with an analogy to a credit card. If you are approved for a credit card, the terms will include a credit limit, such as $5,000, which is the maximum that you are allowed to charge on the card. This is similar to “shares authorized,” the maximum number of shares a company is allowed to issue. The credit limit on a card does not mean that you have to charge $5,000 on your first purchase, but instead that you may continue to charge purchases up until you have reached a $5,000 maximum. The same holds true for shares issued. Smaller numbers of shares may be sold over time up to the maximum of the number of shares authorized.

If you wish to charge more than your credit limit on a credit card, you may contact the company that issued the card and request an increase in your credit limit. They may or may not grant this request. The same is true for a corporation. If it wishes to issue more shares than the number authorized, it may approach the Board of Directors with this request.