5.3: Notes Payable

- Page ID

- 43089

A business may borrow money from a bank, vendor, or individual to finance operations on a temporary or long-term basis or to purchase assets. Note Payable is used to keep track of amounts that are owed as short-term or long- term business loans.

A note payable is a loan contract that specifies the principal (amount of the loan), the interest rate stated as an annual percentage, and the terms stated in number of days, months, or years. A note payable may be either short term (less than one year) or long term (more than one year).

5.3.1 Short-Term Note Payable

Loans may be short term, due to be repaid by the business within one year. These are current liabilities. There are two types of short-term notes payable: interest bearing and discounted. The difference lies basically in when the borrowerpays the interest to the lender. For an interest-bearing note, the interest is paid at the end of the term of the loan. For a discounted note, the interest is paid up front when the note is issued.

Short-Term Note Payable - Interest Bearing

In the following example, a company issues a 60-day, 12% interest-bearing note for $1,000 to a bank on January 1. The company is borrowing $1,000.

| Date | Account | Debit | Credit | |

| 1/1 | Cash | 1,000 | ▲ Cash is an asset account that is increasing. | |

| Note Payable | 1,000 | ▲ Note Payable is a liability account that is increasing. | ||

Cash is debited to recognize the receipt of the loan proceeds. Note Payable is credited for the principal amount that must be repaid at the end of the term of the loan.

An interest-bearing note payable may also be issued on account rather than for cash. In this case, a company already owed for a product or service it previously was invoiced for on account. Rather than paying the account off on the due date, the company requests an extension and converts the accounts payable to a note payable.

| Date | Account | Debit | Credit | |

| 1/1 | Accounts Payable | 1,000 | ▼ Accounts Payable is a liability account that is decreasing. | |

| Note Payable | 1,000 | ▲ Note Payable is a liability account that is increasing. | ||

At the end of the term of the loan, on the maturity date, the note is void. At that time the Note Payable account must be debited for the principle amount. In addition, the amount of interest charged must be recorded in the journal entry as Interest Expense. The interest amount is calculated using the following equation:

Principal x Rate x Time = Interest Earned

To simplify the math, we will assume every month has 30 days and each year has 360 days.

For a 12% interest rate on a 60-day note, the interest on a 1,000 note would be $20, calculated as follows:

1,000 x 12% x 60/360 = $20

Note that since the 12% is an annual rate (for 12 months), it must be pro- rated for the number of months or days (60/360 days or 2/12 months) in the term of the loan.

On the maturity date, both the Note Payable and Interest Expense accounts are debited. Note Payable is debited because it is no longer valid and its balance must be set back to zero. Interest Expense is debited because it is now a cost of business. Cash is credited since it is decreasing as the loan is repaid.

| Date | Account | Debit | Credit | |

| 2/28 | Note Payable | 1,000 | ▼ Note Payable is a liability account that is decreasing. | |

| Interest Expense | 20 | ▲ Interest Expense is an expense account that is increasing. | ||

| Cash | 1,020 | ▼ Cash is an asset account that is decreasing. |

Short-Term Note Payable - Discounted

In the following example, a company issues a 60-day, 12% discounted note for $1,000 to a bank on January 1. The company is borrowing $1,000.

| Date | Account | Debit | Credit | |

| 1/1 | Cash | 980 | ▲ Cash is an asset account that is increasing. | |

| Interest Expense | 20 | ▲ Interest Expense is an expense account that is increasing. | ||

| Note Payable | 1,000 | ▲ Note Payable is a liability account that is increasing. |

Cash is debited to recognize the receipt of the loan proceeds. Note Payable is credited for the principal amount that must be repaid at the end of the term of the loan.

In addition, the amount of interest charged is recorded as part of the initial journal entry as Interest Expense. The amount of interest reduces the amount of cash that the borrower receives up front.

The interest amount is calculated using the following equation:

Principal x Rate x Time = Interest Earned

To simplify the math, we will assume every month has 30 days and each year has 360 days.

For a 12% interest rate on a 60-day note, the interest on a 1,000 note would be $20, calculated as follows:

1,000 x 12% x 60/360 = $20

Note that since the 12% is an annual rate (for 12 months), it must be pro- rated for the number of months or days (60/360 days or 2/12 months) in the term of the loan.

On the maturity date, only the Note Payable account is debited for the principal amount. Note Payable is debited because it is no longer valid and its balance must be set back to zero. Cash is credited since it is decreasing as the loan is repaid.

| Date | Account | Debit | Credit | |

| 2/28 | Note Payable | 1,000 | ▼ Note Payable is a liability account that is decreasing. | |

| Cash | 1,000 | ▼ Cash is an asset account that is decreasing. |

5.3.2 Long-Term Note Payable

Long-term notes payable are often paid back in periodic payments of equal amounts, called installments. Each installment includes repayment of part of the principal and an amount due for interest. The principal is repaid annually over the life of the loan rather than all on the maturity date.

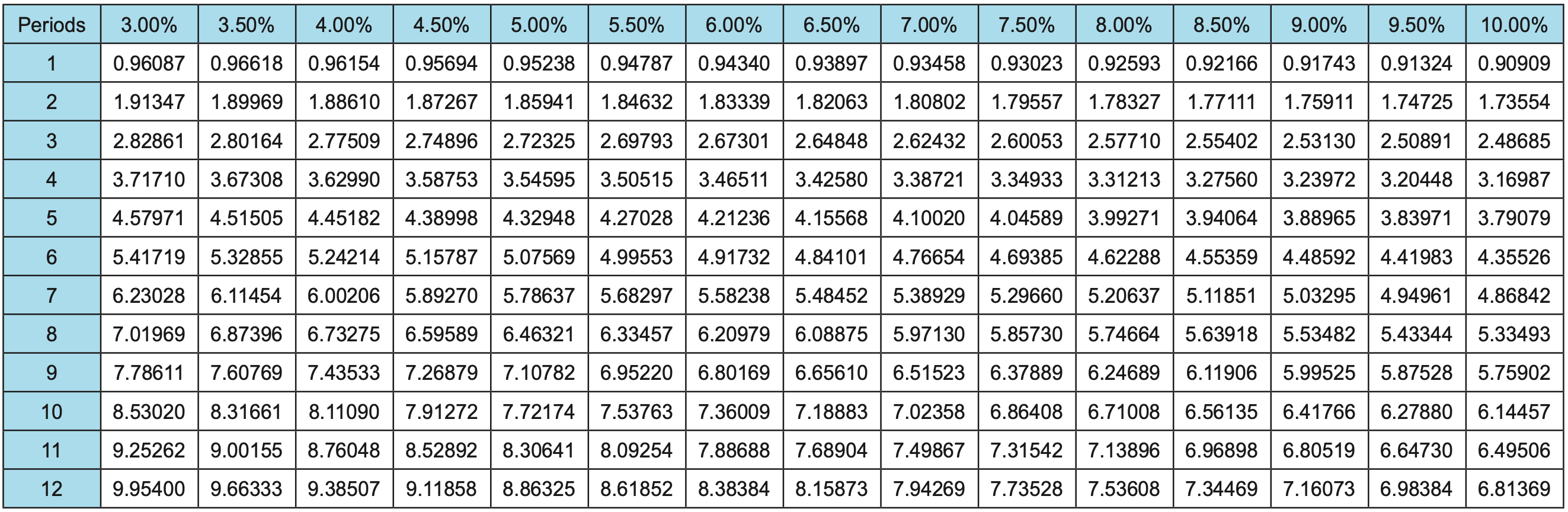

To determine the amount of the annual payment, divide the face amount of the note (the amount borrowed) by one of the factors in the present value of an annuity of $1 to be paid in the future shown in the table below. Select the amount in the table at the intersection of the interest rate and number of years of the loan. For example, a $10,000, 4%, 10-year loan would have an annual payment of $1,232 (rounded to the nearest dollar.) The calculation is 10,000 / 8.11090.

Assume a company borrows $50,000 for five years at an annual interest rate of 5%. The journal entry would be as follows:

| Date | Account | Debit | Credit | |

| 1/1 | Cash | 50,000 | ▲ Cash is an asset account that is increasing. | |

| Note Payable | 50,000 | ▲ Note Payable is a liability account that is increasing. |

Installment payments of $11,549 will be made once a year on December 31. This amount is determined by dividing the $50,000 principal by the present value of an annuity of $1 factor of 4.32948 and rounding to the nearest dollar.

The breakout of the year 1 installment payment of $11,549 is as follows:

Interest on amount owed: $50,000 x 5% = $2,500

Reduction of principal: $11,549 - $2,500 = $9,049

The company owes $40,951 after this payment, which is $50,000 - $9,049.

| Date | Account | Debit | Credit | |

| 12/31 | Note Payable | 9,049 | ▼ Note Payable is a liability account that is decreasing. | |

| Interest Expense | 2,500 | ▲ Interest Expense is an expense account that is increasing. | ||

| Cash | 11,549 | ▼ Cash is an asset account that is decreasing. |

The breakout of the year 2 installment payment of $11,549 is as follows:

Interest on amount owed: $40,951 x 5% = $2,048

Reduction of principal: $11,549 - $2,048 = $9,501

The company owes $31,450 after this payment, which is $40,951 - $9,501.

| Date | Account | Debit | Credit | |

| 12/31 | Note Payable | 9,501 | ▼ Note Payable is a liability account that is decreasing. | |

| Interest Expense | 2,048 | ▲ Interest Expense is an expense account that is increasing. | ||

| Cash | 11,549 | ▼ Cash is an asset account that is decreasing. |

The breakout of the year 3 installment payment of $11,549 is as follows:

Interest on amount owed: $31,450 x 5% = $1,573

Reduction of principal: $11,549 - $1,573 = $9,976

The company owes $21,474 after this payment, which is $31,450 - $9,976.

| Date | Account | Debit | Credit | |

| 12/31 | Note Payable | 9,976 | ▼ Note Payable is a liability account that is decreasing. | |

| Interest Expense | 1,573 | ▲ Interest Expense is an expense account that is increasing. | ||

| Cash | 11,549 | ▼ Cash is an asset account that is decreasing. |

The breakout of the year 4 installment payment of $11,549 is as follows:

Interest on amount owed: $21,474 x 5% = $1,074

Reduction of principal: $11,549 - $1,074 = $10,475

The company owes $10,999 after this payment, which is $21,474 - $10,475.

| Date | Account | Debit | Credit | |

| 12/31 | Note Payable | 10,475 | ▼ Note Payable is a liability account that is decreasing. | |

| Interest Expense | 1,074 | ▲ Interest Expense is an expense account that is increasing. | ||

| Cash | 11,549 | ▼ Cash is an asset account that is decreasing. |

The breakout of the year 5 installment payment of $11,549 is as follows:

Interest on amount owed: $10,999 x 5% = $550

Reduction of principal: $11,549 - $550 = $10,999

The company owes $0 after this payment, which is $10,999 - $10,999.

| Date | Account | Debit | Credit | |

| 12/31 | Note Payable | 10,999 | ▼ Note Payable is a liability account that is decreasing. | |

| Interest Expense | 550 | ▲ Interest Expense is an expense account that is increasing. | ||

| Cash | 11,549 | ▼ Cash is an asset account that is decreasing. |

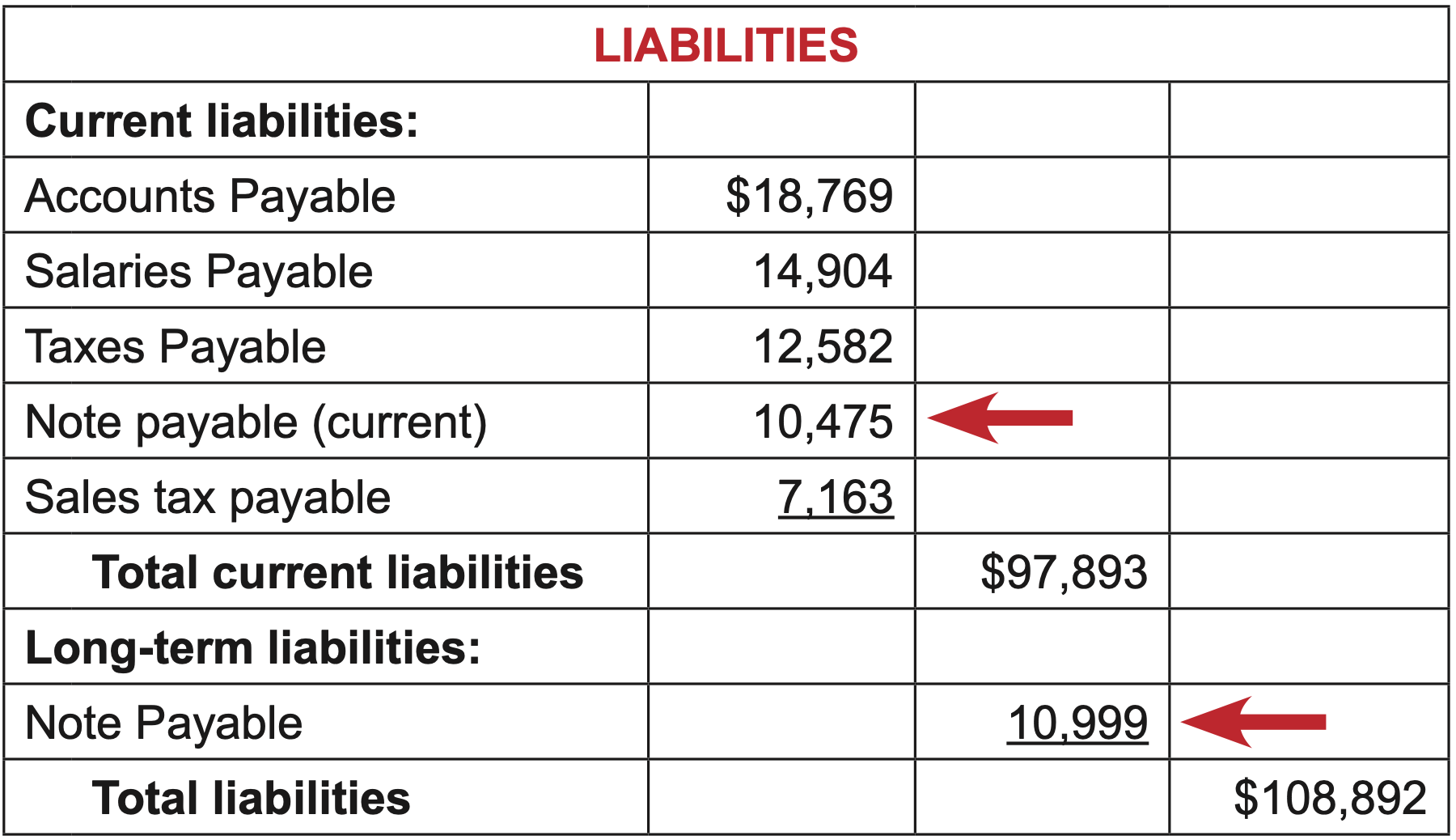

Installments that are due within the coming year are classified as a current liability on the balance sheet. Installments due after the coming year are classified as a long-term liability on the balance sheet.

Using the example above, Notes Payable would be listed on the balance sheet that is prepared at the end of year 3 as follows:

The principal of $10,475 due at the end of year 4—within one year—is current. The principal of $10,999 due at the end of year 5 is classified as long term.