4.4: Uncollectible Accounts

- Page ID

- 43079

When a company extends credit to its customers, it invoices customers and gives them time (usually 30 days) to pay.

SALE ON ACCOUNT: The company debits Accounts Receivable rather than Cash when it sells on account.

| Date | Account | Debit | Credit | ||

| 4/1 | Accounts Receivable | 3,000 | ▲ Accounts Receivable is an asset account that is | ||

| Sales | 3,000 | ▲ Sales is a revenue account that is increasing. | |||

RECEIPT OF PAYMENT: When customers pay off their account within the time allowed, Cash is debited and Accounts Receivable is credited.

| Date | Account | Debit | Credit | ||

| 4/30 | Cash | 3,000 | ▲ Cash is an asset account that is increasing. | ||

| Accounts Receivable | 3,000 | ▼ Accounts Receivable is an asset account that is decreasing. |

The customer has paid the entire amount owed on account and now owes nothing.

However, there may be cases when customers default on their accounts and can or will never pay. If the company is certain that it will never be paid, it can write off the customer’s account and claim the non-payment as a business expense. A write-off is forgiveness of a customer’s debt. This is done only when a company is absolutely certain that a customer can never pay (due to death, bankruptcy, his own admission, etc.)

There are two methods for recording bad debt.

- Direct write-off method—for companies that rarely have bad debt

- Allowance method—for companies that consistently have bad debt

The method a company selects depends on how frequently it anticipates it will experience bad debt. A business such as a movie theater, which primarily accepts cash from customers rather than invoicing them, would not write off bad debt often, if ever. Conversely, a utility company that provides electricity to homeowners constantly must write off bad debt as customers cannot pay or move and do not pay their last bill. The movie theater would select the direct method; the utility company would employ the allowance method.

4.4.1 Direct Write-off Method

The direct write-off method is used by companies that rarely experience any bad debt. A new account—Bad Debt Expense—is an expense account that absorbs this non-payment when the account receivable is closed out. The ONLYaccount that is written off is Accounts Receivable—it is credited to remove the customer’s balance.

SALE ON ACCOUNT: The company debits Accounts Receivable rather than Cash when it sells on account.

| Date | Account | Debit | Credit | ||

| 4/1 | Accounts Receivable | 3,000 | ▲ Accounts Receivable is an asset account that is increasing. | ||

| Sales | 3,000 | ▲ Sales is a revenue account that is increasing. | |||

WRITE-OFF OF ALL OF AN ACCOUNTS RECEIVABLE: If none of what the customer owes will ever be received, Bad Debt Expense is debited instead of Cash to close out the account.

| Date | Account | Debit | Credit | ||

| 4/30 | Bad Debt Expense | 3,000 | ▲ Bad Debt Expense is an expense account that is increasing. | ||

| Accounts Receivable | 3,000 | ▼ Accounts Receivable is an asset account that is decreasing. | |||

WRITE-OFF OF PART OF AN ACCOUNTS RECEIVABLE: If the customer pays some of what he owes but will never be able to pay the rest, the company records the receipt of cash and also writes off the remaining amount that it will never receive. In this case the customer pays $1,000 and the company writes off the remaining $2,000.

| Date | Account | Debit | Credit | ||

| 4/30 | Cash | 1,000 | ▲ Cash is an asset account that is increasing. | ||

| Bad Debt Expense | 2,000 | ▲ Bad Debt Expense is an expense account that is increasing. | |||

| Accounts Receivable | 3,000 | ▼ Accounts Receivable is an asset account that is decreasing. |

REINSTATEMENT OF FULL AMOUNT: If, for some reason, the customer returns to pay his entire bill AFTER the write-off, just “flip over” the previous transaction to void it. This is called reinstating. Then make the journal entry to collect the cash. Note that there are two journal entries for a reinstatement.

| Date | Account | Debit | Credit | ||

| 6/17 | Accounts Receivable | 3,000 | ▲ Accounts Receivable is an asset account that is increasing. | ||

| Bad Debt Expense | 3,000 | ▼ Bad Debt Expense is an expense account that is decreasing. | |||

| Cash | 3,000 | ▲ Cash is an asset account that is increasing. | |||

| Accounts Receivable | 3,000 | ▼ Accounts Receivable is an asset account that is decreasing. |

REINSTATEMENT OF PARTIAL AMOUNT: If, for some reason, the customer returns to pay only part of what he owed AFTER the write-off (for example, $1,000), just “flip over” the previous transaction to void it. This is called reinstating. Then make the journal entry to collect the cash. Only include the amount the customer repays, not the entire amount that was written off

| Date | Account | Debit | Credit | ||

| 6/17 | Accounts Receivable | 1,000 | ▲ Accounts Receivable is an asset account that is increasing. | ||

| Bad Debt Expense | 1,000 | ▼ Bad Debt Expense is an expense account that is decreasing. | |||

| Cash | 1,000 | ▲ Cash is an asset account that is increasing. | |||

| Accounts Receivable | 1,000 | ▼ Accounts Receivable is an asset account that is decreasing. |

4.4.2 Allowance Method

The allowance method is used by companies that frequently experience bad debt. A new account—Allowance for Doubtful Accounts—is a contra asset account that absorbs this non-payment when the account receivable is closed out.

An allowance is an estimate. Companies that have continuous bad debt make an adjusting entry at the beginning of the year to estimate how much of its Accounts Receivable it believes it will never collect due to non-payment. This is recorded before any customer’s account actually defaults during the year.

ADJUSTING ENTRY TO SET UP BAD DEBT ESTIMATE of $15,000 FOR THE YEAR: A credit to Allowance for Doubtful Accounts increases it, since it is a contra asset. NOTE: The only time Bad Debt Expense is used under the allowance method is in the annual adjusting entry. There are two ways of estimating the amount of bad debt for the upcoming year; these will be discussed shortly.

| Date | Account | Debit | Credit | ||

| 1/1 | Bad Debt Expense | 15,000 | ▲ Bad Debt Expense is an expense account that is increasing. | ||

| Allowance for Doubtful Accounts | 15,000 | ▲ Allow Doubt Accts is a contra asset account that is increasing. |

SALE ON ACCOUNT: The company debits Accounts Receivable rather than Cash when it sells on account.

| Date | Account | Debit | Credit | ||

| 4/1 | Accounts Receivable | 3,000 | ▲ Accounts Receivable is an asset account that is increasing. | ||

| Sales | 3,000 | ▲ Sales is a revenue account that is increasing. | |||

WRITE-OFF OF ALL OF AN ACCOUNTS RECEIVABLE: If none of what the customer owes will ever be received, Allowance for Doubtful Accounts is debited instead of Cash to close out the account.

| Date | Account | Debit | Credit | ||

| 4/30 | Allowance Doubtful Accounts | 3,000 | ▼ Allow Doubt Accts is a contra asset account that is decreasing. | ||

| Accounts Receivable | 3,000 | ▼ Accounts Receivable is an asset account that is decreasing. | |||

WRITE-OFF OF PART OF AN ACCOUNTS RECEIVABLE: If the customer pays some of what he owes but will never be able to pay the rest, the company records the receipt of cash and also writes off the remaining amount that it will never receive. In this case the customer pays $1,000 and the company writes off the remaining $2,000.

| Date | Account | Debit | Credit | ||

| 4/30 | Cash | 1,000 | ▲ Cash is an asset account that is increasing. | ||

| Allowance Doubtful Accounts | 2,000 | ▼ Allow Doubt Accts is a contra asset account that is decreasing. | |||

| Accounts Receivable | 3,000 | ▼ Accounts Receivable is an asset account that is decreasing. |

REINSTATEMENT OF FULL AMOUNT: If, for some reason, the customer returns to pay his entire bill AFTER the write-off, just “flip over” the previous transaction to void it. This is called reinstating. Then make the journal entry to collect the cash. Note that there are two journal entries for a reinstatement.

| Date | Account | Debit | Credit | ||

| 6/17 | Accounts Receivable | 3,000 | ▲ Accounts Receivable is an asset account that is increasing. | ||

| Allowance for Doubtful Accounts | 3,000 | ▲ Allow Doubt Accts is a contra asset account that is increasing. | |||

| Cash | 3,000 | ▲ Cash is an asset account that is increasing. | |||

| Accounts Receivable | 3,000 | ▼ Accounts Receivable is an asset account that is decreasing. |

REINSTATEMENT OF PARTIAL AMOUNT: If, for some reason, the customer returns to pay only part of what he owed AFTER the write-off (for example, $1,000), just “flip over” the previous transaction to void it. This is called reinstating. Then make the journal entry to collect the cash. Only include the amount the customer repays, not the entire amount that was written off.

| Date | Account | Debit | Credit | ||

| 6/17 | Accounts Receivable | 1,000 | ▲ Accounts Receivable is an asset account that is increasing. | ||

| Allowance for Doubtful Accounts | 1,000 | ▲ Allow Doubt Accts is a contra asset account that is increasing. | |||

| Cash | 1,000 | ▲ Cash is an asset account that is increasing. | |||

| Accounts Receivable | 1,000 | ▼ Accounts Receivable is an asset account that is decreasing. |

Net Realizable Value is the amount of a company’s total Accounts Receivable that it expects to collect. It is calculated and appears on the Balance Sheet as follows:

| Less: |

Accounts Receivable Allowance for Doubtful Accounts Net Realizable Value |

$97,000 12,000 \(\ \overline{$85,000}\) |

(amount owed to a company) (amount the company expects will “go bad”) |

In fairness to the readers of the balance sheet, the company admits on the balance sheet that even though it is owed $97,000 from customers (an asset), it does not expect to ever receive $12,000 of it. The Accounts Receivable andAllowance for Doubtful Accounts amounts on the balance sheet are the current ledger balances.

Allowance Method - Analysis of Receivables

The allowance method is used by companies that frequently experience bad debt. An allowance is an estimate. Companies that have continuous bad debt make an adjusting entry at the beginning of the year to estimate how much of its Accounts Receivable it believes it will never collect due to non-payment.

The question now is this: How is the amount of the adjusting entry determined?

Sample: ADJUSTING ENTRY TO SET UP BAD DEBT ESTIMATE FOR THE YEAR

| Date | Account | Debit | Credit | ||

| 1/1 | Bad Debt Expense | ????? | ▲ Bad Debt Expense is an expense account that is increasing. | ||

| Allowance for Doubtful Accounts | ????? | ▲ Allow Doubt Accts is a contra asset account that is increasing. | |||

There are two ways to arrive at the estimate for the upcoming year (the amount of the adjusting entry) under the allowance method. These are analysis of receivables and percent of sales.

- Analysis of receivables involves analyzing and/or contacting all customers, determining who is likely to default and adding the amounts for all customers who are likely to become bad debt. The adjusting entry should include the amount necessary to bring the Allowance for Doubtful Accounts ledger balance up to this number.

In the three examples that follow, assume that after analyzing receivables on 1/1, it is estimated that there will be $8,000 of bad debt during the upcoming year.

Example 1 – Analysis of Receivables: No balance in the Allowance for Doubtful Accounts ledger.

| Date | Item | Debit | Credit | Debit | Credit | |

| 1/1 | Balance | Since there is no balance in the account “left over” from last year, it will take a credit of $8,000 to bring the year’s beginning balance up to $8,000. | ||||

| Date | Account | Debit | Credit | ||

| 1/1 | Bad Debt Expense | 8,000 | ▲ Bad Debt Expense is an expense account that is increasing. | ||

| Allowance for Doubtful Accounts | 8,000 | ▲ Allow Doubt Accts is a contra asset account that is increasing. | |||

| Date | Item | Debit | Credit | Debit | Credit | |

| 1/1 | 8,000 | 8,000 | The adjusting entry for the estimate brings the Accumulated Depreciation credit balance to $8,000 | |||

Example 2– Analysis of Receivables: A $600 credit balance in the Allowance for Doubtful Accounts ledger.

This means that the company overestimated its Bad Debt Expense last year—it had less bad debt than it had estimated it would have.

| Date | Item | Debit | Credit | Debit | Credit | |

| 1/1 | Balance | 600 | Since there is already a $600 credit balance in the account “left over” from last year, it will only take an additional credit of $7,400 to bring the year’s beginning balance up to $8,000. | |||

| Date | Account | Debit | Credit | ||

| 1/1 | Bad Debt Expense | 7,400 | ▲ Bad Debt Expense is an expense account that is increasing. | ||

| Allowance for Doubtful Accounts | 7,400 | ▲ Allow Doubt Accts is a contra asset account that is increasing. | |||

| Date | Item | Debit | Credit | Debit | Credit | |

| 1/1 | Balance | 600 | The adjusting entry for the estimate brings the Accumulated Depreciation credit balance to $8,000. | |||

| 1/1 | 7,400 | 8,000 | ||||

Example 3– Analysis of Receivables: A $600 debit balance in the Allowance for Doubtful Accounts ledger.

This means that the company underestimated its Bad Debt Expense last year— it had more bad debt than it had estimated it would have.

| Date | Item | Debit | Credit | Debit | Credit | |

| 1/1 | Balance | 600 | Since there is already a $600 debit balance in the account “left over” from last year, it will take an additional credit of $8,600 to bring the year’s beginning balance up to $8,000. | |||

| Date | Account | Debit | Credit | ||

| 1/1 | Bad Debt Expense | 8,600 | ▲ Bad Debt Expense is an expense account that is increasing. | ||

| Allowance for Doubtful Accounts | 8,600 | ▲ Allow Doubt Accts is a contra asset account that is increasing. | |||

| Date | Item | Debit | Credit | Debit | Credit | |

| 1/1 | Balance | 600 | The adjusting entry for the estimate brings the Accumulated Depreciation credit balance to $8,000. | |||

| 1/1 | 8,600 | 8,000 | ||||

Allowance Method - Percent of Sales

- Percent of Sales involves a simple calculation: Sales on account in previous year times the historical percent of sales that default. The adjusting entry should include the result of the calculation; the credit to Allowance for Doubtful Accounts increases the account’s ledger balance.

In the three examples below assume that sales on account for the previous year were $400,000 and an estimated 2% of those sales will have to be written off. The amount of $8,000, which his $400,000 x 2%, is the amount that will be entered in the adjusting entry for the estimate.

Example 1 – Percent of Sales: No balance in the Allowance for Doubtful Accounts ledger.

| Date | Item | Debit | Credit | Debit | Credit | |

| 1/1 | Balance | There is no balance in the account “left over” from last year. | ||||

| Date | Account | Debit | Credit | $400,000 x 2% = $8,000 | |

| 1/1 | Bad Debt Expense | 8,000 | ▲ Bad Debt Expense is an expense account that is increasing. | ||

| Allowance for Doubtful Accounts | 8,000 | ▲ Allow Doubt Accts is a contra asset account that is increasing. |

| Date | Item | Debit | Credit | Debit | Credit | |

| 1/1 | 8,000 | 8,000 | The adjusting entry for the estimate brings the Allowance for Doubtful Accounts credit balance to $8,000. | |||

Example 2– Percent of Sales: A $600 credit balance in the Allowance for Doubtful Accounts ledger.

This means that the company overestimated its Bad Debt Expense last year—it had less bad debt than it had estimated it would have.

| Date | Item | Debit | Credit | Debit | Credit | |

| 1/1 | Balance | 600 | There is a $600 credit balance in the account “left over” from last year. | |||

| Date | Account | Debit | Credit | $400,000 x 2% = $8,000 | |

| 1/1 | Bad Debt Expense | 8,000 | ▲ Bad Debt Expense is an expense account that is increasing. | ||

| Allowance for Doubtful Accounts | 8,000 | ▲ Allow Doubt Accts is a contra asset account that is increasing. | |||

| Date | Item | Debit | Credit | Debit | Credit | |

| 1/1 | Balance | 600 | The adjusting entry for the estimate adds the additional $8,000 to the previous credit balance. | |||

| 1/1 | 8,000 | 8,600 | ||||

Example 3– Percent of Sales: A $600 debit balance in the Allowance for Doubtful Accounts ledger.

This means that the company underestimated its Bad Debt Expense last year— it had more bad debt than it had estimated it would have.

| Date | Item | Debit | Credit | Debit | Credit | |

| 1/1 | Balance | 600 | There is a $600 debit balance in the account “left over” from last year. | |||

| Date | Account | Debit | Credit | $400,000 x 2% = $8,000 | |

| 1/1 | Bad Debt Expense | 8,000 | ▲ Bad Debt Expense is an expense account that is increasing. | ||

| Allowance for Doubtful Accounts | 8,000 | ▲ Allow Doubt Accts is a contra asset account that is increasing. | |||

| Date | Item | Debit | Credit | Debit | Credit | |

| 1/1 | Balance | 600 | The adjusting entry for the estimate adds the additional $8,000 to the previous debit balance. | |||

| 1/1 | 8,000 | 7,400 | ||||

The following table summaries the new asset accounts.

| ACCOUNT TYPE | ACCOUNTS | TO INCREASE | TO DECREASE | NORMAL BALANCE | FINANCIAL STATEMENT | CLOSE OUT? |

| Asset | Accounts Receivable Notes Receivable | debit | credit | debit | Balance Sheet | NO |

| Contra Asset | Allowance for Doubtful Accounts | credit | debit | credit | Balance Sheet | NO |

| Revenue | Interest Revenue | credit | debit | credit | Income Statement | YES |

| Expense | Bad Debt Expense | debit | credit | debit | Income Statement | YES |

| Topics – The basic accounting cycle | Fact | Journal Entry | Calculate Amount | Format |

| Concept of short-term loans | x | |||

| Review sales transactions on account | x | |||

| Journalize the receipt of a note receivable for cash | x | x | ||

| Journalize the receipt of a note receivable on account | x | x | ||

| Journalize the receipt of payment for a note due | x | x | ||

| Journalize the receipt of a new note for a note due | x | x | ||

| Journalize a dishonored note | x | x | ||

| Journalize the receipt of payment on a dishonored note | x | x | ||

| Concept of bad debt and write-offs | x | |||

| Journalize a full write-off under the direct write-off method | x | x | ||

| Journalize a partial write-off under the direct write-off method | x | x | ||

| Journalize a full reinstatement under the direct write-off method | x | x | ||

| Journalize a partial reinstatement under the direct write-off method | x | x | ||

| Journalize bad debt estimates using an analysis of receivables | x | x | ||

| Journalize a full write-off under the allowance method | x | x | ||

| Journalize a partial write-off under the allowance method | x | x | ||

| Journalize a full reinstatement under the allowance method | x | x | ||

| Journalize a partial reinstatement under the allowance method | x | x | ||

| Journalize bad debt estimates using percent of sales | x | x | ||

| Financial statements | x | x | ||

| Journalize closing entries | x | |||

| Post closing entries to ledgers | x |

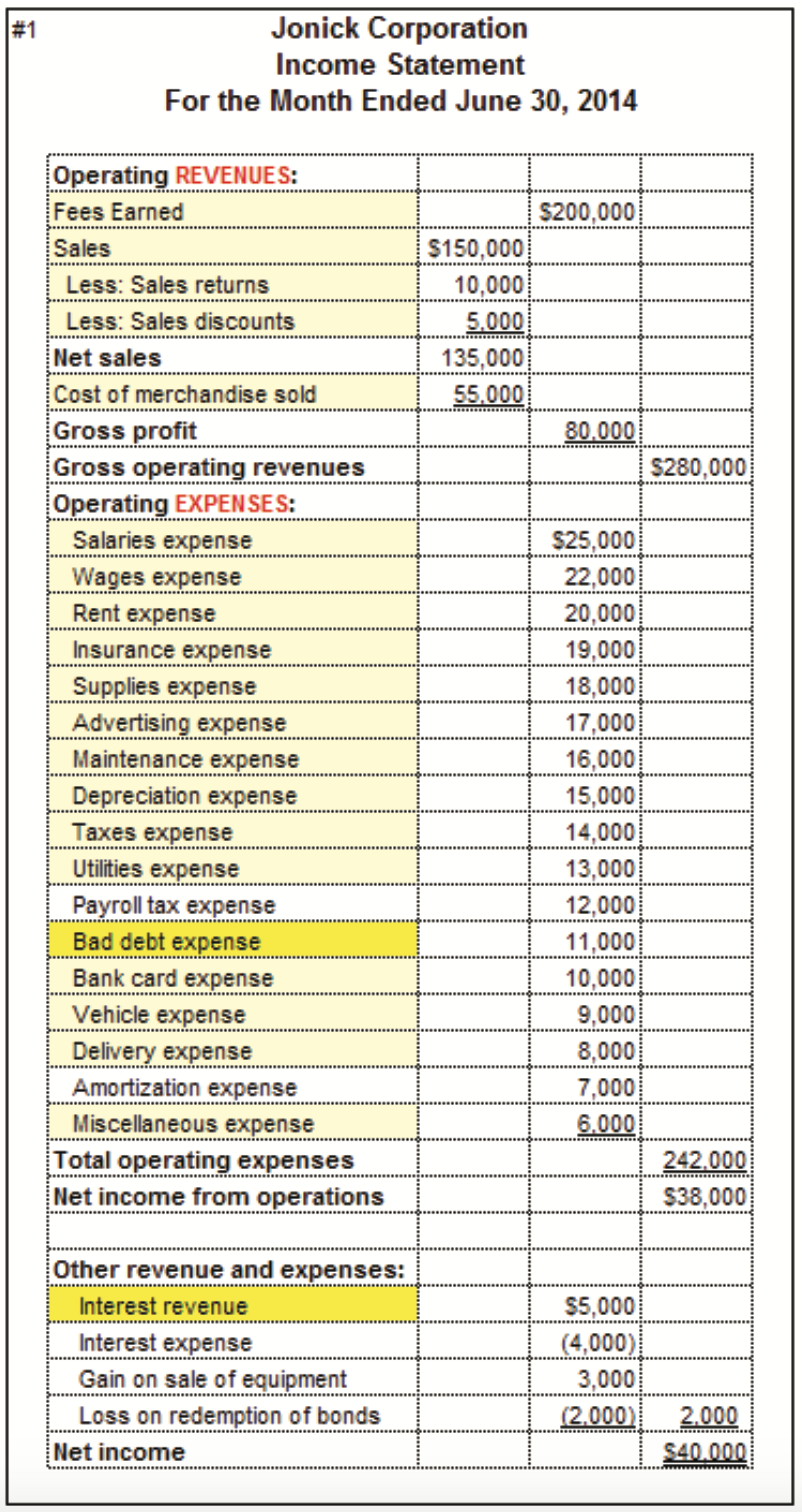

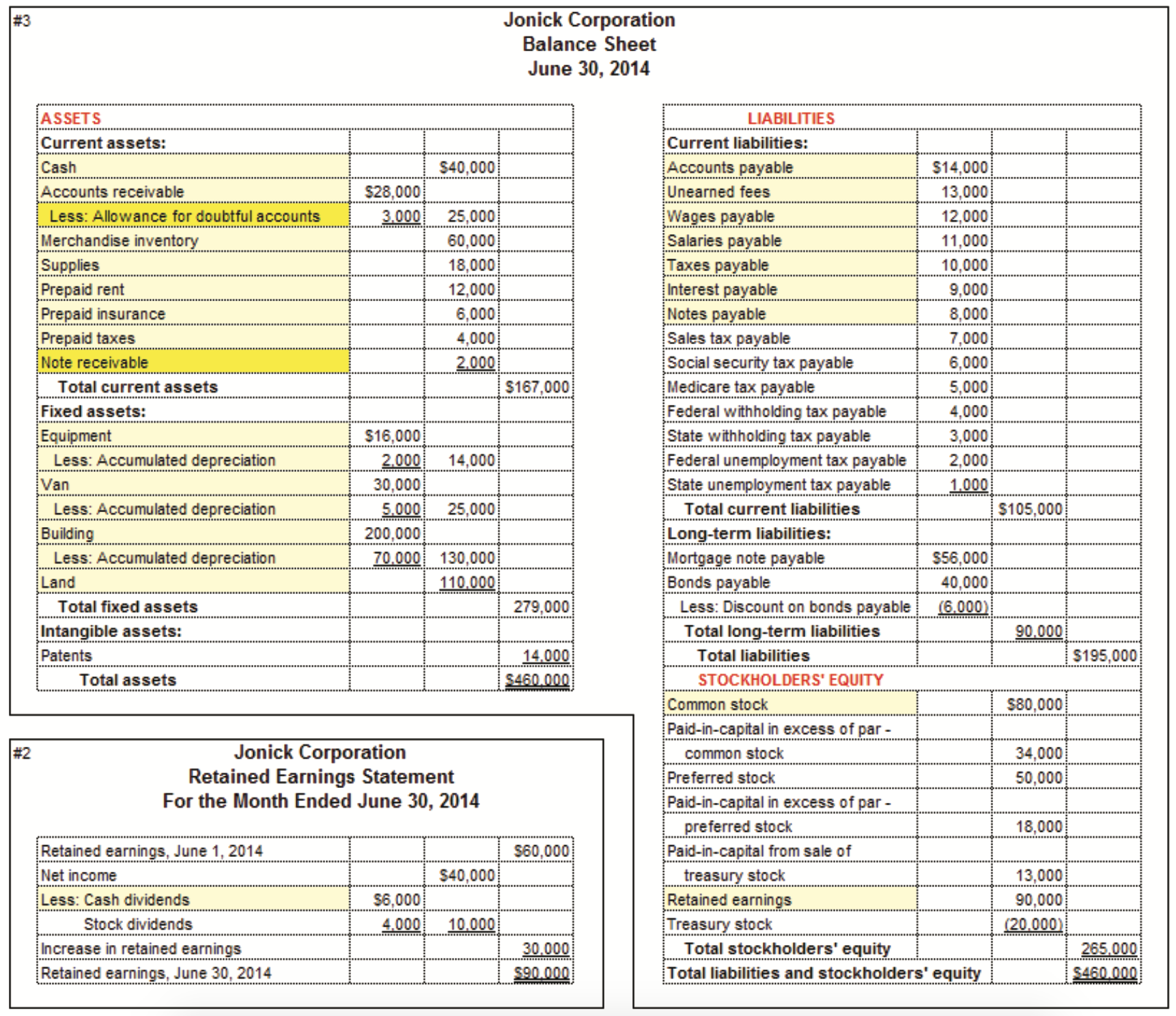

The accounts that are highlighted in bright yellow are the new accounts you just learned. Those highlighted in light yellow are the ones you learned previously.