2.2: Matching Principle

- Page ID

- 43064

The matching principle relates to income statement accounts. It states that expenses incurred during a period should relate to (or match up with) the revenues earned during the same period. This lets you know how much it cost you to produce the revenue you generated in a given period of time, such as a month.

You have probably heard that “It takes money to make money.” A business person contributes financial resources and hopefully uses them effectively to generate even more value. The matching principle looks at a window of time in terms of how much income came in and how much it cost to generate that income. The key here is the “window of time,” such as a month. It compares how much came in in sales in a month vs. how much was spent. Any revenue or expenses before that month or after that month are not considered.

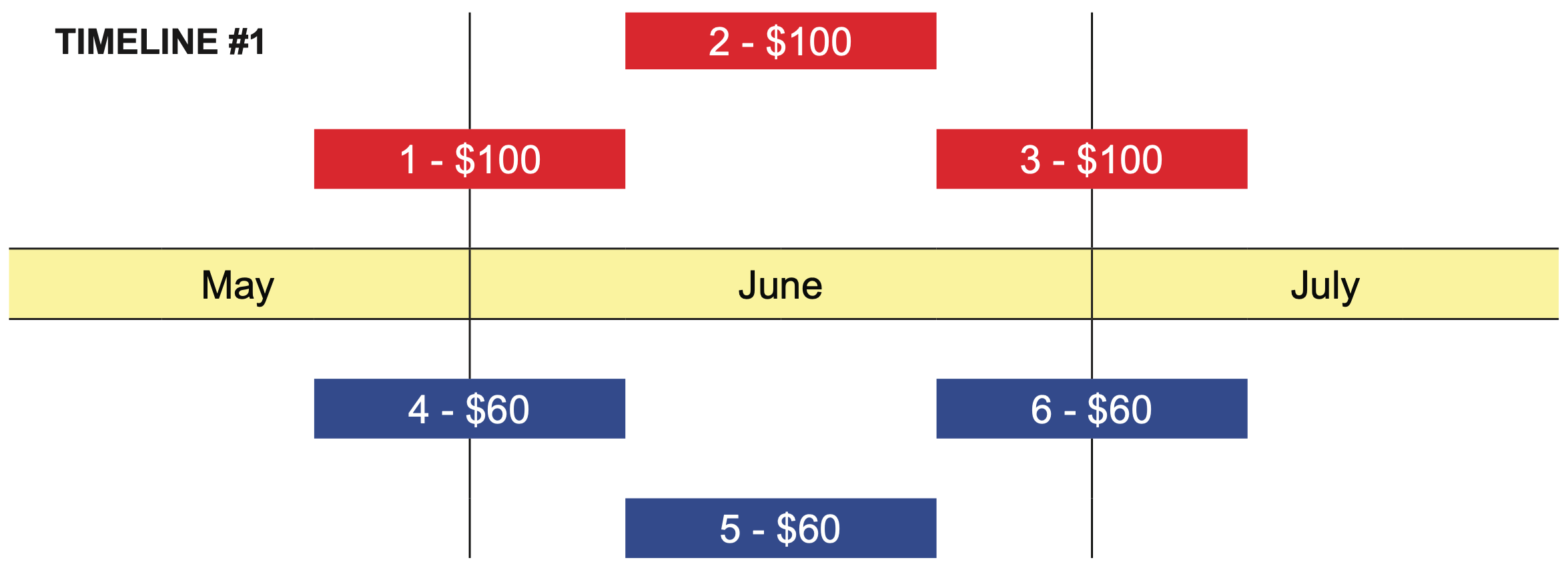

Below is Timeline #1, which includes three months. The red bars represent revenue—three different jobs for $100 each. Job 1 was started in May and completed in June. Job 2 was started in June and completed in June. Job 3 was started in June and was completed in July. There was a total of $300 in revenue from these three jobs, but not all of it is earned in June. As you can see, only half of the revenue from Jobs 1 and 3 was earned in June.

The blue bars represent expenses. Expense 4 began in May and was incurred partially in May and partially in June. Expense 5 began in June and all of this expense was incurred in June. Expense 6 also began in June; some of it was incurred in June and some in July. There was a total of $180 of expenses, but not all of it was incurred in June. As you can see, only half of the expenses from Jobs 1 and 3 was incurred in June.

Let’s say we want to produce an income statement for June, our window of time. We want to include all the revenue and expenses that occurred in June, but none that occurred in May or July. We have to “chop off” the pieces of these transactions that did not occur in June to be left with only the parts that belong in June.

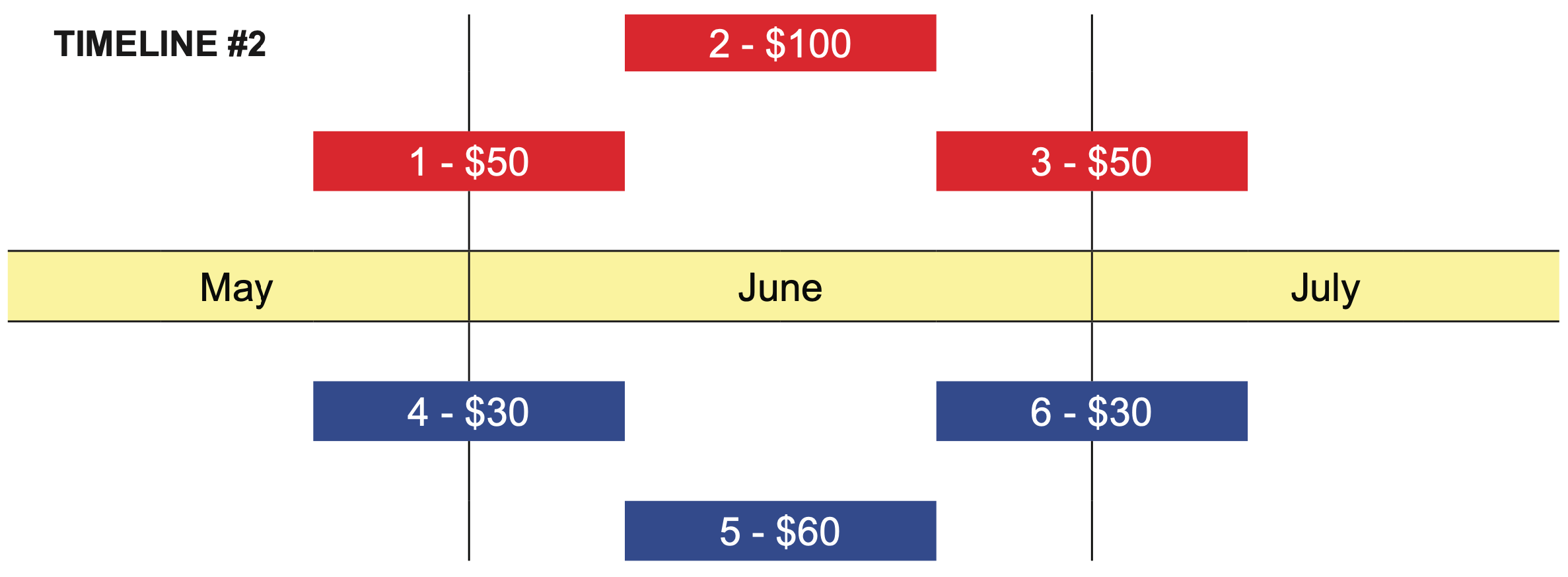

The result appears in the Timeline #2 below. In June, $200 of revenue ($50 + $100 + $50) was earned and is matched with $120 ($30 + $60 +$30) of expenses that were incurred in the same month. The net income for June, therefore, was $80 ($200 - $120).

Adjusting entries, discussed next, help do the job of matching the June revenue with the June expenses by “chopping” off amounts of transactions that do not belong in a given month.

2.2.1 Adjusting Entries

Adjusting entries are special entries made just before financial statements are prepared—at the end of the month and/or year. They bring the balances of certain accounts up to date if they are not already current to properly match revenues and expenses. So far we have dealt with companies that did not need adjusting entries under the cash basis of accounting. Now we will see situations where they are necessary and will be using the accrual basis of accounting.

Many ledger account balances are already correct at the end of the accounting period; however, some account balances may have changed during the period and but have not yet been updated. This is what you will do by making adjustingentries, and this will ensure that your financial statement numbers are current and correct. Adjusting entries are typically necessary for transactions that extend over more than one accounting period—you want to include the part of the transaction that belongs in the one accounting period you are preparing financial statements for and exclude that part that belongs in a previous or future accounting period. This relates to the matching process.

IMPORTANT: Each adjusting entry will always affect at least one income statement account (revenue or expense) and one balance sheet account (asset or liability).

2.2.2 Complete Accounting Cycle

Accounting is a cyclical process. It involves a series of steps that take place in a particular order during a period of time. Once this period of time is over, these same steps are repeated in the next period of time of equal length.

The complete accounting cycle involves these nine steps, done in this order:

| ACTION | WHEN | YOUR JOB | |

| 1. | Journalize transactions | Daily | THINK |

| 2. | Post to ledgers | Daily | COPY from journal; CALCULATE |

| 3. | Journalize the adjusting entries | End of month | THINK |

| 4. | Post the adjusting entries | End of month | COPY from journal; CALCULATE |

| 5. | Income statement | End of month | COPY from ledgers; CALCULATE |

| 6. | Retained earnings statement | End of month | COPY net income from income statement |

| 7. | Balance sheet | End of month | COPY from ledgers; ADD |

| 8. | Journalize the closing entries | End of month | THINK (same three entries) |

| 9. | Post the closing entries | End of month | COPY from journal; CALCULATE |

You have already learned how to complete seven of the steps. The remaining two steps, #3 and #4, are new and involve adjusting entries that update account balances that are not current just before preparing the financial statements.

IMPORTANT: Notice that adjusting entries are recorded BEFORE the financial statements are prepared and closing entries are recorded AFTER financial statements are prepared.

2.2.3 Adjusting Entry Accounts

The following list includes accounts whose balances may need to be brought up to date in the 10 adjusting entry transactions we will cover.

| ACCOUNT TYPE | ACCOUNTS | TO INCREASE | TO DECREASE | NORMAL BALANCE | FINANCIAL STATEMENT | CLOSE OUT? |

| Asset | Accounts Receivable Supplies Prepaid Rent Prepaid Insurance Prepaid Taxes Prepaid ANYTHING |

debit | credit | debit | Balance Sheet | NO |

| Contra Asset | Accumulated Depreciation | credit | debit | credit | Balance Sheet | NO |

| Liability | Wages Payable Taxes Payable Interest Payable ANY Payable Unearned Fees Unearned Rent Unearned ANYTHING |

credit | debit | credit | Balance Sheet | NO |

| Revenue | Fees Earned Rent Revenue |

credit | debit | credit | Income Statement | YES |

| Expense | Wages Expense Rent Expense Supplies Expense Insurance Expense Depreciation Expense Taxes Expense Interest Expense |

debit | credit | debit | Income Statement | YES |

Here are the 10 adjusting entries we will cover.

| Date | Account | Debit | Credit | ||

| 6/30 | Supplies Expense | 100 | ▲ Supplies Expense is an expense account that is increasing. | ||

| Supplies | 100 | ▼ Supplies is an asset account that is decreasing. | |||

| 6/30 | Insurance Expense | 100 | ▲ Insurance Expense is an expense account that is increasing. | ||

| Prepaid Insurance | 100 | ▼ Prepaid Insurance is an asset account that is decreasing. | |||

| 6/30 | Rent Expense | 100 | ▲ Rent Expense is an expense account that is increasing. | ||

| Prepaid Rent | 100 | ▼ Prepaid Rent is an asset account that is decreasing. | |||

| 6/30 | Taxes Expense | 100 | ▲ Taxes Expense is an expense account that is increasing. | ||

| Prepaid Taxes | 100 | ▼ Prepaid Taxes is an asset account that is decreasing. | |||

| 6/30 | Depreciation Expense | 100 | ▲ Depreciation Expense is an expense account that is increasing. | ||

| Accumulated Depreciation | 100 | ▲ Accumulated Depreciation is a contra asset account that is increasing. | |||

| 6/30 | Unearned Fees | 100 | ▼ Unearned Fees is a liability account that is decreasing. | ||

| Fees Earned | 100 | ▲ Fees Earned is a revenue account that is increasing. | |||

| 6/30 | Wages Expense | 100 | ▲ Wages Expense is an expense account that is increasing. | ||

| Wages Payable | 100 | ▲ Wages Payable is a liability account that is increasing. | |||

| 6/30 | Taxes Expense | 100 | ▲ Taxes Expense is an expense account that is increasing. | ||

| Taxes Payable | 100 | ▲ Taxes Payable is a liability account that is increasing. | |||

| 6/30 | Interest Expense | 100 | ▲ Interest Expense is an expense account that is increasing. | ||

| Interest Payable | 100 | ▲ Interest Payable is a liability account that is increasing. | |||

| 6/30 | Accounts Receivable | 100 | ▲ Accounts Receivable is an asset account that is increasing. | ||

| Fees Earned | 100 | ▲ Fees Earned is a revenue account that is increasing. | |||

From this point we will go into a more detailed discussion of each of these adjusting entries above.