1.2: Distinguish between Financial and Managerial Accounting

- Page ID

- 5180

Now that you have a basic understanding of managerial accounting, consider how it is similar to and different from financial accounting. After completing a financial accounting class, many students do not look forward to another semester of debits, credits, and journal entries. Thankfully, managerial accounting is much different from financial accounting. Also known as management accounting or cost accounting, managerial accounting provides information to managers and other users within the company in order to make more informed decisions. The overriding roles of managers (planning, controlling, and evaluating) lead to the distinction between financial and managerial accounting. The main objective of management accounting is to provide useful information to managers to assist them in the planning, controlling, and evaluating roles.

Unlike managerial accounting, financial accounting is governed by rules set out by the Financial Accounting Standards Board (FASB), an independent board made up of accounting professionals who determine and publicize the standards of financial accounting and reporting in the United States. Larger, publicly traded companies are also governed by the US Securities and Exchange Commission (SEC), in the form of the generally accepted accounting principles (GAAP), the common set of rules, standards, and procedures that publicly traded companies must follow when they are composing their financial statements.

Financial accounting provides information to enable stockholders, creditors, and other stakeholders to make informed decisions. This information can be used to evaluate and make decisions for an individual company or to compare two or more companies. However, the information provided by financial accounting is primarily historical and therefore is not sufficient and is often synthesized too late to be overly useful to management. Managerial accounting has a more specific focus, and the information is more detailed and timelier. Managerial accounting is not governed by GAAP, so there is unending flexibility in the types of reports and information gathered. Managerial accountants regularly calculate and manage “what-if” scenarios to help managers make decisions and plan for future business needs. Thus, managerial accounting focuses more on the future, while financial accounting focuses on reporting what has already happened. In addition, managerial accounting uses nonfinancial data, whereas financial accounting relies solely on financial data.

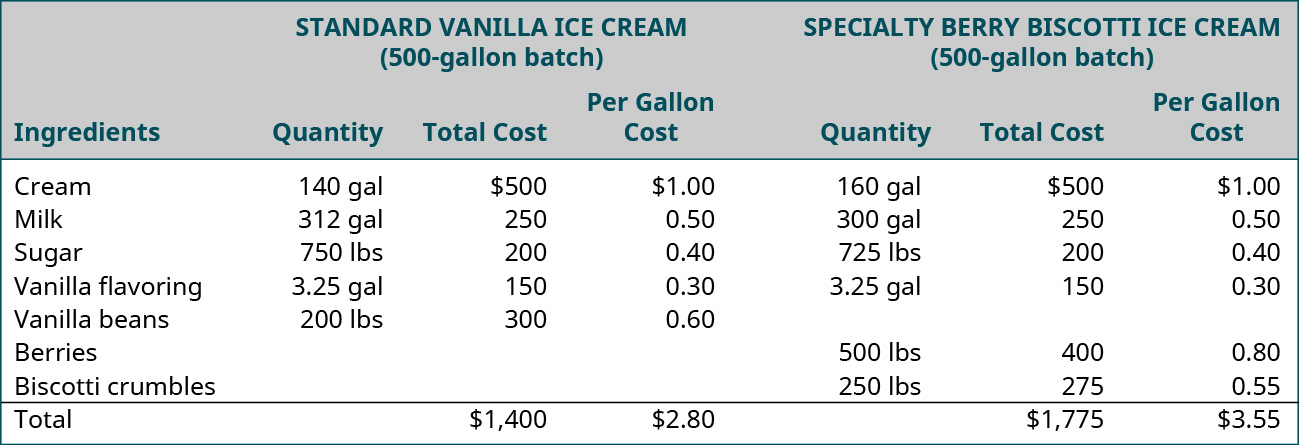

For example, Daryn’s Dairy makes many different organic dairy products. Daryn’s managers need to track their costs for certain jobs. One of the company’s top-selling ice creams is their seasonal variety; a new flavor is introduced every three months and sold for only a six-month period. The cost of these specialty ice creams is different from the cost of the standard flavors for reasons such as the unique or expensive ingredients and the specialty packaging. Daryn wants to compare the costs involved in making the specialty ice cream and those involved in making the standard flavors of ice cream. This analysis will require that Daryn track not only the cost of materials that go into the product, but also the labor hours and cost of the labor, plus other costs, known as overhead costs (rent, electricity, insurance, etc.), that are incurred in producing the various ice creams. Once the total costs for both the specialty ice cream and the standard flavored ice cream are known, the cost per unit can be determined for each type. These types of analyses help a company evaluate how to set pricing, evaluate the need for new or substitute ingredients, manage product additions and deletions, and make many other decisions. Figure \(\PageIndex{1}\) shows an example of a materials cost analysis by Daryn’s Dairy used to compare the materials cost for producing \(500\) gallons of their best-selling standard flavor—vanilla—with one of their specialty ice creams—Very Berry Biscotti.

Financial and Managerial Accounting Comparative

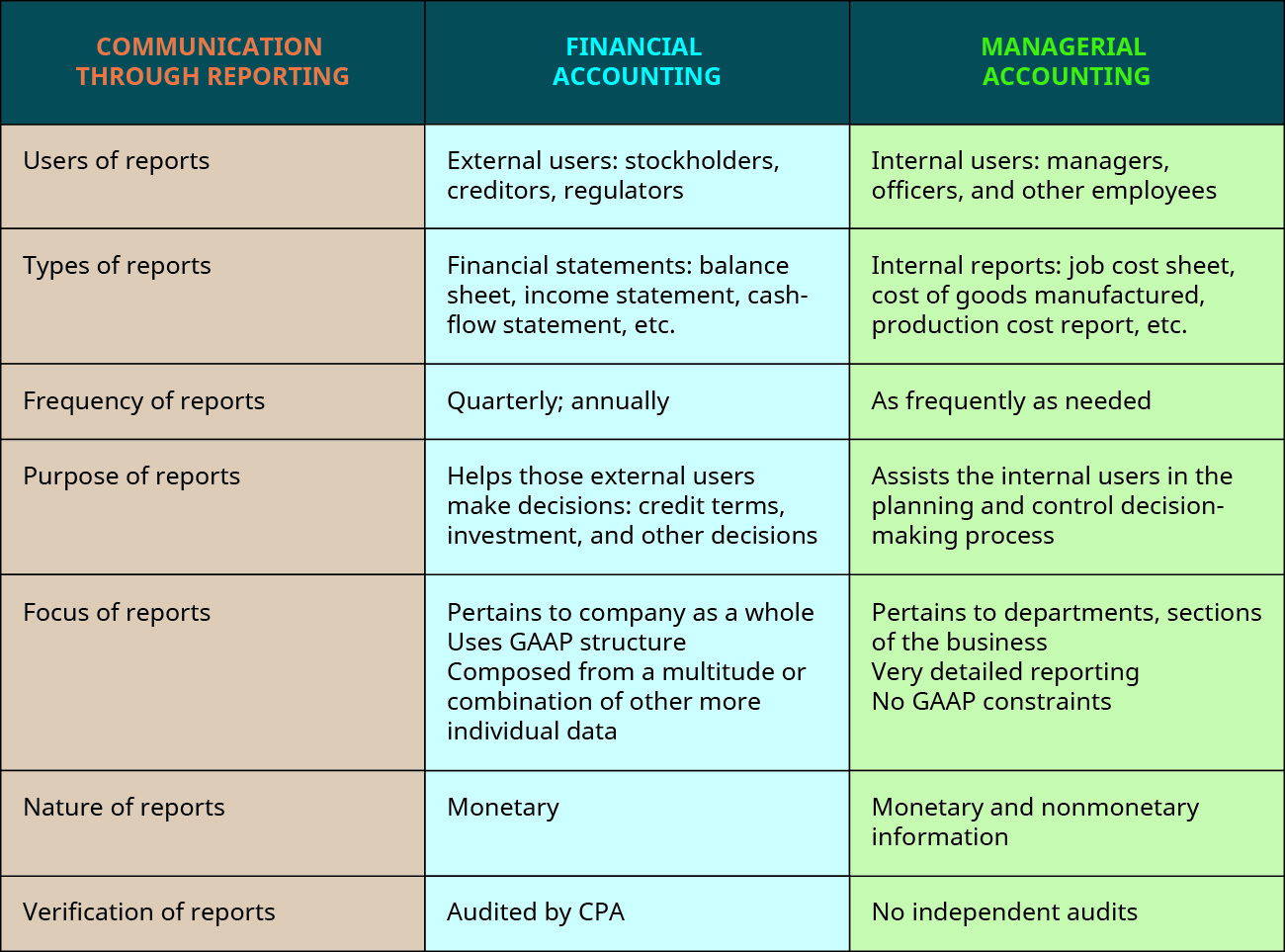

Managerial and financial accounting are used by every business, and there are important differences in their reporting functions. Those differences are detailed in Figure \(\PageIndex{2}\).

Users of Reports

The information generated from the reports of financial accountants tends to be used primarily by external users, including the creditors, tax authorities and regulators, investors, customers, competitors, and others outside the company, who rely on the financial statements and annual reports to access information about a company in order to make more informed decisions. Since these external people do not have access to the documents and records used to produce the financial statements, they depend on Generally Applied Accounting Principles (GAAP). These outside users also depend greatly on the preparation of audits that are done by public accounting firms, under the guidelines and standards of either the American Institute of Certified Public Accountants (AICPA), the US Securities and Exchange Commission (SEC), or the Public Company Accounting Oversight Board (PCAOB).

Managerial accounting information is gathered and reported for a more specific purpose for internal users, those inside the company or organization who are responsible for managing the company’s business interests and executing decisions. These internal users may include management at all levels in all departments, owners, and other employees. For example, in the budget development process, a company such as Tesla may want to project the costs of producing a new line of automobiles. The managerial accountants could create a budget to estimate the costs, such as parts and labor, and after the manufacturing process has begun, they can measure the actual costs, thus determining if they are over or under their budgeted amounts. Although outside parties might be interested in this information, companies like Tesla, Microsoft, and Boeing spend significant amounts of time and money to keep their proprietary information secret. Therefore, these internal budget reports are only available to the appropriate users. While you can find a cost of goods sold schedule in the financial statements of publicly traded companies, it is difficult for outside parties to break it down in order to identify the individual costs of products and services.

Investopedia is considered to be the largest Internet financial education resource in the world. There are many short, helpful videos that explain various concepts of managerial accounting. Watch this video explaining managerial accounting and how useful it can be to many different types of managers to learn more.

Types of Reports

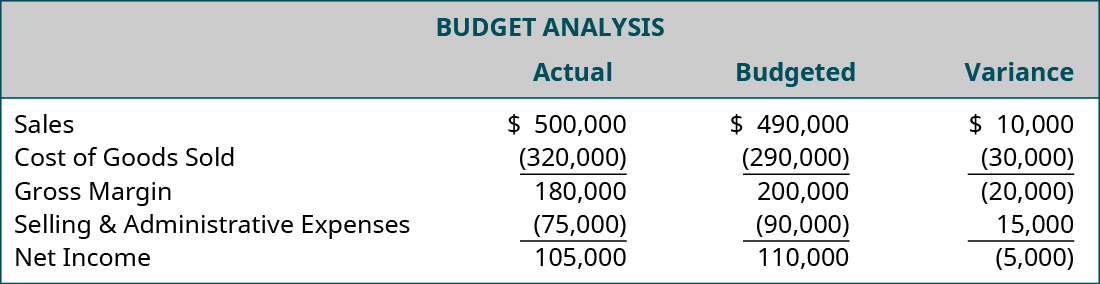

Financial accounting information is communicated through reporting, such as the financial statements. The financial statements typically include a balance sheet, income statement, cash flow statement, retained earnings statement, and footnotes. Managerial accounting information is communicated through reporting as well. However, the reports are more detailed and more specific and can be customized. One example of a managerial accounting report is a budget analysis (variance report) as shown in Figure \(\PageIndex{3}\). Other reports can include cost of goods manufactured, job order cost sheets, and production reports. Since managerial accounting is not governed by GAAP or other constraints, it is important for the creator of the reports to disclose all assumptions used to make the report. Since the reports are used internally, and not typically released to the general public, the presentation of any assumptions does not have to follow any industry-wide guidelines. Each organization is free to structure its reports in the format that organizes its information in the best way for it.

This type of analysis helps management to evaluate how effective they were at carrying out the plans and meeting the goals of the corporation. You will see many examples of reports and analyses that can be used as tools to help management make decisions.

You are working as the accountant in the special projects and budgets area of Sturm, Ruger & Company, a law firm that currently specializes in bankruptcy law. In order to serve their customers better and more efficiently, the company is trying to decide whether or not to expand its services and offer credit counseling, credit monitoring, credit rebuilding, and identity protection services. The president comes to you and asks for some sales and revenue projections. He would like the projections in three days’ time so that he can present the results to the board at the annual meeting.

You work tirelessly for two straight days compiling projections of sales and revenues to prepare the reports. The report is provided to the president just before the board is to arrive.

When you return to your office, you start clearing away some of the materials that you used in your report, and you discover an error that makes all of your projections significantly overstated. You ask the president’s administrative assistant if the president has presented the report to the board, and you find that he had mentioned it but not given the full report as of yet.

What would you do?

- What are the ethical concerns in this matter?

- What would be the results of telling the president of your error?

- What would be the results of not telling the president of your error?

Frequency of Reports

The financial statements are typically generated quarterly and annually, although some entities also require monthly statements. Much work is involved in creating the financial statements, and any adjustments to accounts must be made before the statements can be produced. A physical count inventory must be done to adjust the inventory and cost of goods sold accounts, depreciation must be calculated and entered, all prepaid asset accounts must be reviewed for adjustments, and so forth. The annual reports are not finalized for several weeks after the year-end, because they are based on historical data; for a company that is traded on one of the major or regional stock exchanges, it must have an audit of the financial statements conducted by an independent certified public accountant. This audit cannot be completed until after the end of the company’s fiscal year, because the auditors need access to all of the information for the company for that year. For companies that are privately held, an audit is not normally required. However, potential lenders might require an independent audit.

Conversely, managers can quickly attain managerial accounting information. No external, independent auditors are needed, and it is not necessary to wait until the year-end. Projections and estimates are adequate. Managers should understand that in order to obtain information quickly, they must accept less precision in the reporting. While there are several reports that are created on a regular basis (e.g., budgets and variance reports), many management reports are produced on an as-needed basis.

Purpose of Reports

The general purpose of financial statement reporting is to provide information about the results of operations, financial position, and cash flows of an organization. This data is useful to a wide range of users in order to make economic decisions. The purpose of the reporting done by management accountants is more specific to internal users. Management accountants make available the information that could assist companies in increasing their performance and profitability. Unlike financial reports, management reporting centers on components of the business. By dividing the business into smaller sections, a company is able to get into the details and analyze the smallest segments of the business.

An understanding of managerial accounting will assist anyone in the business world in determining and understanding product costs, analyzing break-even points, and budgeting for expenses and future growth (which will be covered in other parts of this course). As a manager, chief executive officer, or owner, you need to have information available at hand to answer these types of questions:

- Are my profits higher this quarter over last quarter?

- Do I have enough cash flow to pay my employees?

- Are my jobs priced correctly?

- Are my products priced correctly in order for me to make the profit I need to make?

- Who are my most productive and least productive employees?

In the world of business, information is power; stated simply, the more you know, typically, the better your decisions can be. Managerial accounting delivers data-driven feedback for these decisions that can assist in improving decision-making over the long term. Business managers can leverage this powerful tool in order to make their businesses more successful, because management accounting adds value to common business decision-making. All of this readily available information can lead to great improvements for any business.

Focus of Reports

Because financial accounting typically focuses on the company as a whole, external users of this information choose to invest or loan money to the entire company, not to a department or division within the company. Therefore, the global focus of financial accounting is understandable.

However, the focus of management accounting is typically different. Managerial reporting is more focused on divisions, departments, or any component of a business, down to individuals. The mid-level and lower-level managers are typically responsible for smaller subsets within the company.

Managers need accounting reports that deal specifically with their division and their specific activities. For instance, production managers are responsible for their specific area and the results within their division. Accordingly, these production managers need information about results achieved in their division, as well as individual results of departments within the division. The company can be broken into segments based on what managers need—for example, geographic location, product line, customer demographics (e.g., gender, age, race), or any of a variety of other divisions.

Nature of Reports

Both financial reports and managerial reports use monetary accounting information, or information relating to money or currency. Financial reports use data from the accounting system that is gathered from the reporting of transactions in the form of journal entries and then aggregated into financial statements. This information is monetary in nature. Managerial accounting uses some of the same financial information as financial accounting, but much of that information will be broken down to a more detailed level. For example, in financial reporting, net sales are needed for the income statement. In managerial accounting, the quantity and dollar value of the sales of each product are likely more useful. In addition, managerial accounting uses a significant amount of nonmonetary accounting information, such as quantity of material, number of employees, number of hours worked, and so forth, which does not relate to money or currency.

Verification of Reports

Financial reports rely on structure. They are generated using accepted principles that are enforced through a vast set of rules and guidelines, also known as GAAP. As mentioned previously, companies that are publicly traded are required to have their financial statements audited on an annual basis, and companies that are not publicly traded also may be required to have their financial statements audited by their creditors. The information generated by the management accountants is intended for internal use by the company’s divisions, departments, or both. There are no rules, guidelines, or principles to follow. Managerial accounting is much more flexible, so the design of the managerial accounting system is difficult to standardize, and standardization is unnecessary. It depends on the nature of the industry. Different companies (even different managers within the same company) require different information. The most important issue is whether the reporting is useful for the planning, controlling, and evaluation purposes.

Suppose you have been hired by Daryn’s Dairy as a market analyst. Your first assignment is to evaluate the sales of various standard and specialty ice creams within the Midwest region where Daryn’s Dairy operates. You also need to determine the best-selling flavors of ice cream in other regions of the United States as well as the selling patterns of the flavors. For example, do some flavors sell better than others at different times of the year, or are some top sellers sold as limited-edition flavors? Remember that one of the strategic goals of the company is to increase market share, and the first step in meeting this goal is to sell their product in 10 percent more stores within their current market, so your research will help upper-level management carry out the company’s goals. Where would you gather the information? What type of information would you need? Where would you find this information? How would the company determine the impact of this type of change on the business? If implemented, what information would you need to assess the success of the plan?

Solution

Answers will vary. Sample answer:

Where would you gather the information? Where would you find this information?

- Current company sales information would be obtained from internal company reports and records that detail the sale of each type of ice cream including volume, cost, price, and profit per flavor.

- Sales of ice cream from other companies may be more difficult to obtain, but the footnotes and supplemental information to the annual reports of those companies being analyzed, as well as industry trade journals, would likely be good sources of information.

What types of information would you need?

- Some of the types of information that would be needed would be the volume of sales of each flavor (number of gallons), how long each flavor has been sold, whether seasonal or limited-edition flavors are produced and sold only once or are on a rotating basis, the size of the market being examined (number of households), whether the other companies sell similar products (organic, all natural, etc.), the median income of consumers or other information to assess the consumers’ willingness to pay for organic products, and so forth.

How would Daryn’s Dairy determine the impact of this type of change on the business?

- Management would evaluate the cost to expand into new stores in their current market compared to the potential revenues from selling their products in those stores in order to assess the ability of the potential expansion to generate a profit for the company.

If implemented, what information would Daryn’s Dairy need to assess the success of the plan?

- Management would measure the profitability of selling any new products, expanding into new stores in their current market, or both to determine if the implementation of the plan was a success. If the plan is a success and the company is generating profits, the company will continue to figure out ways to improve efficiency and profitability. If the plan is not a success, the company will determine the reasons (cost to produce too high, sales price too high, volume too low, etc.) and make a new plan.