2.4: Job Costing Process with Journal Entries

- Page ID

- 26036

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\( \newcommand{\dsum}{\displaystyle\sum\limits} \)

\( \newcommand{\dint}{\displaystyle\int\limits} \)

\( \newcommand{\dlim}{\displaystyle\lim\limits} \)

\( \newcommand{\id}{\mathrm{id}}\) \( \newcommand{\Span}{\mathrm{span}}\)

( \newcommand{\kernel}{\mathrm{null}\,}\) \( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\) \( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\) \( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\id}{\mathrm{id}}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\kernel}{\mathrm{null}\,}\)

\( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\)

\( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\)

\( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\) \( \newcommand{\AA}{\unicode[.8,0]{x212B}}\)

\( \newcommand{\vectorA}[1]{\vec{#1}} % arrow\)

\( \newcommand{\vectorAt}[1]{\vec{\text{#1}}} % arrow\)

\( \newcommand{\vectorB}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vectorC}[1]{\textbf{#1}} \)

\( \newcommand{\vectorD}[1]{\overrightarrow{#1}} \)

\( \newcommand{\vectorDt}[1]{\overrightarrow{\text{#1}}} \)

\( \newcommand{\vectE}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash{\mathbf {#1}}}} \)

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\(\newcommand{\longvect}{\overrightarrow}\)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\(\newcommand{\avec}{\mathbf a}\) \(\newcommand{\bvec}{\mathbf b}\) \(\newcommand{\cvec}{\mathbf c}\) \(\newcommand{\dvec}{\mathbf d}\) \(\newcommand{\dtil}{\widetilde{\mathbf d}}\) \(\newcommand{\evec}{\mathbf e}\) \(\newcommand{\fvec}{\mathbf f}\) \(\newcommand{\nvec}{\mathbf n}\) \(\newcommand{\pvec}{\mathbf p}\) \(\newcommand{\qvec}{\mathbf q}\) \(\newcommand{\svec}{\mathbf s}\) \(\newcommand{\tvec}{\mathbf t}\) \(\newcommand{\uvec}{\mathbf u}\) \(\newcommand{\vvec}{\mathbf v}\) \(\newcommand{\wvec}{\mathbf w}\) \(\newcommand{\xvec}{\mathbf x}\) \(\newcommand{\yvec}{\mathbf y}\) \(\newcommand{\zvec}{\mathbf z}\) \(\newcommand{\rvec}{\mathbf r}\) \(\newcommand{\mvec}{\mathbf m}\) \(\newcommand{\zerovec}{\mathbf 0}\) \(\newcommand{\onevec}{\mathbf 1}\) \(\newcommand{\real}{\mathbb R}\) \(\newcommand{\twovec}[2]{\left[\begin{array}{r}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\ctwovec}[2]{\left[\begin{array}{c}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\threevec}[3]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\cthreevec}[3]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\fourvec}[4]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\cfourvec}[4]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\fivevec}[5]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\cfivevec}[5]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\mattwo}[4]{\left[\begin{array}{rr}#1 \amp #2 \\ #3 \amp #4 \\ \end{array}\right]}\) \(\newcommand{\laspan}[1]{\text{Span}\{#1\}}\) \(\newcommand{\bcal}{\cal B}\) \(\newcommand{\ccal}{\cal C}\) \(\newcommand{\scal}{\cal S}\) \(\newcommand{\wcal}{\cal W}\) \(\newcommand{\ecal}{\cal E}\) \(\newcommand{\coords}[2]{\left\{#1\right\}_{#2}}\) \(\newcommand{\gray}[1]{\color{gray}{#1}}\) \(\newcommand{\lgray}[1]{\color{lightgray}{#1}}\) \(\newcommand{\rank}{\operatorname{rank}}\) \(\newcommand{\row}{\text{Row}}\) \(\newcommand{\col}{\text{Col}}\) \(\renewcommand{\row}{\text{Row}}\) \(\newcommand{\nul}{\text{Nul}}\) \(\newcommand{\var}{\text{Var}}\) \(\newcommand{\corr}{\text{corr}}\) \(\newcommand{\len}[1]{\left|#1\right|}\) \(\newcommand{\bbar}{\overline{\bvec}}\) \(\newcommand{\bhat}{\widehat{\bvec}}\) \(\newcommand{\bperp}{\bvec^\perp}\) \(\newcommand{\xhat}{\widehat{\xvec}}\) \(\newcommand{\vhat}{\widehat{\vvec}}\) \(\newcommand{\uhat}{\widehat{\uvec}}\) \(\newcommand{\what}{\widehat{\wvec}}\) \(\newcommand{\Sighat}{\widehat{\Sigma}}\) \(\newcommand{\lt}{<}\) \(\newcommand{\gt}{>}\) \(\newcommand{\amp}{&}\) \(\definecolor{fillinmathshade}{gray}{0.9}\)Job costing

A job cost system (job costing) accumulates costs incurred according to the individual jobs. Companies generally use job cost systems when they can identify separate products or when they produce goods to meet a customer’s particular needs.

Who uses job costing? Examples include home builders who design specific houses for each customer and accumulate the costs separately for each job, and caterers who accumulate the costs of each banquet separately. Consulting, law, and public accounting firms use job costing to measure the costs of serving each client. Motion pictures, printing, and other industries where unique jobs are produced use job costing. Hospitals also use job costing to determine the cost of each patient’s care.

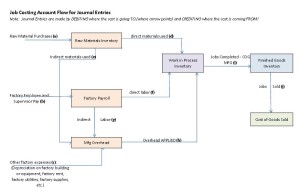

We will use the following flow chart to help us record the transactions in job costing (click job cost flow for a printable version complete with journal entry examples):

In a journal entry, we will do entries for each letter labeled in the chart — where the arrow is pointing TO is our debit and where the arrow is coming FROM is our credit. Here is a video discussion of job cost journal entries and then we will do an example.

A YouTube element has been excluded from this version of the text. You can view it online here: pb.libretexts.org/llmanagerialaccounting/?p=52

Example

Assume Creative Printers is a company run by a group of students who use desktop publishing to produce specialty books and instruction manuals. Creative Printers uses job costing. Creative Printers keeps track of the time and materials (mostly paper) used on each job.

The company compares the cost of each job with the revenue received to be sure the jobs are profitable. Sometimes the company learns that certain jobs are too costly considering the prices they can charge. For example, Creative Printers recently learned that cookbooks were not profitable. On the other hand, printing instruction manuals was quite profitable, so the company has focused more on the instruction manual market. To illustrate a job costing system, this section describes the transactions for the month of July for Creative Printers.

On July 1, Creative Printers had these beginning inventories:

| Materials inventory (or Raw Materials Inventory) | $20,000 |

|

Work in process inventory (Job No. 106: direct materials, $4,200;direct labor, $5,000; and overhead, $4,000) |

13,200 |

| Finished goods inventory (Job No. 105) | 5,500 |

Creative Printing had completed Job No. 105, a set of gardening books, but had not shipped them to the customer as of June 30. Additional information regarding July transactions follows:

a. During July, Creative Printers purchased $ 25,000 of materials on account. This purchase included both direct materials, such as paper, and indirect materials, such as printing supplies and computer supplies. The journal entry required would be:

| Debit | Credit | ||

| a. | Raw Materials Inventory | $ 25,000 | |

| Accounts Payable | 25,000 | ||

| Purchased materials on account | |||

b. During July, Creative Printers sent direct materials from the materials storeroom to jobs as follows: $ 9,000 to Job No. 106, and $ 14,000 to Job No. 107. The company also sent indirect materials of $ 1,000 to jobs. We want to move the cost of the direct materials FROM raw materials inventory TO work in process inventory. It charged indirect materials to overhead, not to each job, because the company does not keep track of how much indirect materials it uses on each job. (Manufacturing companies often use Manufacturing (or Factory) Overhead for the Overhead account. We generally use the Overhead account for both manufacturing and non-manufacturing companies in this chapter.) The entries would be:

| Debit | Credit | ||

| b. | Work In Process Inventory | 23,000 | |

| Raw Materials Inventory | 23,000 | ||

| Record direct materials used ($9,000+ 14,000) | |||

| Overhead | 1,000 | ||

| Raw Materials Inventory | 1,000 | ||

| Record indirect materials used | |||

c. Production workers keep track of the time spent on each job at Creative Printers. Based on that information, the company assigned production-related labor costs to jobs (direct labor) and to Overhead as follows: $4,000 to Job No. 106, $ 16,000 to Job No. 107, and indirect labor of $ 2,000 to Overhead. The entry to record payroll incurred during the accounting period (not shown) includes a debit to Payroll Summary (or Factory Payroll) and a credit to cash or a liability accounts depending if it has been paid. In these entries, we will distribute the payroll summary (Factory Payroll) to the jobs and overhead. For direct labor, we want to take the cost of labor FROM the payroll summary account TO work in process inventory. For indirect labor, we will charge this to overhead instead of to a specific job in work in process inventory.

| Debit | Credit | ||

| c. | Work In Process Inventory | 20,000 | |

| Factory Payroll | 20,000 | ||

| Record direct labor used ($4,000+ 16,000) | |||

| Overhead | 2,000 | ||

| Factory Payroll | 2,000 | ||

| Record indirect labor used | |||

d. The company assigns overhead to each job on the basis of the machine-hours each job uses. Overhead is assigned to a job at the rate of $ 2 per machine-hour used on the job. Job 16 had 875 machine-hours so we would charge overhead of $1,750 (850 machine-hours x $2 per machine-hour). Job 17 had 4,050 machine-hours so overhead would be $8,100 (4,050 machine-hours x $2). The journal entry to apply or assign overhead to the jobs would be to move the cost FROM overhead TO work in process inventory.

| Debit | Credit | ||

| d. | Work In Process Inventory | 9,850 | |

| Overhead | 9,850 | ||

| Record overhead applied ($1,750+ 8,100) | |||

The complete job cost sheets for Jobs 106 and 107 would appear as below:

| Job: | 106 | 107 |

| Beginning Work in Process | $13,200 | 0 |

| Added this period: | ||

| Direct Materials | 9,000 | 14,000 |

| Direct Labor | 4,000 | 16,000 |

| Overhead applied | 1,750 | 8,100 |

| Total Job Costs | $ 27,950 | $ 38,100 |

e. Job No. 106 was completed. The total job cost of Job 106 is $27,950 for the total work done on the job, including costs in beginning Work in Process Inventory on July 1 and costs added during July. This entry records the completion of Job 106 by moving the total cost FROM work in process inventory TO finished goods inventory.

| Debit | Credit | ||

| e. | Finished Goods Inventory | 27,950 | |

| Work In Process Inventory | 27,950 | ||

| Record completion of Job 16 | |||

| (Beg. WIP $13,200 + DM 9,000 + DL 4,000 + OH 1,750) | |||

f. Job No. 105 was sold on account in July for $ 9,000. This transaction would require 2 entries: one for the sales and customer side and one for the company’s actual cost (remember, you do not want these to be the same amount. You want to charge customers MORE than it cost you to make a profit). Since this was sold on account, we know that means accounts receivable. The cost of Job 105 can be found in the beginning inventory for finished goods inventory.

| Debit | Credit | ||

| f. | Accounts Receivable | 9,000 | |

| Sales | 9,000 | ||

| Record sale of Job 105 for $9,000 on account | |||

| Cost of goods sold | 5,500 | ||

| Finished Goods Inventory | 5,500 | ||

| Record total cost of Job 105 now sold | |||

g. The company applied overhead to the jobs in entry (d) based on a predetermined overhead rate. Many of the actual overhead costs are not known until the end of the month or later. For example, the company would not receive its utility bill for July until sometime in August. In addition to the indirect materials and indirect labor recorded in entries (b) and (c), Creative Printers incurred these other overhead costs for July:

| Machinery repairs and maintenance | $1,500 |

| Utilities, including energy costs to run machines | 1,000 |

| Depreciation of building and machines | 2,500 |

| Other overhead | 1,800 |

| Total overhead incurred in July, other than indirect materials and indirect labor | $6,800 |

To prepare the journal entry, we debit the Overhead account for the actual costs. Then we credit Accounts Payable for the machinery repairs and maintenance, utilities, and other overhead. (We assume an outside contractor does the maintenance and repairs.) The amount is $ 4,300 ($ 3,500 + $ 1,000 + $ 1,800). And, finally we credit Accumulated Depreciation for $ 2,500. Here is the journal entry to record the actual overhead:

| Debit | Credit |

||

| g. | Overhead | 6,800 | |

| Accounts Payable | 4,300 | ||

| Accum. Depreciation | 2,500 | ||

| Record actual overhead costs incurred | |||

If we posted each of these journal entries, you will find the ending balances of the inventory accounts to be:

| Raw Materials Inventory | $21,000 |

| (20,000 + 25,000 – 23,000 – 1,000) | |

| Work in Process Inventory | $38,100 |

| (Total costs of Job 17) | |

| Finished Goods Inventory | $27,950 |

| (Total cost of Job 16) |

Notice, Job 105 has been moved from Finished Goods Inventory since it was sold and is now reported as an expense called Cost of Goods Sold. Also, did you notice that actual overhead came to $9,800 ($1,000 indirect materials + $2,000 indirect labor + $6,800 other overhead from transaction g) but we applied $9,850 in overhead to the jobs in transaction d? Whenever we use an estimate instead of actual numbers, it should be expected that an adjustment is needed. We will discuss the difference between actual and applied overhead and how we handle the differences in the next sections.

Managers would use the preceding cost information for several purposes: First, they would compare the actual costs of the job with expected costs, both as the work is being done and after the job has been completed. Later chapters discuss the role of managerial accounting in performance evaluation.

Second, managers would assess the profitability of jobs. For example, Job 105 had revenue of USD 9,000 and costs of USD 5,500.Third, managers would compare actual overhead on the left side of the Overhead account, with the overhead applied to jobs on the right side. If the actual overhead exceeds the applied overhead, they may wish to learn why the actual overhead is so high. Also, they may ask the accountants to increase the overhead applied to jobs to give them a better idea of the cost of jobs. If the actual is less than the applied overhead, they may ask the accountants to reduce the overhead applied to jobs.

- Accounting Principles: A Business Perspective.. Authored by: James Don Edwards, University of Georgia & Roger H. Hermanson, Georgia State University.. Provided by: Endeavour International Corporation. Project: The Global Text Project.. License: CC BY: Attribution

- Management Accounting Job Order Journal Entries (Managerial Accounting Tutorial #25) . Authored by: Note Pirate. Located at: youtu.be/Ut_2r-hvfXA. License: All Rights Reserved. License Terms: Standard YouTube License