12.7: Appendix- Using the Direct Method to Prepare the Statement of Cash Flows

- Page ID

- 27360

- Prepare a statement of cash flows using the direct method.

Question: The same four steps apply to preparing a statement of cash flows using the direct method as with the indirect method. The only difference is how the operating activities section is presented in step 1; all other steps are the same as presented in the chapter. Although presentation of the operating activities section using the direct method differs from the indirect method, the end result is exactly the same. How does step 1 differ using the direct method?

- Answer

-

Rather than adjusting net income from an accrual basis to a cash basis using the indirect method, the direct method simply presents the income statement on a cash basis. The format of the operating activities section using the direct method is presented in Figure 12.10.

Figure 12.10. Operating Activities Format Using the Direct Method

The first item shown in Figure 12.10, cash receipts from customers, is revenue (or sales) on a cash basis. The second item, cash payments to suppliers, is cost of goods sold on a cash basis. The third item, cash payments for operating expenses (also called selling and administrative expenses), is operating expenses on a cash basis. The fourth item, cash payments for interest expense, is interest expense on a cash basis. And the fifth item, cash payments for income taxes, is income tax expense on a cash basis. Cash receipts minus cash payments results in cash provided by operating activities.

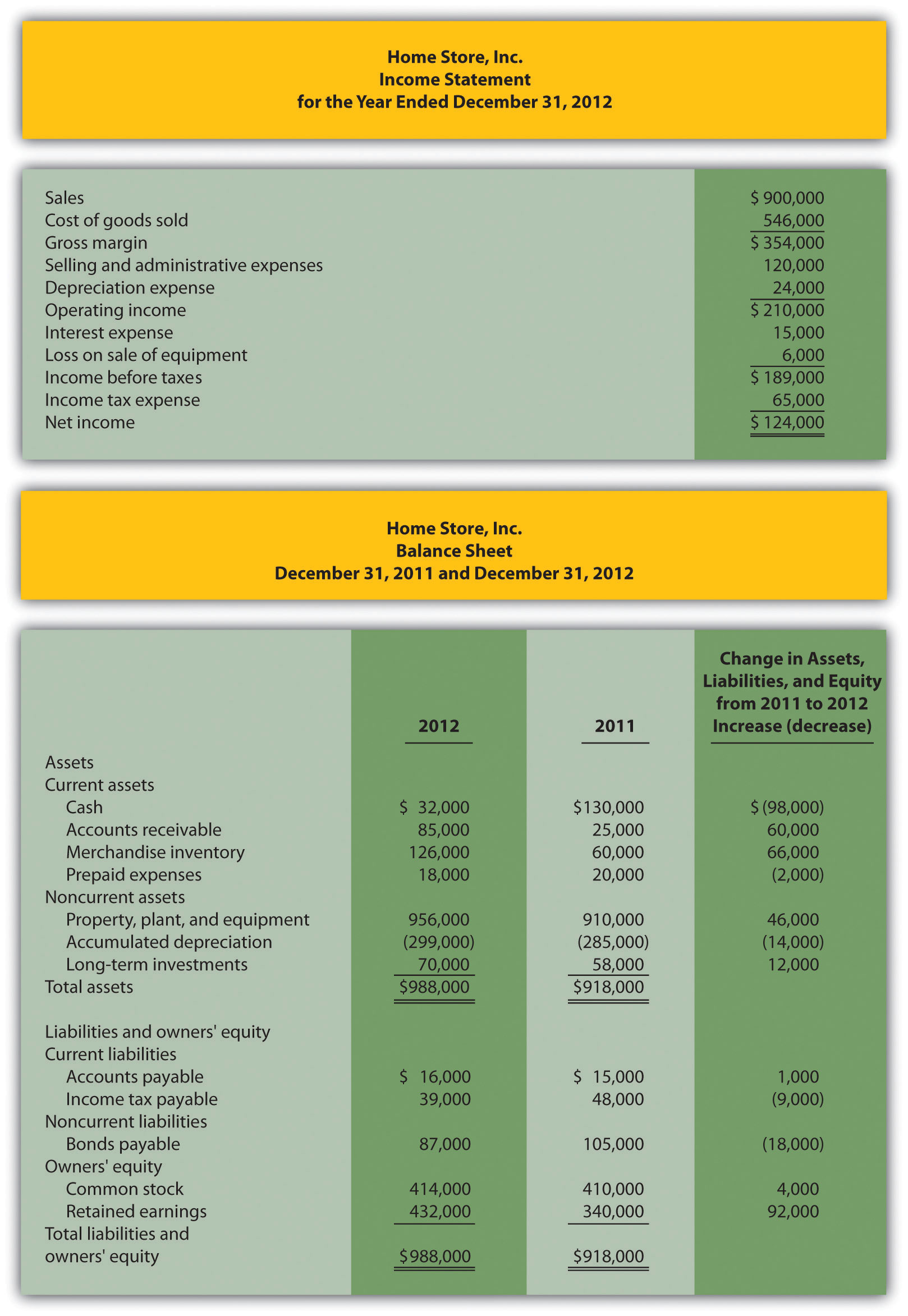

Adjustments must be made to each income statement item to convert income statement information from an accrual basis to a cash basis. These adjustments will be described next using the same information for Home Store, Inc., presented earlier in the chapter. The income statement and balance sheet for Home Store, Inc., are presented again in Figure 12.11. We will start at the top of the income statement with sales and work our way down item-by-item making adjustments to convert each item to a cash basis.

Figure 12.11. Income Statement and Balance Sheet (Home Store, Inc.)

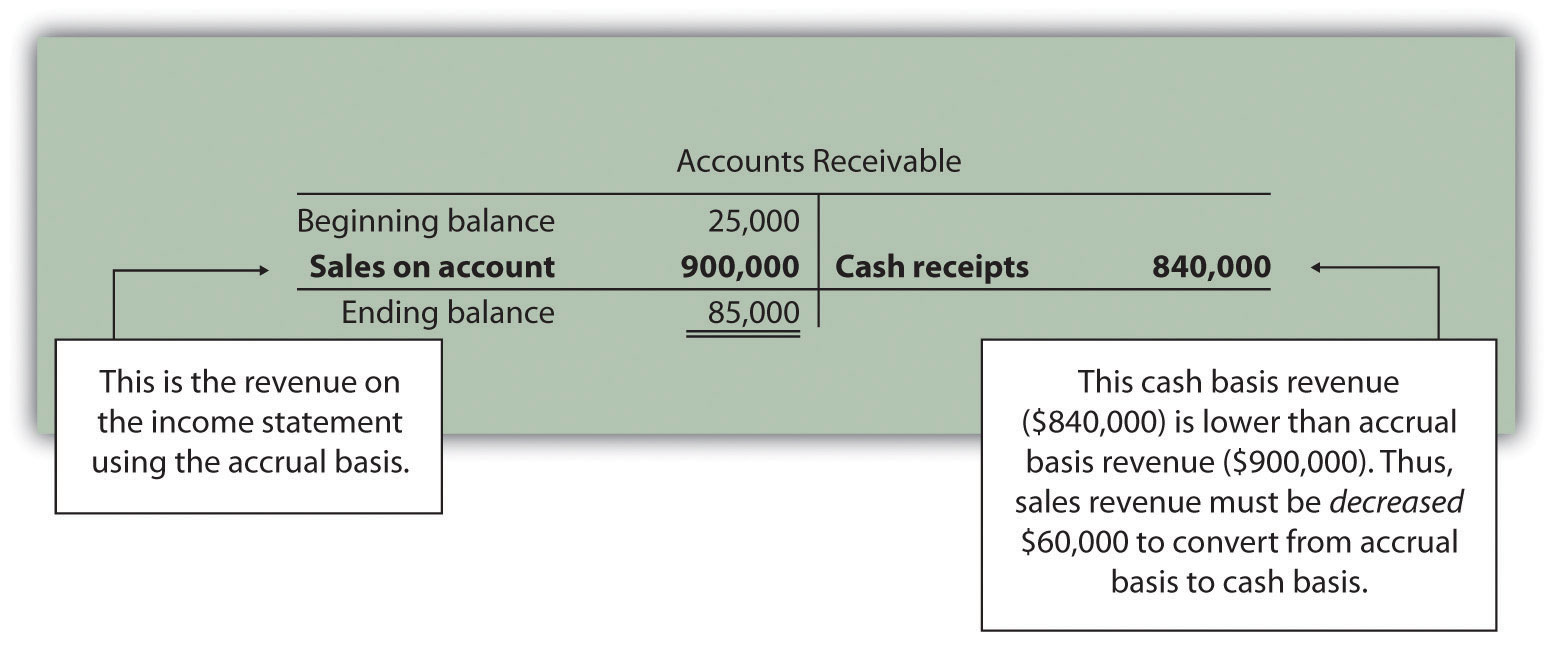

Converting Sales to Cash Receipts

Question: How are sales on an accrual basis converted to sales on a cash basis?

- Answer

Here’s how sales revenue on a cash basis appears in the operating activities section of the statement of cash flows for Home Store, Inc.:

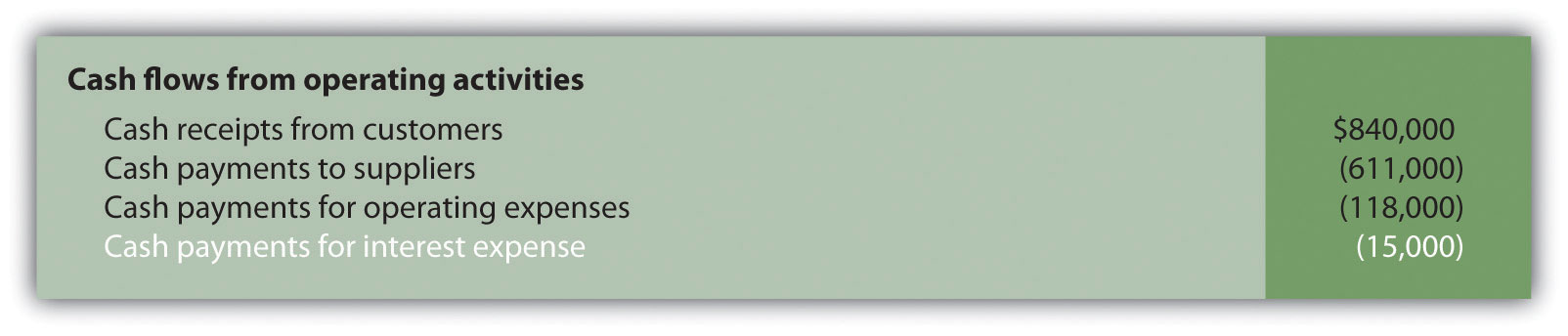

Converting Cost of Goods Sold to a Cash Basis

Question: How is cost of goods sold on an accrual basis converted to cost of goods sold on a cash basis?

- Answer

Here’s how cost of goods sold on a cash basis appears in the operating activities section of the statement of cash flows for Home Store, Inc.:

Converting Operating Expenses to a Cash Basis

Question: How are operating expenses on an accrual basis converted to operating expenses on a cash basis?

- Answer

Here’s how operating expenses on a cash basis appears in the operating activities section of the statement of cash flows for Home Store, Inc.:

Depreciation Expense

Question: How is depreciation expense handled when using the direct method?

- Answer

-

Since depreciation is a noncash expense, it is not included in the statement of cash flows using the direct method.

Converting Interest Expense to a Cash Basis

Question: How is interest expense on an accrual basis converted to interest expense on a cash basis?

- Answer

Here’s how interest expense on a cash basis appears in the operating activities section of the statement of cash flows for Home Store, Inc.:

Loss on Sale of Equipment

Question: How is the loss on sale of equipment handled when using the direct method?

- Answer

-

Because the loss on sale of equipment is included as part of the proceeds from the sale of equipment in the investing activities section, this item is not included in the operating activities section. This holds true for both the direct and indirect methods.

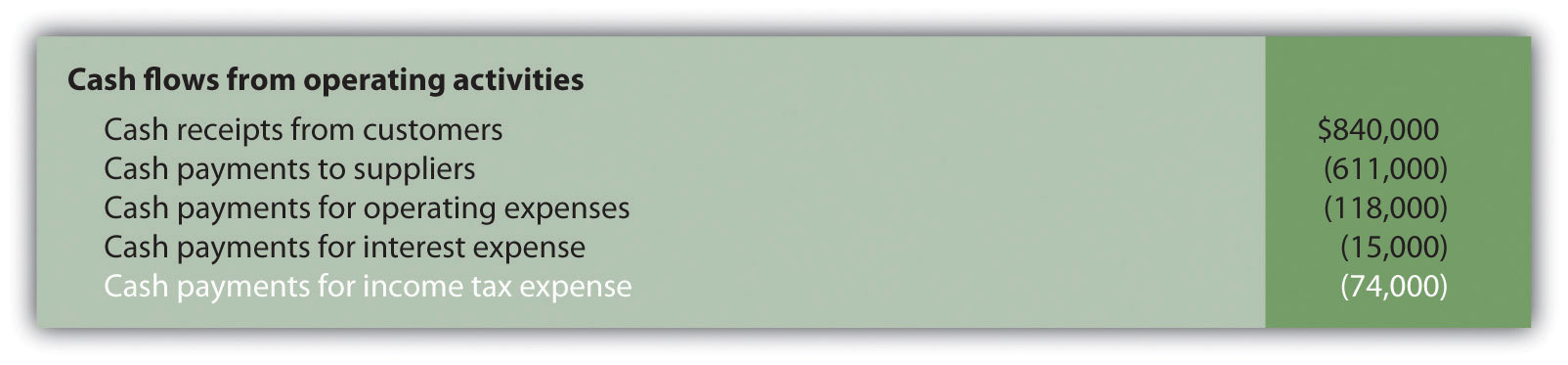

Converting Income Tax Expense to a Cash Basis

Question: How is income tax expense on an accrual basis converted to income tax expense on a cash basis?

- Answer

-

Income tax expense of $65,000 shown on the income statement does not represent cash paid for income taxes. The adjustment rule used to convert income tax expense to cash payments for income taxes is: Increases in income taxes payable are deducted from income tax expense, and conversely, decreases in income taxes payable are added to income tax expense. (The same rules apply to companies that have deferred income taxes.) Since income taxes payable decreased $9,000, income tax expense is increased $9,000. Thus cash payments for income taxes totaled $74,000 (= $65,000 income tax expense + $9,000 decrease in income taxes payable).

Here’s how income tax expense on a cash basis appears in the operating activities section of the statement of cash flows for Home Store, Inc.:

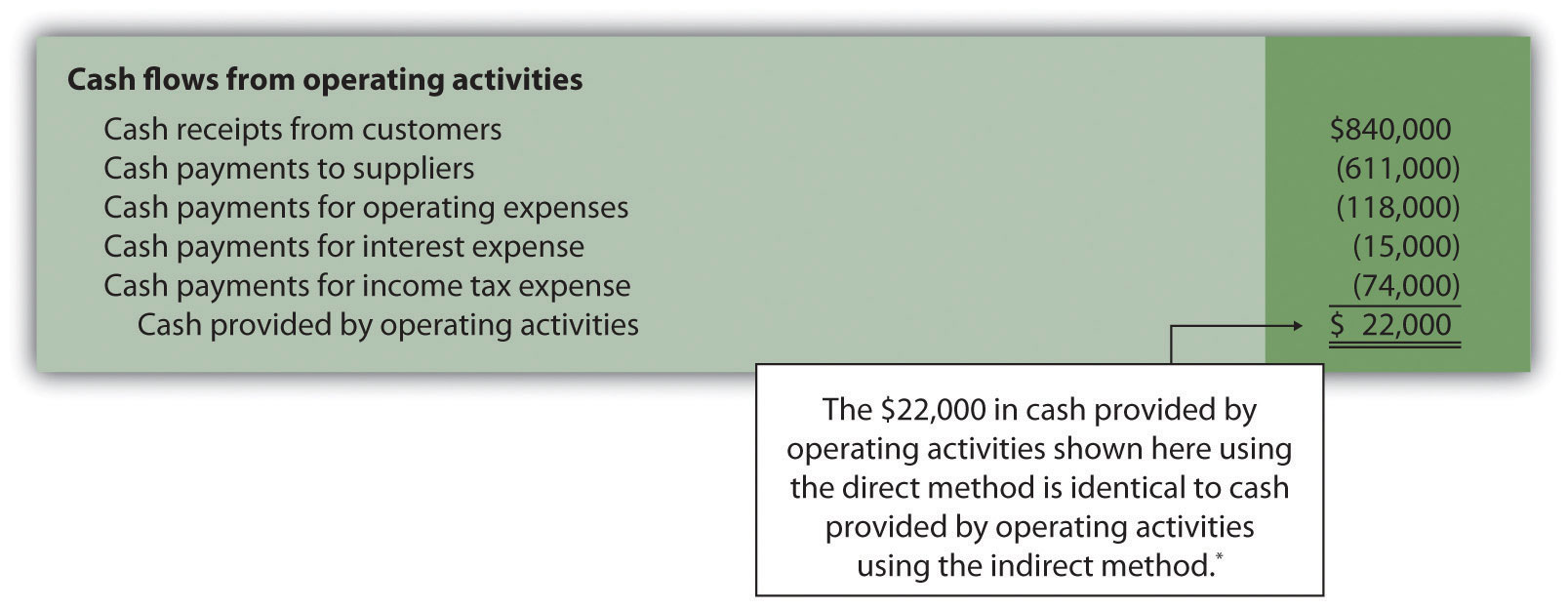

Question: What does the completed operating activities section for Home Store, Inc., look like using the direct method?

- Answer

-

The operating activities section for Home Store, Inc., is shown in Figure 12.12. Notice that cash provided by operating activities of $22,000 in Figure 12.12 (using the direct method) matches cash provided by operating activities in Figure 12.5 (using the indirect method). The direct and indirect methods of presenting the operating activities section of the statement of cash flows yield the exact same results. Also note that the investing and financing activities do not change using the direct method.

Figure 12.12. Operating Activities Section Using the Direct Method (Home Store, Inc.)

*As shown in Figure 12.5.

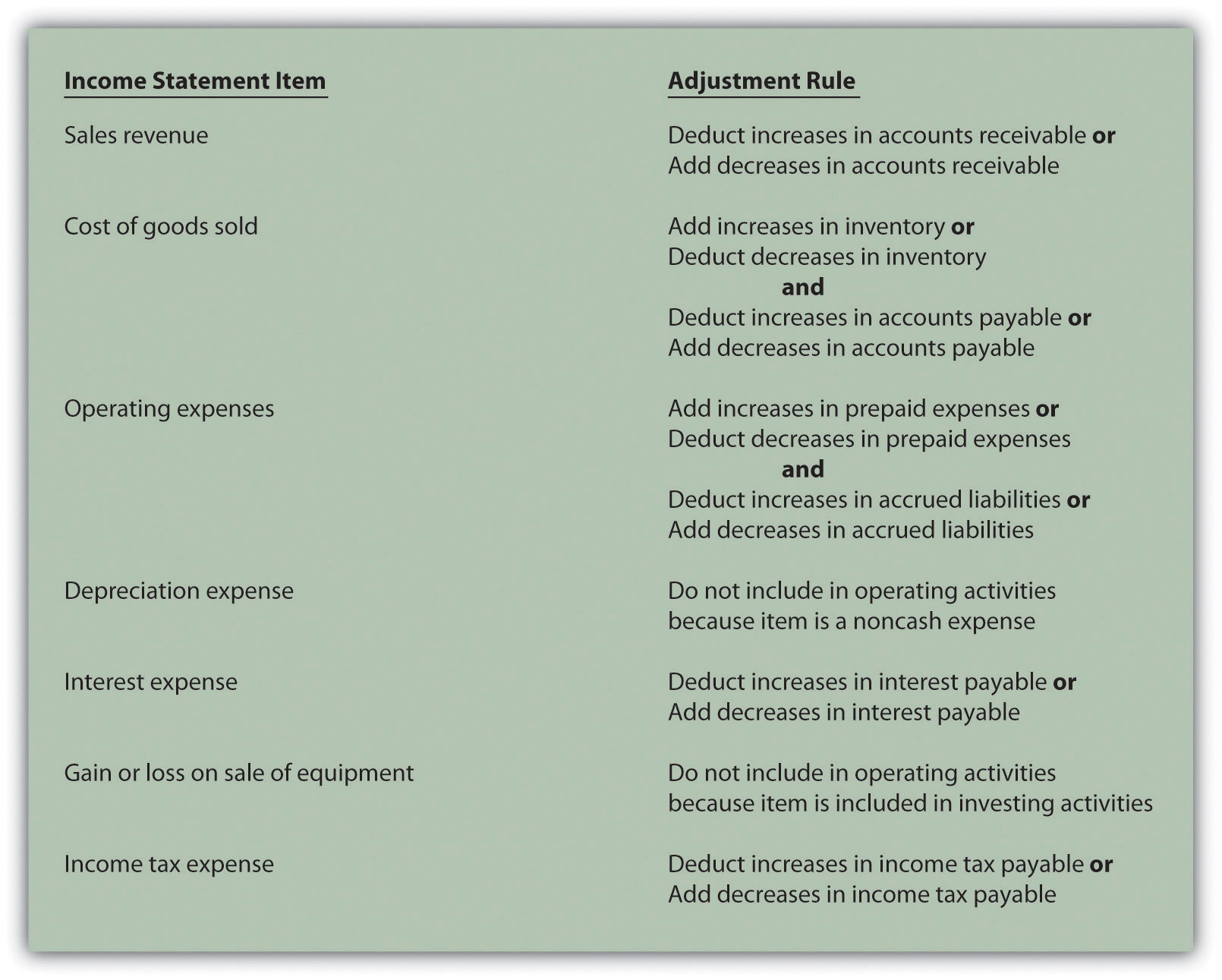

Figure 12.13 summarizes the rules used to convert income statement line items to a cash basis. Review these rules carefully before working Note 12.40 "Review Problem 12.9".

Figure 12.13. Adjustment Rules for the Direct Method

The same four steps apply to preparing the statement of cash flows using the direct method as with the indirect method. The difference is in the operating activities section of step 1. In step 1, the indirect method starts with net income and makes adjustments to convert net income to a cash basis. The direct method makes adjustments directly to each income statement revenue and expense line item, thereby converting each line item to a cash basis. The resulting cash provided by (used by) operating activities is identical in both approaches.

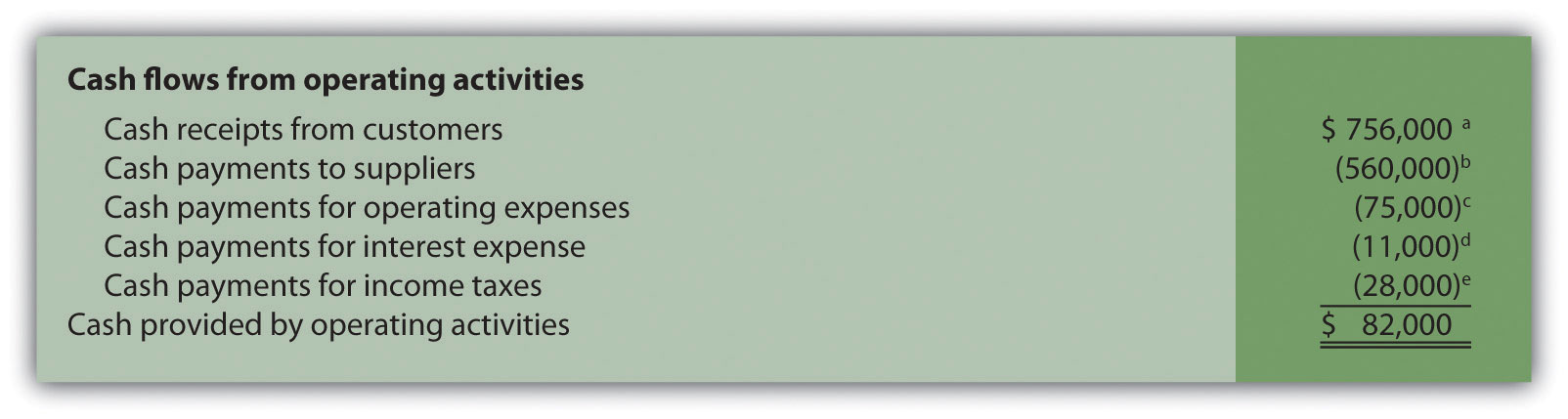

Using the information presented for Phantom Books in Note 12.21 "Review Problem 12.4", prepare the operating activities section of the statement of cash flows using the direct method. Follow the format presented in Figure 12.12, and refer to the adjustment rules in Figure 12.13.

- Answer

-

The operating activities section of the statement of cash flows for Phantom Books using the direct method is presented as follows. Notice that cash provided by operating activities of $82,000 shown here using the direct method is identical to cash provided by operating activities using the indirect method (shown in the solution to Note 12.21 "Review Problem 12.4").

a $756,000 = $750,000 sales revenue + $6,000 decrease in accounts receivable.

b $560,000 = $546,000 cost of goods sold + $13,000 increase in inventory + $1,000 decrease in accounts payable.

c $75,000 = $79,000 operating expenses − $4,000 decrease in prepaid expenses.

d Since no interest payable balances exist this year or last year, the interest expense of $11,000 is the same as cash payments for interest expense.

e $28,000 = $30,000 income tax expense − $2,000 increase in income tax payable.