15.1: Long-Term Financing

- Page ID

- 26273

In previous chapters, you learned that corporations obtain cash for recurring business operations from stock issuances, profitable operations, and short-term borrowing (current liabilities). However, when situations arise that require large amounts of cash, such as the purchase of a building, corporations also raise cash from long-term borrowing. One way to borrow this money is through getting a loan through the bank (like in the case of a mortgage) or the corporation could issue bonds. The issuing of bonds results in a Bonds Payable account.

youtu.be/WIeHWjxvU9M

Bonds payable

A bond is a long-term debt, or liability, owed by its issuer. Physical evidence of the debt lies in a negotiable bond certificate. In contrast to long-term notes, which usually mature in 10 years or less, bond maturities often run for 20 years or more.

Generally, a bond issue consists of a large number of $1,000 bonds rather than one large bond. For example, a company seeking to borrow $100,000 would issue one hundred $1,000 bonds rather than one $100,000 bond. This practice enables investors with less cash to invest to purchase some of the bonds.

Bonds derive their value primarily from two promises made by the borrower to the lender or bondholder. The borrower promises to pay (1) theface value or principal amount of the bond on a specific maturity date in the future and (2) periodic interest at a specified rate on face value at stated dates, usually semiannually, until the maturity date.

Large companies often have numerous long-term notes and bond issues outstanding at any one time. The various issues generally have different stated interest rates and mature at different points in the future. Companies present this information in the footnotes to their financial statements. Promissory notes, debenture bonds, and foreign bonds are shown with their amounts, maturity dates, and interest rates.

Comparison with stock

A bond differs from a share of stock in several ways:

•A bond is a debt or liability of the issuer, while a share of stock is a unit of ownership.

•A bond has a maturity date when it must be paid. A share of stock does not mature; stock remains outstanding indefinitely unless the company decides to retire it.

•Most bonds require stated periodic interest payments by the company. In contrast, dividends to stockholders are payable only when declared; even preferred dividends need not be paid in a particular period if the board of directors so decides.

•Bond interest is deductible by the issuer in computing both net income and taxable income, while dividends are not deductible in either computation.

Selling (issuing) bonds

A company seeking to borrow millions of dollars generally is not able to borrow from a single lender. By selling (issuing) bonds to the public, the company secures the necessary funds.

Usually companies sell their bond issues through an investment company or a banker called an underwriter. The underwriter performs many tasks for the bond issuer, such as advertising, selling, and delivering the bonds to the purchasers. Often the underwriter guarantees the issuer a fixed price for the bonds, expecting to earn a profit by selling the bonds for more than the fixed price.

When a company sells bonds to the public, many purchasers buy the bonds. Rather than deal with each purchaser individually, the issuing company appoints a trustee to represent the bondholders. The trustee usually is a bank or trust company. The main duty of the trustee is to see that the borrower fulfills the provisions of the bond indenture. A bond indenture is the contract or loan agreement under which the bonds are issued. The indenture deals with matters such as the interest rate, maturity date and maturity amount, possible restrictions on dividends, repayment plans, and other provisions relating to the debt. An issuing company that does not adhere to the bond indenture provisions is in default. Then, the trustee takes action to force the issuer to comply with the indenture.

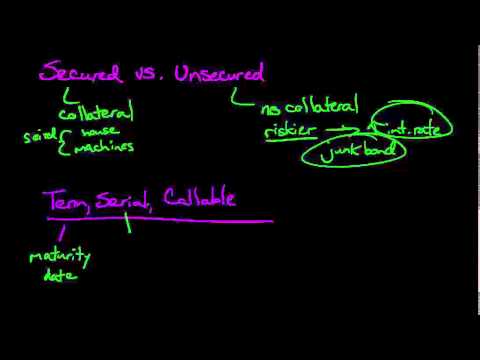

Bonds may differ in some respects; they may be secured or unsecured bonds, registered or unregistered (bearer) bonds, and term or serial bonds. We discuss these differences next but first watch this video about the different bond types.

A YouTube element has been excluded from this version of the text. You can view it online here: pb.libretexts.org/llfinancialaccounting/?p=268

Certain bond features are matters of legal necessity, such as how a company pays interest and transfers ownership. Such features usually do not affect the issue price of the bonds. Other features, such as convertibility into common stock, are sweeteners designed to make the bonds more attractive to potential purchasers. These sweeteners may increase the issue price of a bond.

- Secured bonds: A secured bond is a bond for which a company has pledged specific property to ensure its payment. Mortgage bonds are the most common secured bonds. A mortgage is a legal claim (lien) on specific property that gives the bondholder the right to possess the pledged property if the company fails to make required payments.

- Unsecured bonds: An unsecured bond is a debenture bond, or simply a debenture. A debenture is an unsecured bond backed only by the general creditworthiness of the issuer, not by a lien on any specific property. A financially sound company can issue debentures more easily than a company experiencing financial difficulty.

- Registered bonds: A registered bond is a bond with the owner’s name on the bond certificate and in the register of bond owners kept by the bond issuer or its agent, the registrar. Bonds may be registered as to principal (or face value of the bond) or as to both principal and interest. Most bonds in our economy are registered as to principal only. For a bond registered as to both principal and interest, the issuer pays the bond interest by check. To transfer ownership of registered bonds, the owner endorses the bond and registers it in the new owner’s name. Therefore, owners can easily replace lost or stolen registered bonds.

- Unregistered (bearer) bonds: An unregistered (bearer) bond is the property of its holder or bearer because the owner’s name does not appear on the bond certificate or in a separate record. Physical delivery of the bond transfers ownership.

- Coupon bonds: A coupon bond is a bond not registered as to interest. Coupon bonds carry detachable coupons for the interest they pay. At the end of each interest period, the owner clips the coupon for the period and presents it to a stated party, usually a bank, for collection.

- Term bonds and serial bonds: A term bond matures on the same date as all other bonds in a given bond issue. Serial bonds in a given bond issue have maturities spread over several dates. For instance, one-fourth of the bonds may mature on 2011 December 31, another one-fourth on 2012 December 31, and so on.

- Callable bonds: A callable bond contains a provision that gives the issuer the right to call (buy back) the bond before its maturity date. The provision is similar to the call provision of some preferred stocks. A company is likely to exercise this call right when its outstanding bonds bear interest at a much higher rate than the company would have to pay if it issued new but similar bonds. The exercise of the call provision normally requires the company to pay the bondholder a call premium of about $30 to $70 per $1,000 bond. A call premium is the price paid in excess of face value that the issuer of bonds must pay to redeem (call) bonds before their maturity date.

- Convertible bonds: A convertible bond is a bond that may be exchanged for shares of stock of the issuing corporation at the bondholder’s option. A convertible bond has a stipulated conversion rate of some number of shares for each $1,000 bond. Although any type of bond may be convertible, issuers add this feature to make risky debenture bonds more attractive to investors.

- Bonds with stock warrants: A stock warrant allows the bondholder to purchase shares of common stock at a fixed price for a stated period. Warrants issued with long-term debt may be nondetachable or detachable. A bond with nondetachable warrants is virtually the same as a convertible bond; the holder must surrender the bond to acquire the common stock. Detachable warrants allow bondholders to keep their bonds and still purchase shares of stock through exercise of the warrants.

- Junk bondsJunk bonds are high-interest rate, high-risk bonds. Many junk bonds issued in the 1980s financed corporate restructurings. These restructurings took the form of management buyouts (called leveraged buyouts or LBOs), hostile takeovers of companies by outside parties, or friendly takeovers of companies by outside parties. In the early 1990s, junk bonds lost favor because many issuers defaulted on their interest payments. Some issuers declared bankruptcy or sought relief from the bondholders by negotiating new debt terms.

Several advantages come from raising cash by issuing bonds rather than stock. First, the current stockholders do not have to dilute or surrender their control of the company when funds are obtained by borrowing rather than issuing more shares of stock. Second, it may be less expensive to issue debt rather than additional stock because the interest payments made to bondholders are tax deductible while dividends are not. Finally, probably the most important reason to issue bonds is that the use of debt may increase the earnings of stockholders through favorable financial leverage.

A company has favorable financial leverage when it uses borrowed funds to increase earnings per share (EPS) of common stock. An increase in EPS usually results from earning a higher rate of return than the rate of interest paid for the borrowed money. For example, suppose a company borrowed money at 10 per cent and earned a 15 per cent rate of return. The 5 per cent difference increases earnings.

Several disadvantages accompany the use of debt financing. First, the borrower has a fixed interest payment that must be met each period to avoid default. Second, use of debt also reduces a company’s ability to withstand a major loss. A third disadvantage of debt financing is that it also causes a company to experience unfavorable financial leverage when income from operations falls below a certain level. Unfavorable financial leverage results when the cost of borrowed funds exceeds the revenue they generate; it is the reverse of favorable financial leverage. The fourth disadvantage of issuing debt is that loan agreements often require maintaining a certain amount of working capital (Current assets – Current liabilities) and place limitations on dividends and additional borrowings.

- Accounting Principles: A Business Perspective. Authored by: James Don Edwards, University of Georgia & Roger H. Hermanson, Georgia State University. Provided by: Endeavour International Corporation. Project: The Global Text Project. License: CC BY: Attribution

- Not Your Mama's Finance Lesson: What the Heck is a Bond?. Authored by: Nicole Lapin. Located at: youtu.be/WIeHWjxvU9M. License: All Rights Reserved. License Terms: Standard YouTube License

- Types of Bonds. Authored by: Education Unlocked. Located at: youtu.be/Jj0V01Arebk. License: All Rights Reserved. License Terms: Standard YouTube License