12.2: Entries Related to Notes Payable

- Page ID

- 26253

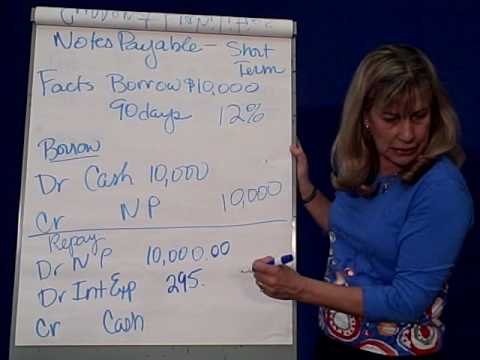

Here is a classic video on short term notes payable that will allow us to review some of the concepts we learned when discussing Notes Receivable.

A YouTube element has been excluded from this version of the text. You can view it online here: pb.libretexts.org/llfinancialaccounting/?p=222

Remember, with Notes Receivable we learned we need to know 3 things about a note:

- Principal (the amount of money we borrowed)

- Interest Rate (typically an annual interest rate)

- Maturity term (or frequency of the year — how many days or months for the note)

In Notes Receivable, we were the ones providing funds that we would receive at maturity. Now, we are going to borrow money that we must pay back later so we will have Notes Payable. Interest is still calculated as Principal x Interest x Frequency of the year (use 360 days as the base if note term is days or 12 months as the base if note term is in months).

Interest-bearing notes To receive short-term financing, a company may issue an interest-bearing note to a bank. An interest-bearing note specifies the interest rate charged on the principal borrowed. The company receives from the bank the principal borrowed; when the note matures, the company pays the bank the principal plus the interest.

Accounting for an interest-bearing note is simple. For example, assume the company’s accounting year ends on December 31. Needham Company issued a $10,000, 90-day, 9% note on December 1. The following entries would record the loan, the accrual of interest on December 31 and its payment on March 1 of the next year:

| Date | Account | Debit | Credit |

| Dec 1 | Cash | 10,000 | |

| Notes Payable | 10,000 | ||

| To record 90-day bank loan. | |||

| Dec 31 | Interest Expense | 75 | |

| Interest Payable | 75 | ||

| $10,000 x 9% x (30 days in Dec / 360 days in year) | |||

| To record accrued interest on note at year end | |||

| Mar 1 | Notes Payable (principal amount) | 10,000 | |

| Interest Payable (from Dec 31 entry) | 75 | ||

| Interest Expense | 150 | ||

| $10,000 x 9% x (60 days remaining in note / 360 days in year) | |||

| Cash (10,000 + 75 + 150) | 10,225 | ||

| To record principal and interest paid on bank loan. |

- Accounting Principles: A Business Perspective.. Authored by: James Don Edwards, University of Georgia & Roger H. Hermanson, Georgia State University. . Provided by: Endeavour International Corporation.. Project: The Global Text Project.t. License: CC BY: Attribution

- FA 8 2 Notes Payable. Authored by: Susan Crosson. Located at: youtu.be/hdyO5Csq1Hs. License: All Rights Reserved. License Terms: Standard YouTube License