6.1: Adjusting Entries for a Merchandising Company

- Page ID

- 26210

Remember this?

| Accounting Cycle | ||

| 1. Analyze Transactions | 5. Prepare Adjusting Journal Entries | 9. Prepare Closing Entries |

| 2. Prepare Journal Entries | 6. Post Adjusting Journal Entries | 10. Post Closing Entries |

| 3. Post journal Entries | 7. Prepare Adjusted Trial Balance | 11. Prepare Post-Closing Trial Balance |

| 4. Prepare Unadjusted Trial Balance | 8. Prepare Financial Statements | |

We learned how the accounting cycle applies to a service company but guess what? The same accounting cycle applies to any business. We spent the last section discussing the journal entries for sales and purchase transactions. Now we will look how the remaining steps are used in a merchandising company. Those wonderful adjusting entries we learned in previous sections still apply.

Adjusting entries reflect unrecorded economic activity that has taken place but has not yet been recorded because it is either more convenient to wait until the end of the period to record the activity, or because no source document concerning that activity has yet come to the accountant’s attention. Additionally, periodic reporting and the matching principle necessitate the preparation of adjusting entries. Remember, the matching principle indicates that expenses have to be matched with revenues as long as it is reasonable to do so. To follow this principle, adjusting entries are journal entries made at the end of an accounting period or at any time financial statements are to be prepared to bring about a proper matching of revenues and expenses.

Each adjusting entry has a dual purpose: (1) to make the income statement report the proper revenue or expense and (2) to make the balance sheet report the proper asset or liability. Thus, every adjusting entry affects at least one income statement account and one balance sheet account. Adjusting entries fall into two broad classes: accrued (meaning to grow or accumulate) items and deferred (meaning to postpone or delay) items. The entries can be further divided into accrued revenue, accrued expenses, unearned revenue and prepaid expenses.

For a merchandising company, Merchandise Inventory falls under the prepaid expense category since we purchase inventory in advance of using (selling) it. We record it as an asset (merchandise inventory) and record an expense (cost of goods sold) as it is used. The adjusting journal entry we do depends on the inventory method BUT each begins with a physical inventory.

A physical inventory is typically taken once a year and means the actual amount of inventory items is counted by hand. The physical inventory is used to calculate the amount of the adjustment.

Perpetual Inventory Method

Under the perpetual inventory method, we compare the physical inventory count value to the unadjusted trial balance amount for inventory. If there is a difference (there almost always is for a variety of reasons including theft, damage, waste, or error), an adjusting entry must be made. If the physical inventory is less than the unadjusted trial balance inventory amount, we call this an inventory shortage. This is the most common reason for an adjusting journal entry.

A YouTube element has been excluded from this version of the text. You can view it online here: pb.libretexts.org/llfinancialaccounting/?p=124

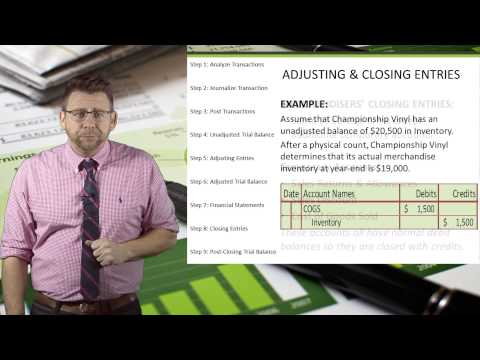

The video showed an example of an inventory shortage. Let’s look at another example. Our company has an unadjusted trial balance in inventory of $45,000 and $150,000 in cost of goods sold. The physical inventory count came to $43,000. We have a difference in inventory of $2,000 ($45,000 unadjusted inventory – $43,000 physical count) that needs to be recorded. We want to reduce our inventory and increase our expense account Cost of Goods Sold. The journal entry would be:

| Account | Debit | Credit |

| Cost of goods sold | 2,000 | |

| Merchandise Inventory | 2,000 | |

| To adjust inventory to match the physical count. | ||

When we post this adjusting journal entry, you can see the ending inventory balance matches the physical inventory count and cost of good sold has been increased.

| Account: Merchandise Inventory | Debit | Credit | Balance |

| Unadjusted Balance | 45,000 | ||

| Adjust for shortage | 2,000 | 43,000 |

| Account: Cost of goods sold | Debit | Credit | Balance |

| Unadjusted Balance | 150,000 | ||

| Adjust for shortage | 2,000 | 152,000 |

On the rare occasion when the physical inventory count is more than the unadjusted inventory balance, we increase (debit) inventory and decrease (credit) cost of goods sold for the difference.

Periodic Inventory Method

Under the periodic inventory method, we do not record any purchase or sales transactions directly into the inventory account. The unadjusted trial balance for inventory represents last period’s ending balance and includes nothing from the current period. We have not record any cost of goods sold during the period either. We will use the physical inventory count as our ending inventory balance and use this to calculate the amount of the adjustment needed.

A YouTube element has been excluded from this version of the text. You can view it online here: pb.libretexts.org/llfinancialaccounting/?p=124

To determine the cost of goods sold, a company must know:

- Beginning inventory (cost of goods on hand at the beginning of the period).

- Net cost of purchases during the period (purchases + transportation in – purchase discounts – purchase returns and allowances)

- Ending inventory (cost of unsold goods at the end of the period).

To illustrate, Hanlon Food Store had the following unadjusted trial balance amounts:

| Trial Balance Accounts | Debit | Credit |

| Merchandise Inventory | 24,000 | |

| Purchases | 167,000 | |

| Purchase discounts | 3,000 | |

| Purchase returns and allowances | 8,000 | |

| Transportation In | 10,000 |

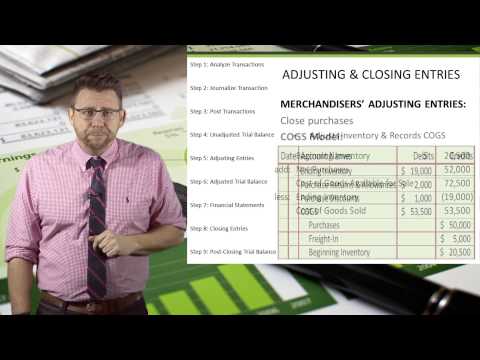

The unadjusted trial balance amount for inventory represents the ending inventory from last period. In our first adjusting entry, we will close the purchase related accounts into inventory to reflect the inventory transactions for this period. Remember, to close means to make the balance zero and we do this by entering an entry opposite from the balance in the trial balance.

| Account | Debit | Credit |

| Merchandise Inventory | 166,000 | |

| Purchase discounts | 3,000 | |

| Purchase returns and allowances | 8,000 | |

| Purchases | 167,000 | |

| Transportation In | 10,000 | |

| To close net purchases into inventory. | ||

Next we can look at recording cost of goods sold. The beginning inventory is the unadjusted trial balance amount of $24,000. The net cost of purchases for the year is $ 166,000 (calculated as Purchases $167,000 + Transportation In $10,000 – Purchase discounts $3,000 – Purchase returns and allowances $8,000). On December 31, the physical count of merchandise inventory was $ 31,000, meaning that this amount was left unsold. We calculate cost of goods sold as follows:

Beg. Inventory $24,000 + Net Purchases $166,000 – Ending inventory count $31,000 = $159,000 cost of goods sold

The second adjusting journal would increase (debit) cost of goods sold and decrease (credit) inventory for the calculated amount of cost of goods sold and would look like:

| Account | Debit | Credit |

| Cost of goods sold | 159,000 | |

| Merchandise Inventory | 159,000 | |

| To record cost of goods sold for the period. | ||

Next we would post these adjusting journal entries. We will look at the how the merchandise inventory account changes based on these transactions. The physical inventory count of $31,000 should match the reported ending inventory balance.

| Account: Merchandise Inventory | Debit | Credit | Balance |

| Unadjusted Balance | 24,000 | ||

| (1) Close net purchases | 166,000 | 190,000 | |

| (2) Record cost of goods sold | 159,000 | 31,000 |

Notice how the ending inventory balance equals physical inventory of $31,000 (unadjusted balance $24,000 + net purchases $166,000 – cost of goods sold $159,000).

Summary

The perpetual inventory method has ONE additional adjusting entry at the end of the period. This entry compares the physical count of inventory to the inventory balance on the unadjusted trial balance and adjusts for any difference. The difference is recorded into cost of goods sold and inventory.

The periodic inventory methods has TWO additional adjusting entries at the end of the period. The first entry closes the purchase accounts (purchases, transportation in, purchase discounts, and purchase returns and allowances) into inventory by increasing inventory. The second entry records cost of goods sold for the period calculated as beginning inventory (unadjusted trial balance amount) + net purchases – ending inventory (physical inventory account) from the inventory account.

- Financial Acccounting: Adjusting & Closing Entries to Income Summary (Perpetual Method) . Authored by: Prof Alldredge. Located at: youtu.be/YVVFrXptzTw. License: CC BY: Attribution

- Financial Accounting: Adjusting & Closing Entries to Income Summary (Periodic Method) . Authored by: Prof Alldredge. Located at: youtu.be/jgd0HuRHFoY. License: CC BY: Attribution