4.3: Classes and Types of Adjusting Entries

- Page ID

- 26193

What is an Adjusting Entry?

Adjusting entries reflect unrecorded economic activity that has taken place but has not yet been recorded because it is either more convenient to wait until the end of the period to record the activity, or because no source document concerning that activity has yet come to the accountant’s attention. Additionally, periodic reporting and the matching principle necessitate the preparation of adjusting entries. Remember, the matching principle indicates that expenses have to be matched with revenues as long as it is reasonable to do so. To follow this principle, adjusting entries are journal entries made at the end of an accounting period or at any time financial statements are to be prepared to bring about a proper matching of revenues and expenses.

With respect to when adjusting entries are made during the accounting cycle, they will be made after the unadjusted trial balance and before the company prepares its financial statements, bringing the amounts in the general ledger accounts to their proper balances.

Each adjusting entry has a dual purpose: (1) to make the income statement report the proper revenue or expense and (2) to make the balance sheet report the proper asset or liability. Thus, every adjusting entry affects at least one income statement account and one balance sheet account.

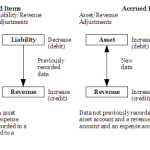

Adjusting entries fall into two broad classes: accrued (meaning to grow or accumulate) items and deferred (meaning to postpone or delay) items. The entries can be further divided into accrued revenue, accrued expenses, unearned revenue and prepaid expenses which will examine further in the next lessons.

The adjusting entries for a given accounting period are entered in the general journal and posted to the appropriate ledger accounts (note: these are the same ledger accounts used to post your other journal entries).

THREE ADJUSTING ENTRY RULES

- Adjusting entries will never include cash. Adjusting entries are done to make the accounting records accurately reflect the matching principle – match revenue and expense of the operating period. It doesn’t make any sense to collect or pay cash to ourselves when doing this internal entry.

- Usually the adjusting entry will only have one debit and one credit.

- The adjusting entry will ALWAYS have one balance sheet account (asset, liability, or equity) and one income statement account (revenue or expense) in the journal entry. Remember the goal of the adjusting entry is to match the revenue and expense of the accounting period.

- Accounting Principles: A Business Perspective. Authored by: James Don Edwards, University of Georgia & Roger H. Hermanson, Georgia State University. Provided by: Endeavour International Corporation. Project: The Global Text Project . License: CC BY: Attribution